Gold, silver, and Bitcoin have had an especially difficult year. At Mercer Advisors, we have stuck to our principles and avoided recommending these investments — even when they were sizzling. In this commentary, we share our analysis of this decline, showing how this crash underscores that gold, silver, and crypto are primarily speculative assets (and not investable assets).

How have gold, silver, and crypto performed?

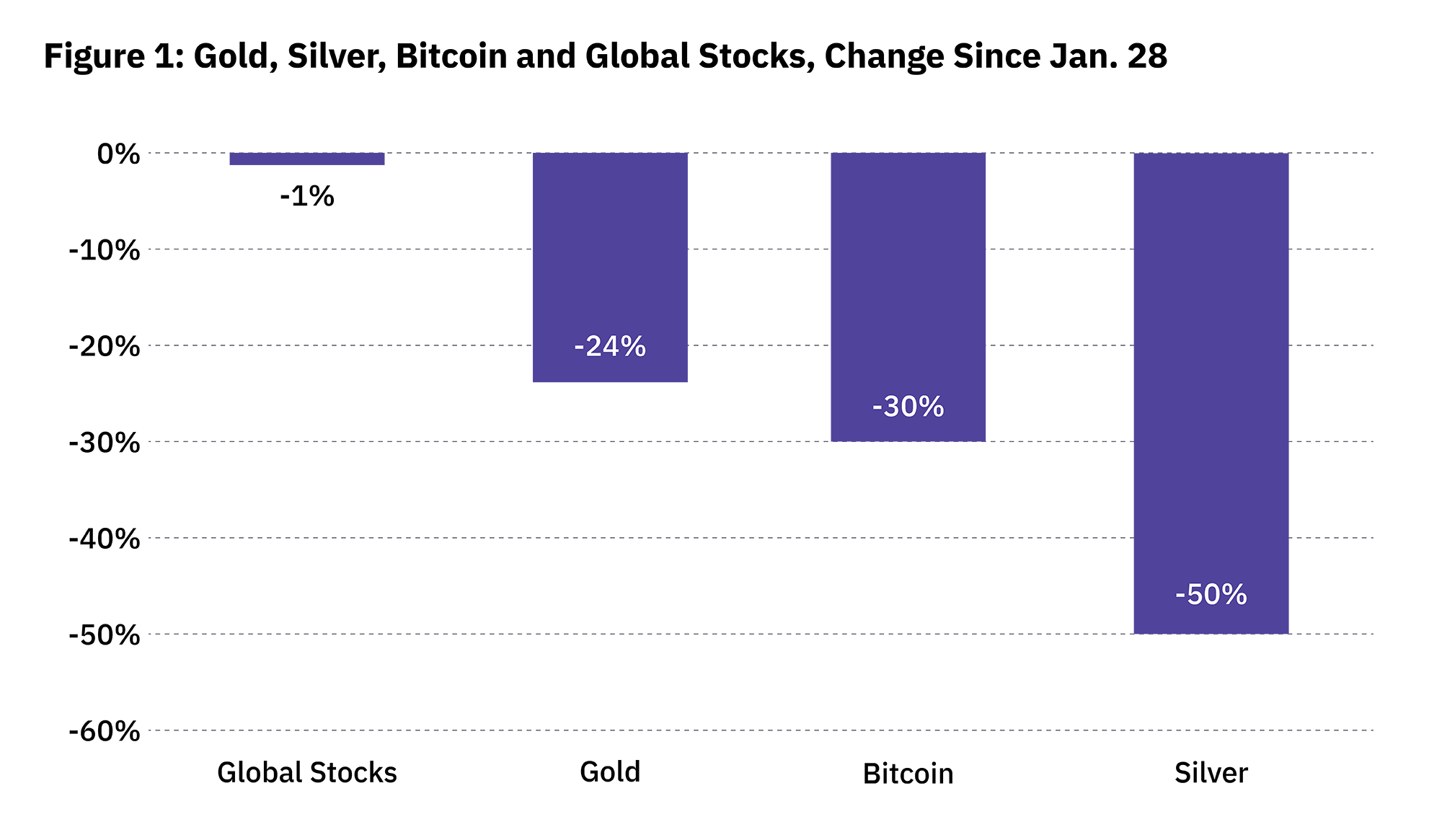

We last wrote about these assets in February (Why We Don’t Speculate on Gold, Silver, and Crypto), and since that time, their performance has continued to suffer.

Note: The performance of Bitcoin is even worse on a peak-to-trough basis. Bitcoin has fallen 49.4% since a peak in October 2025.

These declines are on par with some of the worst declines on record for equities. The declines in silver and bitcoin, for example, are similar to declines experienced by stocks during the bursting of the dot-com bubble and the global financial crisis — we’d associate the magnitude of these declines with world-shaking upheavals. A crucial difference, however, is that stock investors continued to earn dividend income during those downturns.

Given the economic and geopolitical turmoil of the past five months, wouldn’t we have expected gold, silver, and Bitcoin to be doing well?

Well, that’s the argument. When discussing the investment case for gold, silver, and Bitcoin, proponents often argue that these assets are safe havens during times of geopolitical turmoil, rising inflation, or ballooning federal debt. Through that lens, the past five months have been an ideal environment to pressure test this argument.

- Geopolitical turmoil: The Iran war began in late February.

- Inflation: As measured by the annual change in the Consumer Price Index, inflation has jumped from 2.4% in January to 4.2% in its most recent reading.

- The U.S. deficit: The deficit is running at an annual pace of nearly $2 trillion per year. In April, U.S. debt topped 100% of GDP for the first time.

Despite all this, these assets have experienced significant declines. Clearly these assets have not performed as expected or as predicted by their promoters.

So what has driven the decline?

The beginning of the decline in gold and silver coincided with President Trump’s announcement that he intended to nominate Kevin Warsh as the next chair of the Federal Reserve. Gold and silver had their worst day since 1980 immediately after that announcement.

Many investors assessed that Warsh (relative to other contenders for the Fed’s top job) would be vigilant against inflation and a decline in the U.S. dollar.

Notably, however, the interest rate environment hasn’t changed all that much since Warsh took over. The 10-year Treasury started the year at about 4.2% and is currently around 4.5%. That is meaningfully higher but not a dramatic repricing of the market. While Kevin Warsh’s tenure has only just begun, the bond market anticipates changes in Fed policy and currently doesn’t foresee dramatic shifts. That said, remember

What has been the role of speculation?

If geopolitics, inflation, and debt have — in theory — been supportive of these assets, and the interest rate environment hasn’t changed much, then this data strongly suggests the recent performance of gold, silver, and crypto has been heavily driven by sentiment from speculative investors.

While stocks certainly exhibit momentum as well, a range of factors influences the returns of the equity market — things like sales revenue, earnings growth, future cash flows, firm’s cost of capital, decisions made by management teams, and so much more. The pricing of speculative assets like gold, silver, and crypto are influenced almost exclusively by investor sentiment. They have no revenues and no earnings and therefore deliver no cash flows to investors, nor do they have management teams that can make active decisions to help improve returns for investors. These are just some of the key reasons why we prefer investable assets to speculative ones.

What is meant by an investable asset?

In our framework, we have outlined three criteria for investable assets:

- The asset should generate current (or future expected) cash flows.

- Investors’ ownership rights of the asset should be well defined and enforceable in U.S. courts of law.

- Investors should be able to buy and sell freely and securely through a regulated market (whether public or private).

Investable assets, therefore, include stocks, bonds, private equity, private credit, real estate, and more. These assets generate, or are expected to generate at some point in the future, a stream of profits, dividends, or interest payments that provide a basis for asset valuations.

What is meant by a speculative asset?

Investments that don’t pass these tests are speculative in nature. Gold, silver, and Bitcoin do not generate cash flows. Further, cryptocurrencies, including Bitcoin, lack clear ownership rights and well-established regulation. Collectibles or exotic cars would be other examples of assets we’d classify as speculative.

There have been times when investors have been able to sell their gold, silver, or crypto at a profit. Now is not one of those times, and unlike stocks or bonds, these assets are generating no income during their slump.

Without underlying cash flows, speculative assets tend to trade on short-term investor sentiment. This year has been a case in point.

Our takeaways

- Gold, silver, and Bitcoin are speculative assets. The year-to-date returns of these assets underscore their speculative nature and also illustrate that these assets do not provide reliable safe-haven protection against geopolitical conflict, inflation, or the growing federal debt burden.

- Our fiduciary duty is upheld by avoiding non-investable assets. Acting in a fiduciary capacity requires disciplined decision-making focused on clients’ best interests, not speculation. Our role is to provide thoughtful, evidence-based guidance focused on growing and protecting wealth.

- Diversify with an evidence-based approach. While broad diversification across and within asset classes is important, it must be intentional. Effective diversification is built through purposeful portfolio construction that includes allocations to investable assets with positive expected returns — and not through a scattershot inclusion of low- or negative-expected-return assets that behave in inconsistent, unreliable ways.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.