Kevin Warsh has assumed leadership of the Federal Reserve, pledging to reform the institution in meaningful ways.

Transitions in Fed leadership often bring moments of uncertainty, and Warsh has made clear his intention to shake things up. As a result, markets will be closely watching his every move in the months ahead, and we expect clients will have questions about what this means for their portfolios and whether interest rates will go up or down.

With that in mind, we want to share our framework for thinking about the relationship between the Fed and fixed income markets. It is still early in Chairman Warsh’s tenure, and we believe it is wise to remain humble rather than to attempt to predict his next steps. What we can offer, however, is a clear and grounded perspective to help guide your thinking as this new chapter unfolds.

What the Fed can control

While the Fed is sometimes portrayed as an all-powerful force in financial markets, the central bank directly controls a relatively limited set of tools:

- Short-term interest rates:The Fed’s primary policy lever is its ability to set the fed funds rate — the rate at which banks borrow from each other overnight. It is the economy’s shortest-term interest rate, and it meaningfully affects money markets and ultra short-duration fixed income (less than a year until maturity).

- The supply of reserves in the banking system: The Fed directly impacts the supply of reserves in the banking system by buying and selling Treasuries via open market operations, which effectively controls the liquidity in the system.

- Quantitative easing, tightening (QE, QT): The Fed can undertake large-scale purchases (known as QE) or sales (known as QT) of Treasuries and certain mortgage-backed securities. These actions influence longer-term rates and directly increase (or decrease) the level of reserves in the banking system.

- Forward guidance: The Fed’s communications around future policy intentions are meant to stabilize the market’s expectations of how interest rates will change. This is one area that Chairman Warsh appears most focused on changing. The Fed’s recent practice has been for all Fed officials (the chair, the governors, and the Fed presidents) to share their expectations of how the Fed’s interest rate will change in coming years. Markets have closely watched these collective forecasts, but at Warsh’s first Fed meeting, he declined to make any predictions.

What the Fed cannot fully control

While the Fed can influence other aspects of the financial markets, it does not control them, and many commentators offer muddled thinking on this point. The following sit outside the Fed’s control:

- Intermediate and long-term rates: The Fed can influence these rates, but intermediate and long-term rates are primarily driven by a complex combination of market expectations around economic growth, inflation, and the term premium — the extra compensation investors demand for taking on the risk that interest rates may change over the life of a bond. As an example, the Fed has not changed its target rate since January, yet the yield of the 10-year-Treasury has ranged from 3.9% to 4.7% this year.

- Corporate yields or mortgage rates: The Fed’s actions are not the primary driver of prices in these markets. This year, while the Fed’s policy rate has remained unchanged, mortgage rates have bounced from below 6% to above 6.5%.

- Fiscal dynamics: Ultimately, the supply of Treasury debt being issued is determined by Congress and the White House, as their policies determine the level of spending and the amount of tax revenue collected. Demand for Treasuries is influenced by an even wider array of factors beyond the Fed’s control, including investor appetite, banks’ regulatory requirements, and the reserves of foreign central banks.

- Market psychology: The Fed is but one influence on investor behavior and investors’ willingness and ability to tolerate risk.

Reviewing fixed income in 2026

With the limits of Fed policy in mind, what can we conclude about the performance of fixed income so far this year?

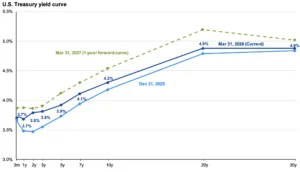

Interest rates have risen year-to-date, as shown in Figure 1 below, and are expected to continue climbing.

Figure 1 illustrates the yield curve at three points in time. The light blue line represents interest rates across different terms as we entered 2026, while the dark blue line reflects where the curve stood as of last week. The green dashed line shows the market’s current expectations for rates one year from now.

Figure 1: Treasury Yield Curve

Source: FactSet, Federal Reserve, J.P. Morgan Asset Management. Guide to the Markets – U.S. Data are as of June 24, 2026

These movements suggest that bond investors believe the risk environment for bonds has deteriorated. This is more than just a story about the Fed — the market remains concerned about the inflation and growth outlook as well as the federal government’s debt outlook.

Humility as Fed watchers

For the past year and a half, much of the conversation surrounding the Fed centered on President Trump’s desire for a chair who would lower short-term interest rates. His pick is now in place, yet rates have continued to climb. This may be surprising at first glance, but it shouldn’t be.

This is precisely why we place such emphasis on understanding which variables the Fed does and does not directly control. When it comes to longer-term rates, the Fed is largely along for the ride. It is a mistake to predict the trajectory of longer-term rates simply by listening to the Fed chair.

If a hall of fame existed for interest rate forecasters, it would be empty. No one has demonstrated a consistent ability to forecast rates successfully, including the Fed itself. This was true well before the new chairman announced his intention to move away from offering explicit guidance about the future direction of rates.

Takeaways for long-term investors

-

- Remain diversified across asset classes. The interest rates that matter most to us can shift in unpredictable ways. Rather than attempting to forecast the direction of interest rates or fixed income assets, we are better served by maintaining broad diversification across asset classes.

- Stick to your financial plan. As long-term investors, our financial plans are built with knowledge that interest rates are one of the countless market factors that are going to shift over the life of our investments. The fluctuations in markets this year are not such that we need to revisit our plans.

- Ensure adequate liquidity for the near-term. If you rely on your portfolio to fund ongoing expenses, it is worth reviewing whether you have sufficient liquidity in place to meet known near-term cash flow needs. This is a prudent step in any environment, but it is particularly relevant when markets are moving.

Not a client and want to learn more?

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy.

Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Chartered Retirement Plan Specialist℠ and CRPS℠ are trademarks or registered service marks of the College for Financial Planning in the United States and/or other countries.