When the Iran war began, we noted that despite the alarming headlines, the underlying fundamentals of the stock market were strong. This has continued to be the case, as reflected in companies’ latest quarterly earnings reports.

Corporate earnings remain strong

As of June 1, 97% of companies have reported their earnings for the first quarter and the results have been robust.

Starting at the top of the income statement: top-line revenue growth is up 12% year over year, besting expectations going into earnings season by 2%.

The strength carries through further down the statement, where the net profit margin for S&P 500 companies increased from 13% to almost 15%, indicating that companies are becoming more efficient at turning revenue into profit. Together, these dynamics drove a 28% surge in earnings growth, exceeding expectations by 15%.

The Magnificent Seven (Alphabet, Amazon, Apple, Meta, Nvidia, Microsoft, Tesla) are once again playing a critical role in the headline figures, with earnings growth surging over 60%, their highest annual earnings growth rate since 2021.

To some extent, these figures were affected by one-time boosts, as several companies marked up the valuation of stakes they own in private companies. Alphabet, for example, recognized an almost $38 billion gain from such investments. Even after removing those one-time items, however, these companies saw earnings rise nearly 30%.

While the Magnificent Seven have been market leaders, the other 493 companies in the S&P 500 still posted robust earnings growth of over 17%. As shown in Figure 1, this stands in contrast to 2023, when the Magnificent Seven were soaring and the rest of the market was struggling.

Figure 1: S&P 500 Earnings Growth for Magnificent 7 and Other 493 Firms in S&P 500

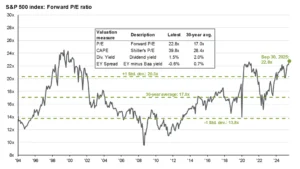

How did it impact valuations?

One of the key questions for investors right now is how the elevated valuations of U.S. equities will resolve. Valuations, typically measured by the price‑to‑earnings (P/E) ratio, reflect how much investors are willing to pay for each dollar of current and expected earnings. Higher P/E ratios signal higher expectations.

Extremely high valuations tend not to persist. They typically revert either because (1) stock prices decline or 2) earnings grow faster than prices, effectively validating the high expectations. As investors, we prefer the latter outcome.

So far in 2026 we’ve seen that dynamic begin to unfold. Valuations remain elevated, to be sure, but they are moving closer to their 30-year average, as shown in Figure 2.

Figure 2: S&P 500 Index: Forward P/E Ratio

Source: Bloomberg, FactSet, Moody’s, Refinitiv Datastream, Robert Shiller, Standard & Poor’s, J.P. Morgan Asset Management.

Forward P/E ratio is the most recent S&P 500 index price divided by consensus analyst estimates for earnings in the next 12 months, provided by IBES since March 1994 and FactSet since January 2022. Shiller’s P/E uses trailing 10-years of inflation-adjusted earnings as reported by companies. Dividend yield is calculated as consensus estimates of dividends in the next 12 months, provided by FactSet, divided by the most recent S&P 500 index price. EY minus Baa yield is the forward earnings yield (the inverse of the forward P/E ratio) minus the Bloomberg U.S. corporate Baa yield since December 2008 and interpolated using the Moody’s Baa seasoned corporate bond yield for values beforehand. Guide to the Markets – U.S. Data are as of May 29, 2026.

What does the market expect from earnings going forward?

Earnings growth expectations for full-year 2026 are now tracking 23% year over year, versus an expectation of 16% at the start of the year and compared with actual earnings growth of 12% in 2025.

It is worth noting that about 60% of that growth is expected to come from semiconductor producers and the so-called hyperscalers that operate the massive data centers behind the AI boom. This group of companies (Nvidia, Micron, Alphabet, Broadcom, Meta, Sandisk, Microsoft, Amazon) largely overlaps with the Magnificent Seven and highlights how reliant this rosy outlook is on the performance of a relatively small group of companies.

How does the U.S. compare to the rest of the world?

Earnings are rising abroad, but at a more modest pace. Earnings so far are up 5% in Europe and 17% in Japan. Top-line revenue growth declined 1% in Europe and is up 6% in Japan.

However, companies in non-U.S. markets trade at a significantly lower valuation than their U.S. counterparts. Non-U.S. equities trade at a 35% discount to U.S. equities for each dollar of earnings. This continues to provide a compelling rationale for maintaining international diversification.

Our takeaways

1. Remain broadly diversified. Earnings growth is strong, but the market’s performance is currently being driven disproportionately by a small number of companies. The Magnificent Seven and the hyperscalers are so large that diversified portfolios still have significant exposure — investors are not missing out — but this level of concentration introduces risk that is best managed through broad diversification.

2. Don’t try to time the market. Trying to predict when the market will rise or fall remains an impossible game. There is always a temptation to believe we can anticipate short- or medium-term moves, but the better course of action is to remain humble about where prices are heading.

3. Continue to invest for the long run. We’ve previously discussed how the market can be viewed as a “voting machine” in the short run and a “weighing machine” in the long run. Put differently, short‑term swings often reflect shifts in sentiment, while long‑term returns ultimately follow intrinsic value, driven primarily by earnings.

Ongoing geopolitical conflicts (like the war in Iran), high-profile IPOs, changes in Federal Reserve leadership, and whatever unexpected news tomorrow brings can all generate attention-grabbing headlines. Staying focused on long‑term intrinsic value — through low‑cost, broadly diversified portfolios that incorporate proven factors such as value and quality — remains a reliable path to durable long‑term outcomes.

-

It’s completely natural to feel unsettled when geopolitical events dominate the news. But the data from first-quarter 2026 earnings suggests the underlying health of the companies in the broad market has remained strong despite that uncertainty. Corporate earnings grew 28% year over year — well above expectations — and profit margins improved. At Mercer Advisors, we keep a close eye on how world events ripple through the economic landscape, but we don’t let short-term headlines drive long-term investment decisions. If you have specific concerns about your portfolio, your wealth advisor is the right person to contact.

-

The Magnificent Seven is a term used to describe seven of the largest technology companies in the S&P 500: Alphabet (Google’s parent company), Amazon, Apple, Meta, Nvidia, Microsoft, and Tesla. Because these companies are so large, they have an outsized influence on how the S&P 500 performs overall. Their first-quarter 2026 earnings grew over 60%, which had a significant effect on the broader index. Even if you hold a diversified portfolio, you very likely have meaningful exposure to these companies — you’re not missing out. What your wealth advisor watches closely is whether that exposure remains balanced and aligned with your personal goals.

-

The price-to-earnings (P/E) ratio tells you how much investors are paying today for each dollar of a company’s earnings. Think of it as a measure of expectations: a higher P/E ratio means investors expect strong future growth; a lower ratio suggests more modest expectations or that a stock may be more attractively valued. U.S. stocks carry elevated P/E ratios now, meaning expectations are high. The encouraging news is that strong earnings growth in early 2026 is helping bring those ratios closer to their historical norms.

-

U.S. equity valuations are above their long-term historical averages, which is worth keeping in mind. That said, elevated valuations don’t always resolve through falling prices — they can also normalize because earnings grow faster than prices, which is exactly what we’re beginning to see now. Your wealth advisor takes valuations into account when reviewing your portfolio’s overall positioning, but elevated valuations alone are not a signal to move out of the market.

-

It’s a fair question. The U.S. market has been a strong performer, and it’s natural to wonder whether international exposure is worth keeping. Here’s the case for it: non-U.S. stocks trade at a 35% discount to U.S. stocks for each dollar of earnings. That meaningful valuation gap suggests there could be real long-term opportunity in international markets, even if their recent growth has been more moderate. Diversification — including across geographies — helps reduce the risk that any one market’s downturn has an outsized effect on your overall portfolio.

-

Strong earnings are good news, and we want you to feel confident in that. But a strong quarter isn’t a reason to chase performance, shift your strategy, or try to predict what comes next. The most reliable path — supported by decades of evidence — is to stay broadly diversified, keep costs low, and remain invested for the long run. Your wealth advisor reviews your portfolio on a regular basis to make sure it’s aligned with your goals, your timeline, and your comfort with market fluctuations. If you have questions about how your specific investments are positioned, that conversation is exactly what we’re here for.

-

Whether to invest additional funds always depends on your unique financial situation — your income, your goals, your timeline, and how you’d feel if markets pulled back in the short term. There’s no single right answer for every person. What we can say is that trying to find the “perfect moment” to invest has historically proven far less effective than investing reliably over time, regardless of short-term conditions. If you’re considering investing additional funds, your wealth advisor can help you think through the approach that makes the most sense for your situation.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

Chartered Retirement Plan Specialist℠ and CRPS℠ are trademarks or registered service marks of the College for Financial Planning in the United States and/or other countries.