So, you’ve decided to consider a long-short strategy. We understand this is a complex approach, and it may have taken time to get comfortable with it. In our experience, most people focus on understanding how to get started with the strategy.

But what happens after the strategy has been in place for a few years? What does your portfolio look like then? And how do you manage it over time?

Because long-short is still new to many investors — and even to some firms that help place clients into the strategy —there’s often a gap in understanding how these portfolios evolve in the future.

As fiduciaries, we firmly believe that our clients should fully understand the strategies they’re investing in.

This guide is designed to outline future options for long-short investors — because no one should enter the strategy unless they’re confident they’re working with a partner who can help them manage it over time.

Entering Long-Short

You may be considering a long-short strategy for a variety of reasons, most often it’s to manage the important assets in your financial picture. These assets are frequently the capstone of your professional accomplishments and the cornerstone of your wealth.

It is critically important to get this right.

Some of the most common situations addressed by a long-short strategy include:

Concentrated equity: Seeks to reduce risk tax efficiently. Create a diversified equity portfolio whose returns are driven by an investment manager’s stock-selection model, while managing concentrated stock positions tax-efficiently by deferring capital gains.

Business/Home sale: Use cash from sale (or existing cash or securities before the sale) to generate investment returns while harvesting tax losses that can offset capital gains from the sale of a business, home, or other investments.

Portfolio transition: Transition a portfolio of existing stocks, mutual funds, or ETFs into a diversified equity portfolio in a tax-efficient way. The long-short manager seeks to generate investment returns aligned with their stock selection model tracking the chosen benchmark, while unrealized taxable gains from the original portfolio transfer into the long-short portfolio.

Long Short Refresher

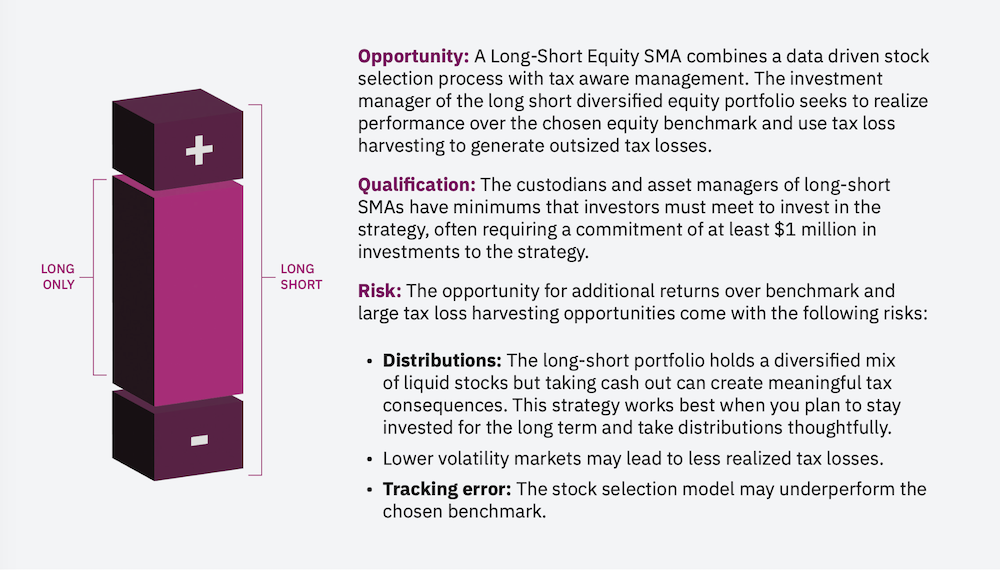

A Long-Short Equity Separately Managed Account (SMA) is designed to:

- Realize performance over the chosen equity benchmark

- Offer tax benefits that are expected to be sustainable

- Adapt to an investor’s evolving financial plan and cash flow needs

How does this differ from a direct indexing equity investment?

Direct indexing seeks to use long stock positions to generate returns in line with the benchmark while generating tax losses when markets decline through tax loss harvesting.

A long-short equity SMA adds short positions and additional market exposure through borrowing and seeks to outperform the chosen benchmark while generating significantly higher tax loss harvesting opportunities regardless of market direction.

Since the long-short portfolio’s borrowing, or “margin”, matches the size of its short positions — a structure often referred to as the portfolio’s “market neutral extensions” — there generally isn’t significant added market risk or a meaningful risk of a margin call. This is different from using margin to double down on a single stock or shorting a stock outright.

Long-Short in Action

A long-short strategy generally unfolds in three phases.

Phase One: Planning With Incoming Assets

Investors can fund a long-short account with concentrated stock, the proceeds from a business or home sale, or an existing portfolio of stocks, mutual funds, or ETFs.

- The investor selects an equity benchmark (S&P 500 or Russell 3000, for example) to track with their new portfolio and, in the case of cash funding, the amount of market risk they wish to take (“beta”).

- The investor chooses how quickly they want to diversify (three years or eight years, for example). Generally, the greater the level of borrowing, the more short-term capital losses (“tax losses”) will be generated, which can be used to offset realized capital gains.

- In the first year, the portfolio’s return is estimated to come from a combination of the initial investment and the diversified stocks gradually purchased in its place.

Phase Two: Tax-Efficient Transition

Proceeds of the legacy investment — whether from the sale of concentrated stock, a home or business, or an existing portfolio — are reinvested in a diverse portfolio of stocks.

- Portfolio returns are driven by a decreasing portion of the initial investment combined with an increasing portion of diversified stocks tracking the manager’s investment model. Because the new portfolio is invested in both long and short positions, the strategy will likely accumulate both gains and losses, regardless of whether the broader market moves up or down.

- Through active tax-loss harvesting and the use of market extensions, tax losses are created and used to help offset the capital gains on the portion of the legacy asset sold in any tax year.

- As the legacy asset is sold down, the portfolio becomes more diversified.

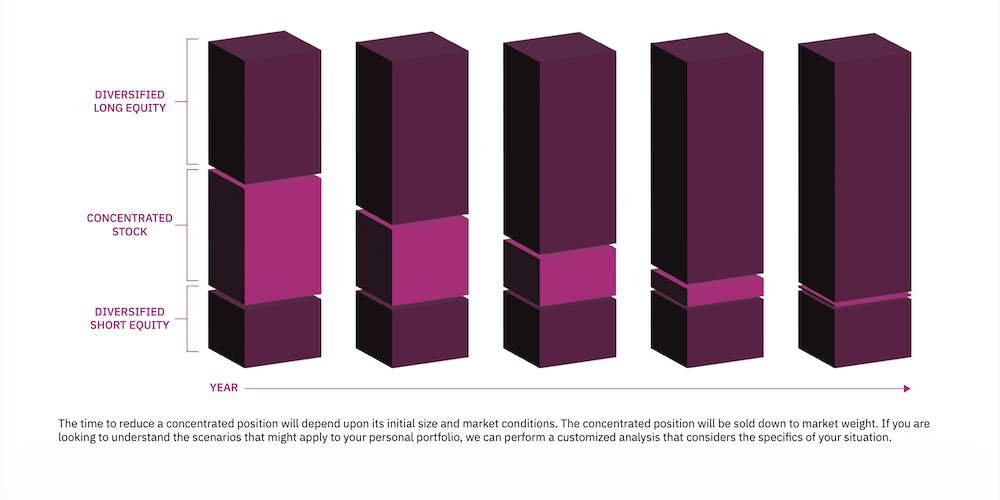

Phase Three: Diversified Portfolio

Over time, the legacy asset is sold down.

- The strategy defers taxes by shifting unrealized gains for the legacy assets into a diversified portfolio, and the investor can benefit from the compounding of investment returns having deferred tax payments.

- Any portfolio distribution at this stage will generate significant capital gains due to the portfolio’s market extensions. One dollar sold from the core portfolio will trigger the closing of associated positions in the long and short market extensions, and capital gains may be realized on each.

- The portfolio’s expected returns are now in line with the chosen benchmark, with differences in return driven by the manager’s stock selection and the degree of market extensions.

But what now?

This new situation still has complexity for the investor.

- The new, broadly diversified core portfolio will have unrealized capital gains

- The portfolio extensions used in the strategy will also have unrealized capital gains

- Portfolio distributions and changes will need to be carefully managed

Unrealized gains

For investors who haven’t used leverage before, the tax treatment of this strategy may be unexpected.

The new, broadly diversified portfolio will likely have more unrealized capital gains than it did with funding due to these three contributors:

- The portfolio follows its benchmark, plus or minus a tracking error. If the benchmarks increase in value, the portfolio will most likely as well.

- Because the goal of the strategy is to defer taxation, the number of gains realized during the initial years of the strategy are intended to be limited and are generally focused on keeping the portfolio in line with its benchmark.

- The stocks in the extensions, which were added through leverage, will have capital gains owed on them (positions that had losses were generally liquidated to recognize these losses).

Note that the tax owed is calculated using standard principles — when using leverage to purchase an investment, the initial purchase becomes the basis for tax purposes, and capital gains taxes are owed on any subsequent realized gains. This is not double taxation; however, an investor who isn’t familiar with the mechanics of the strategy may misinterpret it that way.

Thoughtful planning is needed to ensure

the initial tax deferral benefit is maintained.

After the Transition to a Diversified Portfolio

Once the transition to a diversified portfolio is complete, financial planning, estate planning, and tax strategy can be the difference-maker for maintaining the benefit of the deferred capital gains. Significant unrealized gains and continued strategy costs remain. At this point, the investor has a few decisions to make.

![]()

Option A is to continue with the long-short portfolio as-is.

Option B is to reduce the size of market extensions and the cost of the long-short portfolio. This process can take several years and it leaves the investor with three subsequent options:

- Keep the now lower-leveraged/lower-cost portfolio as-is.

- Reduce the size of the long-short portfolio through a cash distribution.

- Exit the long-short strategy entirely and keep the long-only diversified portfolio.

Considering your options

When considering your choices, investors should revisit their financial goals, risk tolerance, tax sensitivity, and liquidity needs. If, or when, your core preferences change, your long-short strategy can change with it. If your preferences have not changed, there is no need to exit the long-short strategy merely because you have diversified your concentrated position.

OPTION A

Keeping long-short as is

For investors who continue to receive ongoing tax-loss advantages from the long-short approach, staying in the portfolio remains an option even after the legacy position has been unwound.

- The portfolio’s performance will likely be in line with the chosen benchmark, with differences driven by stock selection and the degree of market extensions.

- The strategy will continue to generate tax benefits available to offset future capital gains or allow for tax efficient distributions from the portfolio

- The costs of the portfolio and leverage should stay the same.

OPTION B

Reduce market extensions & the cost of the portfolio

Investors may decide that once they have diversified their legacy position and/or deferred a large capital gain, that they want to unwind or reduce their long-short strategy, perhaps to return to something simpler or a strategy with less (or no) leverage.

- This transition will be most tax efficient if carried out over a period of years

- During the transition:

- The ongoing tax benefits generated by the L-S portfolio may be used to tax efficiently reduce leverage. The leverage is reduced by selling stocks and covering short positions in the extensions.

- The portfolio’s expected return is in line with the chose benchmark, with differences in return driven by stock selection and the size of market extensions

- Management and net borrowing costs reduce over time

Note: You can initially remain in the portfolio as-is for any number of years and switch to Option B at any time.

Long-Term State

Regardless of whether investors select Option A and stay in the strategy as-is for a few years and then began the Option B reduction of leverage, or choose Option B initially, they will generally end up in the same boat. What the investor has now, after reducing leverage, is a lower-cost long-short SMA, with smaller extensions (market-neutral leverage), smaller opportunity to outperform the index, and a smaller (but regular and ongoing) annual tax benefit.

Here are three long-term options, all dependent on your financial plan and cash flow needs. With careful planning, we believe option one and/or two will likely have the best outcomes for most investors.

Keep lower-cost long-short SMA as is.

- Can continue to serve as part of the core equity allocation.

- Continue to generate performance returns in line with the market with opportunity for outperformance.

- Realize ongoing tax benefits that allow for smaller tax efficient distributions each year.

- Costs are higher than long-only SMA

Take cash distribution out of long-short SMA and keep a significant portion invested.

- Use cash for other investments or cash flow needs.

- This option will require paying taxes on distributions – stock positions sold in the core portfolio will have embedded capital gains. As discussed earlier, those will be realized along with capital gains taxes on the associated long and short positions in the extensions. In this scenario, the extensions will be liquidated since they are collateralized by the stocks being sold in the core portfolio.

- For the remaining investment in the long-short SMA, the portfolio will now follow option 1 listed above.

Remove extensions entirely (all leverage removed from portfolio) and convert to a long-only portfolio.

- The strategy can be unwound entirely, and the SMA manager can be removed from the account.

- This will require realizing capital gains taxes on the liquidation of all long and short stock positions in the extensions.

- The remaining core equity portfolio is well diversified and can serve as a core part of asset allocation. It will have significant unrealized capital gains.

- Ongoing portfolio distributions will be taxable.

- The total tax benefit over the life of strategy will be significantly reduced, but the investor has likely still benefitted from the compounding effect of taxes deferred.

Conclusion

The decision to enter into a long-short strategy should be determined by a careful understanding not only of how to begin the strategy, but what the new portfolio will look like after the strategy has run for a number of years.

Once the transition is complete, financial planning, tax strategy, and estate planning are going to be critical considerations for reaping the most long-term benefits. The right options to pursue on the other side of long-short are going to be different for every investor. Working with an advisor that understands your entire financial situation will be very important.

For investors who qualify for a long-short strategy, Mercer Advisors can develop a customized analysis of what entering a long-short strategy would look like for you initially – and down the road.

The optimal outcome will require a thoughtful approach at the beginning and on the other side of the strategy. At Mercer Advisors, we’re prepared to not just help people enter a long-short strategy, but to manage it carefully along the way, and unwind it efficiently in the future.

“Mercer Advisors” is a brand name used by several affiliated legal entities owned by Mercer Advisors, Inc., including, Mercer Global Advisors, Inc., an SEC registered investment adviser providing investment advisory and family office services; Mercer Advisors Private Asset Management, Inc., an SEC registered investment adviser providing discretionary investment management services to affiliated private funds; Mercer Advisors Tax Services LLC, a tax services and accounting firm; Heim, Young and Associates, Inc., (MA Brokerage Solutions) a broker/dealer, member FINRA/SIPC; and Mercer Advisors Insurance Services, LLC (MAIS) an insurance agency.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. Hypothetical examples are for illustrative purposes only.

Long/short investment strategies will entail substantial risks and are not suitable for all investors, these strategies require a thoughtful approach and manager skill, and no assurance can be made that the portfolio managers will be successful. There is a risk of substantial loss associated with leverage. Before investing carefully consider your financial position and risk tolerance to determine if the proposed trading style is appropriate. Investors should realize that when engaging in leverage one could lose the full balance of their account. It is also possible to lose more than the initial deposit when engaging in leverage. The realized tax benefits associated with these strategies may be less than expected or may not materialize due to the economic performance of the strategy, an investor’s particular circumstances, prospective or retroactive changes in applicable tax law, and/or a successful challenge by the IRS. In the case of an IRS challenge, penalties may apply. The information provided may contain projections or other forward-looking statements regarding future events, targets or expectations and is current only as of the date indicated. There is no guarantee that targeted or expected characteristics will be realized or achieved, or that an investment strategy will be successful. Forward-looking statements are subject to numerous assumptions, risks and uncertainties which change over time.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy or product made reference to directly or indirectly, will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Diversification does not ensure a profit or guarantee against loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. Indices are not available for direct investment. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.