Introduction: The Shift From Accumulation to Distribution

For decades, your primary financial objective has likely been accumulation: saving diligently, investing for growth, and building a robust portfolio. These assets are frequently the capstone of your professional accomplishments and the cornerstone of your wealth. However, as you approach retirement, the paradigm shifts fundamentally. You must transition from an accumulation mindset to a distribution mindset.

This transition can be psychologically challenging. Instead of watching your balances grow through regular contributions, you are now drawing down those assets to support your lifestyle. The fear of outliving one’s money is a common concern among retirees, often leading to overly conservative investment choices or unnecessary frugality.

The role of a financial advisor

At Mercer Advisors, we can be your partner during this transition, helping you approach financial decisions with clarity and proper timing. A successful distribution strategy seeks to balance your current lifestyle desires with the need for long-term portfolio sustainability. It requires a comprehensive view of your financial picture, incorporating investment management, tax planning, estate planning, and insurance solutions.

When the transition to a diversified retirement portfolio is complete, financial planning, estate planning, and tax strategy can be the difference-makers for maintaining the benefit of your life’s work.

Chapter 1: Building a Retirement Paycheck

During your working years, your paycheck provided a predictable stream of income. In retirement, you must engineer your own paycheck using a variety of sources. When strategizing income stability, consider diverse sources that can provide for your future, such as retirement accounts, pensions, part-time work, and Social Security benefits.

A practical first step is to be mindful about your spending in the years leading up to retirement. Start by separating your spending into two categories — mandatory expenses (the items you need) and discretionary expenses (the items you want). Mandatory expenses include housing, healthcare, groceries, and insurance. Discretionary expenses cover travel, hobbies, dining out, and gifting.

After you’ve established a liquidity budget that maps out how much cash or near-cash you need readily available and when, you can allocate the proceeds into buckets for short-term needs, long-term investments, and discretionary spending. (In Chapter 5, we discuss bucket strategies in more detail.)

Your income needs will shift throughout retirement, and a sustainable withdrawal strategy should evolve alongside market conditions, lifestyle changes, and unexpected expenses.

When your investment portfolio is your primary income engine — not Social Security or pension income — the central discipline becomes designing a tax-efficient withdrawal hierarchy across your taxable, tax-deferred, and tax-free accounts. It should be constructed to consistently fund your lifestyle, preserve your capital base, and support the legacy you intend to leave.

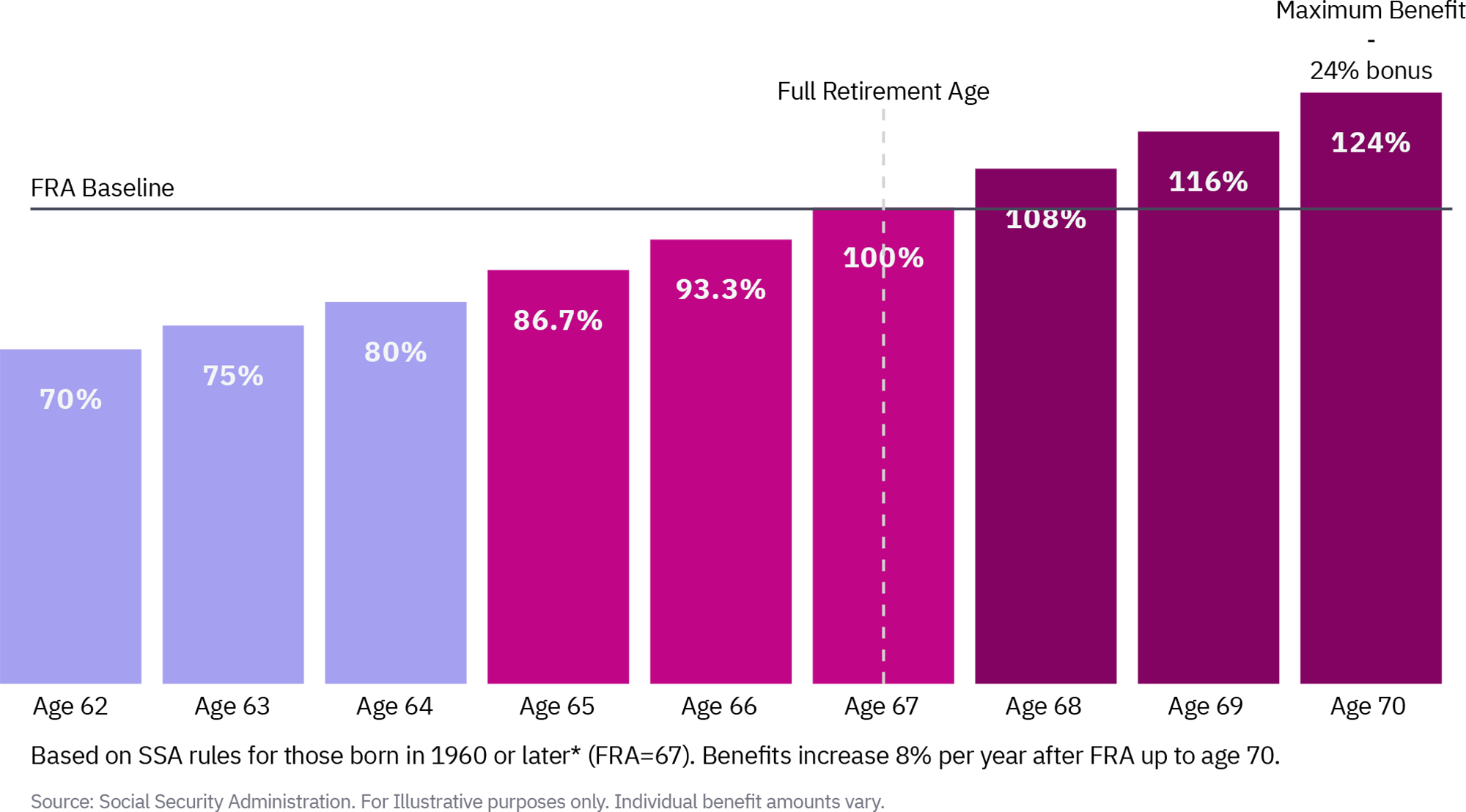

Chapter 2: Social Security Timing Strategy

Social Security remains a foundational element of retirement income for many Americans. According to a 2025 survey, 91% of retirees rely on Social Security for income, and 53% cite it as a primary source.1 For high-net-worth individuals, optimizing this benefit could generate thousands of dollars in additional income and support broader goals, such as tax efficiency, asset preservation, and legacy planning.

Delaying Social Security benefits past your full retirement age (FRA) results in higher monthly payments — up to 8% more for each year you wait, until age 70. Conversely, benefits decrease by as much as 30% if you collect them early at age 62.

Additionally, married couples must consider spousal and survivor benefits. Coordinating when each spouse claims their benefit can maximize the lifetime payout for the household and help ensure the surviving spouse receives the highest possible ongoing benefit.

Chapter 3: The 4% Rule and Its Critics

The “4% rule” has long been a rule of thumb in retirement planning. Originating from research in the 1990s, it suggests that retirees can withdraw 4% of their portfolio in the first year of retirement and adjust that dollar amount for inflation in subsequent years, with a high probability that their money may last for 30 years. Many investors feel comfortable taking out 4% from their retirement savings each year at first and adjusting later based on inflation and market performance.

For retirees with additional guaranteed income sources — such as a defined benefit pension, annuity payments, or substantial rental income — the 4% rule may be less constraining than it appears. When reliable income already covers a meaningful portion of your mandatory expenses, your portfolio may need to fund only the gap, potentially allowing for a more flexible or even higher sustainable withdrawal rate from invested assets. In these cases, the more relevant planning question is not “how much can I withdraw?” but “how do I coordinate all of my income sources to minimize taxes and maximize longevity?”

Endowments and foundations, which operate under certain constraints, often target annual spending rates of approximately 4-5%, requiring portfolios to generate consistent returns while preserving long-term purchasing power.

Individual investors could similarly adopt a flexible approach. Dynamic spending rules — which adjust withdrawal rates based on portfolio performance — can help preserve capital during market downturns while allowing for increased spending during bull markets.

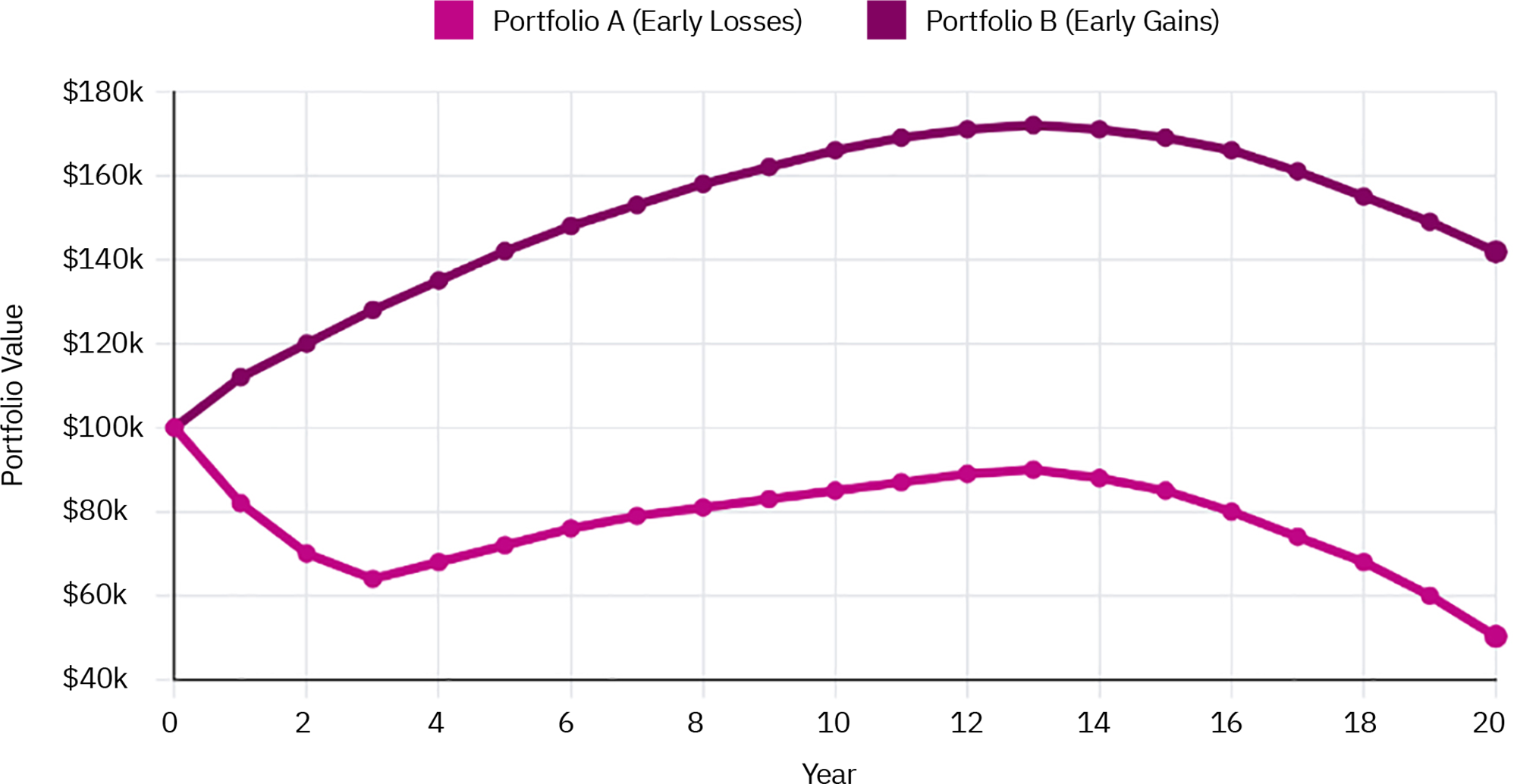

Chapter 4: Sequence-of-Returns Risk

Sequence-of-returns risk refers to the danger of experiencing negative market returns early in your retirement. When you are accumulating wealth, the sequence of returns matters less than the average annualized return. However, when you begin taking distributions, early market downturns can severely deplete your portfolio, making recovery difficult even if the market rebounds later.

Consider two fictitious retirees with identical portfolios and identical average returns over a 20-year period. If Retiree A experiences a market crash in the first three years of retirement while withdrawing funds, the portfolio is permanently impaired. Retiree B, who experiences the same crash in year 17, is largely unaffected because the portfolio had years to compound before the downturn.

Starting value $100,000 with annual withdrawals of $5,000. Returns are mirrored — Portfolio A’s year 1 return is Portfolio B’s year 20, and vice versa. The math is identical in reverse, yet the outcomes diverge sharply.

What the chart demonstrates and why it matters

The setup: Both portfolios start with $100,000 and take $5,000 in annual withdrawals. The yearly returns are mirror images of each other (Portfolio A’s year 1 = Portfolio B’s year 20, etc.), so the arithmetic average return is identical at 5% for both.

What happens: Portfolio A suffers its largest losses in the early years (-18%, -12%, -8%) when the portfolio is at its largest. Those losses hit a big base, and the investor is still withdrawing cash, so there’s less capital left to benefit when the good years arrive. Portfolio B is designed to strategically position itself to potentially benefit from gains before considering any downturns.

The core insight — sequence-of-returns risk: Compounding is asymmetric. A 20% loss requires a 25% gain just to break even. When losses occur early, they permanently shrink the base from which future returns compound. Average return is a misleading statistic on its own. The returns you get are influenced by the average performance of the market. This risk is especially critical during the retirement “red zone” — the five to 10 years before and after you stop working, when your portfolio is at its peak and you’ve just begun drawing it down.

Chapter 5: Bucket Strategies

A strong retirement income strategy should reflect both flexibility and timing. You might consider using a bucket strategy to help manage the transition into retirement and mitigate sequence-of-returns risk.

This approach typically involves dividing your portfolio into three buckets:

- Short-term: Cash and cash equivalents designed for immediate income needs over the next one to three years. This bucket offers a level of protection, ensuring that near-term expenses are covered, even in varying market conditions.

- Intermediate-term: Bonds and fixed-income securities intended for stability and income over the next three to 10 years. In a higher-for-longer interest rate environment, short-duration fixed income can offer competitive yields and lower sensitivity to interest rate changes, making it an attractive option for this bucket.

- Long-term growth: Equities and alternative investments aimed at providing growth for future needs beyond 10 years.

This structure can help support the “bridge years” between retirement and claiming Social Security or other income sources while allowing confidence to spend intentionally during active years. As the short-term bucket is depleted, it is systematically replenished by income and gains from the intermediate and long-term buckets.

Chapter 6: Withdrawal Sequencing

In a bucket strategy, asset location also matters. It is important to understand how various accounts are taxed, allowing buckets to be structured with tax efficiency in mind. Withdrawal sequencing — the order in which you tap your taxable, tax-deferred, and tax-free accounts — can have a profound impact on the longevity of your portfolio.

Generally, a tax-efficient withdrawal strategy might involve:

- Taxable accounts: Selling assets with minimal capital gains or using tax-loss harvesting to offset gains. These accounts are often tapped first to allow tax-advantaged accounts more time to grow.

- Tax-deferred accounts: Drawing from traditional IRAs and 401(k)s, keeping in mind that these distributions are taxed as ordinary income.

- Tax-free accounts: Tapping Roth IRAs last, allowing them to continue growing tax-free and serving as a valuable legacy asset for heirs.

However, this is not a one-size-fits-all rule. In some years, it may make sense to strategically withdraw from tax-deferred accounts up to the top of a lower tax bracket, or to consider Roth conversions during low-income years.

Chapter 7: RMD Planning

Required minimum distributions (RMDs) are the minimum amounts that a retirement plan account owner must withdraw annually starting at a certain age. Failing to take an RMD can result in significant penalties, making proactive planning essential.

Recent legislation has altered the landscape for RMDs, providing retirees with a longer window to execute tax-planning strategies like Roth conversions. Your RMD start age depends on when you were born. For those born between 1951 and 1959, RMDs begin at age 73. If you were born in 1960 or later, they begin at age 75.2

Additionally, under the SECURE 2.0 Act, a new “spousal election” allows a surviving spouse who is the sole beneficiary of a defined contribution plan to be treated as the original account owner.

RMDs can push you into a higher tax bracket and trigger increases in your cost for Medicare coverage. To manage this, some investors consider Qualified Charitable Distributions (QCDs). A QCD allows you to transfer funds directly from your IRA to a qualified charity, satisfying your RMD without adding to your adjusted gross income (AGI). This can be an effective strategy for philanthropically minded retirees.

Chapter 8: Healthcare Cost Planning

Healthcare is often one of the largest expenses in retirement. Navigating Medicare options and healthcare cost planning is a critical component of setting yourself up to thrive.

While Medicare covers many medical expenses, it does not cover everything. Premiums, deductibles, copayments, and out-of-pocket costs for services like dental, vision, and long-term care can add up quickly. Furthermore, as mentioned earlier, higher taxable income can lead to Income-Related Monthly Adjustment Amounts (IRMAA), which increase your Medicare Part B and Part D premiums.

A Health Savings Account (HSA) can be a powerful tool. An HSA started during your working years can help pay for medical expenses in retirement, preserving your other assets.

Additionally, planning for potential long-term care needs — whether through insurance, self-funding, or hybrid policies — is a vital step in protecting your portfolio from catastrophic health events.

Chapter 9: Inflation Protection

Inflation can silently erode purchasing power. Over a 20- or 30-year retirement, even a modest inflation rate can significantly reduce the real value of your income. When tallying the income you expect to receive, it is crucial to determine which sources may keep pace with inflation.

Social Security benefits typically include an annual cost-of-living adjustment (COLA), which helps protect against inflation. However, your investment portfolio must also be structured to generate returns that outpace inflation over the long term. This often requires maintaining a strategic allocation to equities and real assets, even in retirement.

While it may feel counterintuitive to hold volatile assets when you are no longer working, a diversified portfolio that includes growth-oriented investments seeks to ensure that your wealth can sustain your lifestyle for decades to come. Assets such as dividend-growth stocks, real estate, and Treasury Inflation-Protected Securities (TIPS) can play a role in a comprehensive inflation-protection strategy.

Conclusion: Your Retirement, Your Plan

Retirement is not a destination. It is a decades-long journey that deserves the same rigor, intention, and strategic thinking you brought to building your wealth in the first place. The concepts addressed throughout this guide — from the shift in mindset that retirement demands to the technical architecture of a tax-efficient withdrawal strategy — are not isolated decisions. They are interconnected elements of a single, comprehensive plan.

Each chapter has examined a distinct dimension of retirement income planning, yet the most important takeaway is how profoundly these dimensions interact. The timing of your Social Security claim affects your tax bracket, which influences your Roth conversion strategy, which shapes how your RMDs unfold, which determines how much of your portfolio remains exposed to sequence-of-returns risk. A decision in one area ripples across all others.

This is precisely why retirement income planning benefits from a coordinated, comprehensive approach — one that brings together investment strategy, tax planning, estate planning, and healthcare preparation under a unified framework.

Next step

From paying a bill to planning for the full arc of retirement, every question is valid and important, and support is available every step of the way. When you are ready to take the next step, whether that means reviewing your current withdrawal strategy, stress-testing your portfolio against a market downturn, or simply asking a question you have been carrying for months, we are just a call or email away to walk alongside you with care, patience, and understanding.

Your retirement is the culmination of a lifetime of discipline, hard work, and good decisions.

It deserves a plan that honors that effort — and a partner committed to helping you make it last.

Frequently Asked Questions

-

The accumulation phase occurs during your working years when you are saving and investing to build wealth. The distribution phase begins in retirement when you start withdrawing from those assets to generate a sustainable income stream.

-

Building a retirement paycheck typically involves coordinating multiple income sources, such as Social Security, pensions, and portfolio withdrawals. Creating a liquidity budget and using a bucket strategy can help ensure you have cash available for short-term needs while keeping long-term assets invested for growth.

-

While you can claim benefits as early as age 62, delaying until your full retirement age (FRA) or up to age 70 can increase your monthly payout. Benefits increase by up to 8% for each year you delay past your FRA.

-

The 4% rule is a helpful starting point, but it may not be suitable for everyone. We generally recommend a flexible withdrawal strategy that adjusts based on market conditions, inflation, and your personal financial plan.

-

This is the risk of experiencing poor investment returns early in retirement. Significant market declines while you are actively withdrawing funds can deplete your portfolio faster than anticipated, making recovery difficult.

-

A bucket strategy divides your portfolio into segments based on time horizons. Short-term buckets hold cash for immediate needs, intermediate buckets hold bonds for stability, and long-term buckets hold equities for growth. This seeks to prevent you from having to sell volatile assets during a market downturn.

-

Withdrawal sequencing depends on your individual tax situation. A common approach is to draw from taxable accounts first, followed by tax-deferred accounts (like traditional IRAs), and finally tax-free accounts (like Roth IRAs). However, strategic planning with a tax professional may reveal opportunities for Roth conversions or other optimizations.

-

Required minimum distributions (RMDs) mandate that you withdraw a certain amount from tax-deferred accounts annually. These distributions are taxable and can potentially push you into a higher tax bracket or increase your Medicare premiums.

-

To protect against inflation, a portion of your income sources (like Social Security) should have cost-of-living adjustments. Additionally, maintaining a diversified investment portfolio with an allocation to growth assets can help your wealth outpace inflation over time.

- 2025 EBRI/Greenwald Retirement Confidence Survey.” EBRI.org, April 24, 2025

- “IRS Uniform Lifetime Table.” IRS.gov, June 25, 2026.

- “Projected Savings Medicare Beneficiaries Need for Health Expenses in Retirement up Again in 2025.” Employee Benefit Research Institute, March 5, 2026.

“Mercer Advisors” is a brand name used by several affiliated legal entities owned by Mercer Advisors, Inc., including, Mercer Global Advisors, Inc., an SEC registered investment adviser providing investment advisory and family office services; Mercer Advisors Private Asset Management, Inc., an SEC registered investment adviser providing discretionary investment management services to affiliated private funds; Mercer Advisors Tax Services LLC, a tax services and accounting firm; Heim, Young and Associates, Inc., (MA Brokerage Solutions) a broker/dealer, member FINRA/SIPC; and Mercer Advisors Insurance Services, LLC (MAIS) an insurance agency.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. Hypothetical examples are for illustrative purposes only.

Mercer Advisors is not a law firm and does not provide legal advice to clients. All Estate planning document preparation and other legal advice are provided through select third parties, with which Mercer Advisors has a contractual relationship. Mercer Advisors Tax Services, LLC, does not provide financial audit, assurance, compilations, or forensic accounting services. Insurance products are provided by Mercer Advisors Insurance Services, LLC (MAIS), which places individual life, disability, long term care coverage, and property and casualty coverage through select insurance companies. Trustee services are offered through select third parties with which a client would sign an additional agreement, and additional fees may apply.