If you’re working with a financial advisor to build your financial plan, you know where you currently stand and where it is you want to go. Your financial plan is the roadmap for how to get there. The final remaining piece of the puzzle, how best to invest your savings, is a critical one. Your portfolio is the engine that will drive your financial plan.

Get it wrong and you could find yourself wildly off course, perhaps with your destination permanently out of reach. Get it right, and you arrive at your destination on time. So, what’s the best way to put your hard-earned savings to work? Mercer Advisors believes it is factor investing, a strategy we implement for our clients.

Factor investing offers a smart, transparent, and rules-based alternative to both indexing and active management. Borrowing from indexing and active management, factor investing takes a structured, process-driven approach to investing – embracing broad diversification and the theory of market efficiency.

Investing in active management: Does it pay?

Active management is best defined as an investment approach that relies on the use of a human element, typically a single manager or a team of managers, to actively manage a portfolio with the objective of outperforming a broad market index such as the S&P 500 Index. Active managers rely on in-house analytical research, forecasts, and their own judgment and experience in making investment decisions on what securities to buy, hold, and sell – and in what weights. Active managers believe markets are “inefficient” and that it’s possible to outperform the broad market by identifying and investing in mispriced stocks, bonds, and other securities. The opposite of active management is commonly referred to as “passive management” or “indexing.”

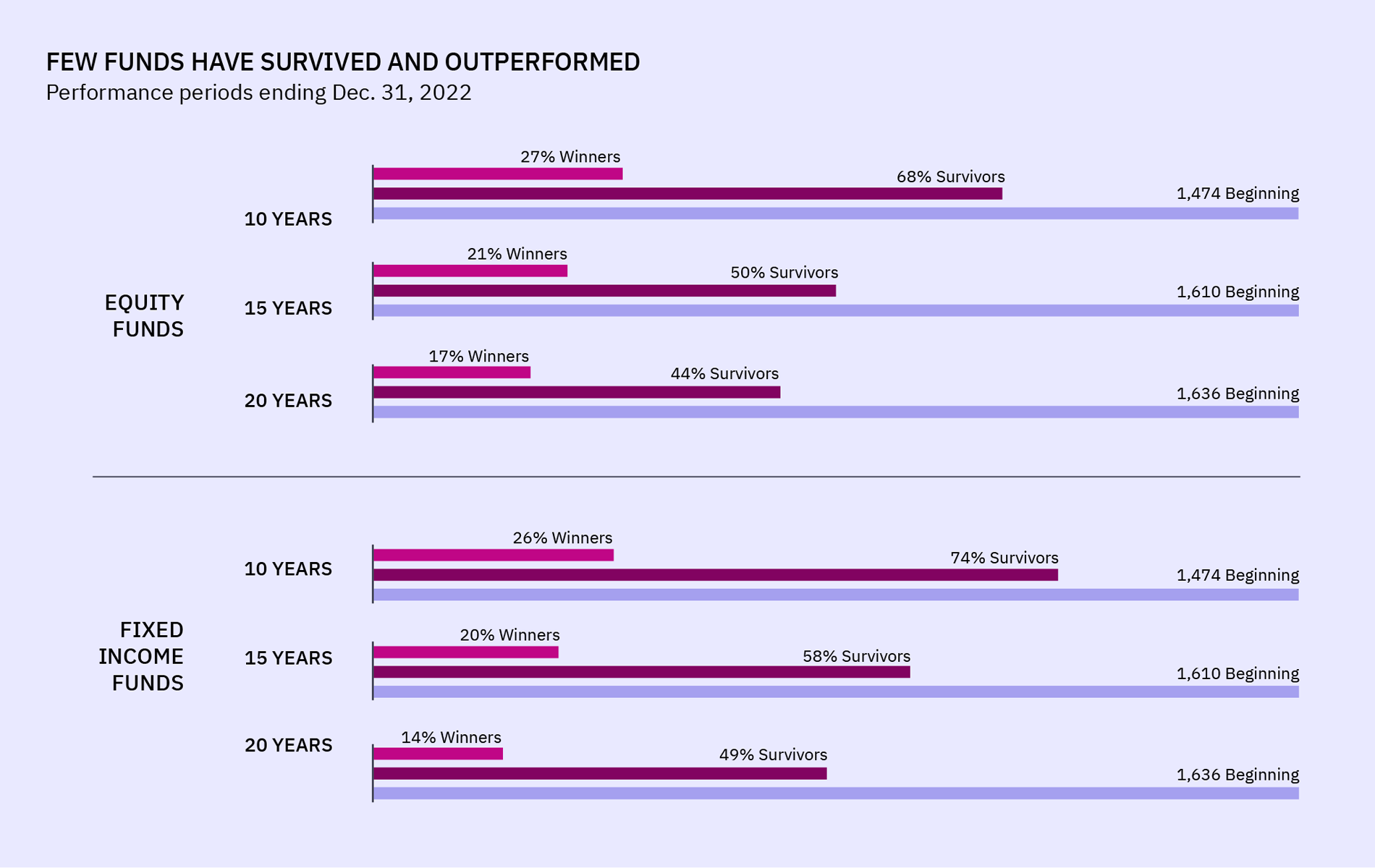

There is a certain romantic appeal to the notion that a financial guru can, against the odds, outperform the broad market through hard work, raw talent, or superior intellect. We see such outperformance in other areas of human endeavor, such as sports or standardized testing, where gifted individuals rise to the top to outperform their peers. However, outperformance in these areas doesn’t translate to financial markets where, in fact, many decades of real-world data conclusively show that nearly all active managers underperform a simple market index. Consider the below data that details mutual fund outperformance over the 20-year period ending Dec. 31, 2022.

The probability of an actively managed mutual fund surviving longer than 20 years is below 50%. Further, the odds of an actively managed fund outperforming its index are exceptionally low (17% for equity managers and 14% for bond managers).

1 Index Data Sources: Index data provided by Bloomberg, MSCI, Russell, FTSE Fixed Income LLC, and S&P Dow Jones Indices LLC. Bloomberg data provided by Bloomberg.

Index investing: If you can’t beat them, join them?

It’s precisely because of the poor results posted by active managers that indexing has become such a powerful force in investing. Firms such as Vanguard have grown tremendously over the past several decades due to the failure of active portfolio management to deliver value. Index investing has been shown to deliver superior returns, and at lower costs than active management, largely due to the high fees and poor diversification associated with active management –making it virtually impossible for such managers to beat their respective indexes.

The secret to indexing’s relative success rests on some very simple observations gleaned from financial theory. First, indexing embraces broad diversification within an asset class. For example, an S&P 500 Index fund purchases all 500 stocks in the index (or a statistically representative sample) rather than trying to divine which individual stocks out of all 500 will outperform in the quarter or year ahead. Both financial theory and mathematics tell us that there’s safety in numbers; more is better, both in terms of risk reduction and superior returns. Second, indexing embraces the efficient markets hypothesis (“EMH”), which postulates that the market “prices in” all publicly available information. If true, this means there are no arbitrage opportunities for active managers to capture risk-free returns. Finally, because indexing doesn’t rely on high-priced financial gurus or constant trading, index fund fees are significantly less expensive than their actively managed competitors, resulting in better returns.

Factor investing: Transforming the way portfolios are constructed and managed

The discussion, however, doesn’t stop at indexing. Walk into any graduate-level investing or portfolio management course at any leading business school in the world, and you’ll find factor investing constitutes the core of the curriculum. And for good reason: factor investing is the modern manifestation of more than nine decades of scientific inquiry into financial markets.

Factors are defined as those quantifiable characteristics that have been shown to be reliable predictors of future outperformance. In equities, the most popular factors include value, quality, momentum, and size. With respect to bonds, factors include term (the length of time until the lender is repaid) and credit (the credit quality of the borrower). All are transparent and quantifiable using data pulled from publicly available financial statements, such as a firm’s balance sheet, income statement, or statement of cash flows.

Factor investing borrows from both indexing and active management. It embraces broad diversification; it does not seek to outperform by way of market timing or concentrating holdings in a handful of stocks or bonds, nor does factor investing attempt to identify mispriced securities.

It embraces the theory of market efficiency and subsequently benefits from low fees. Like active management, factor investing’s objective is to outperform the market. However, unlike active managers, factor investing aims to do so by taking a structured, process-driven approach to investing—not one reliant upon human judgment or experience, both of which are arbitrary and anecdotal (read: not scientific).

In contrast to active management and indexing alike, proponents of factor investing argue that certain assets outperform others for risk-based reasons, not because they’re mispriced. The central premise behind factor investing is that riskier investments are required to pay higher returns for the privilege of putting an investor’s capital to work. Think of the market as a highly competitive global auction with the users of capital (corporations and governments) on one side and the providers of capital (investors like you) on the other. Riskier companies and governments are required to pay higher returns to investors for the privilege of using their capital. We see this in markets all the time. For example, those with lower credit scores are required to pay a higher interest rate for a home mortgage, and vice versa. Financial markets—those markets seeking to put your savings to work—aren’t any different.

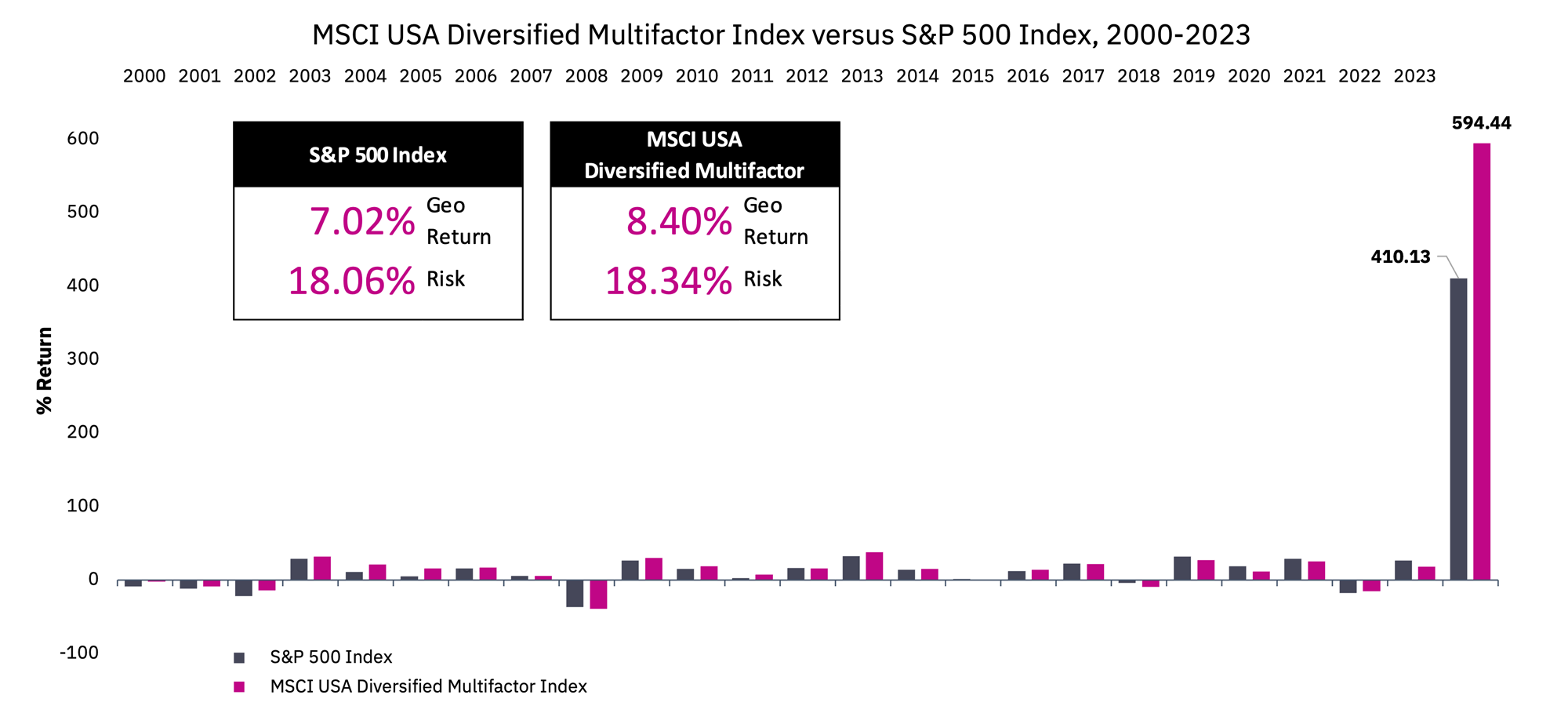

Does this mean factor investing is riskier than, say, indexing? Yes and no. While individual factors usually have higher risk than a typical index, by diversifying, these risks can be lowered without compromising returns. See the below data, from 2000 – 2023 the MSCI USA Diversified Multifactor Index—which invests in US stocks that exhibit the value, momentum, quality, and size factors—outperformed the S&P 500 Index by 1.38% annually with only 0.28% more risk.

2 Source: Bloomberg L.P.

There are three takeaways from this discussion. First, active management’s approach to investing is expensive, underperforms, and subjects your financial plan to unnecessary risk. Second, the low costs and diversification benefits associated with indexing have historically delivered better returns relative to active management. Finally, factor investing offers an intelligent, transparent, and rules-based alternative to both indexing and active management.

To learn more about factor investing, contact your advisor. If you’re not currently working with Mercer Advisors and would like more information on our investment management and planning services, let’s talk.