Over the past few weeks, the U.S. stock market has gone through an abrupt rotation out of the largest capitalization tech stocks and into small cap stocks. The financial media has dubbed this a “stock market rotation of historic proportions.”1

One way to size up this rotation: Since June, the stocks in the Russell 2000 Total Return Index have outperformed the stocks in the Russell 1,000 Total Return Index by around 600 basis points. This is a significant shift in such a short amount of time.

Why is this happening now?

There are likely a few factors behind the rotation happening now. First, early evidence is mounting that the Federal Reserve may be able to justify rate cuts later this year. The latest release of the Consumer-Price Index on July 11 came in lower than expected, and the latest jobs report, which came out July 5, showed the unemployment rate climbing up ever so slightly.

The Fed probably isn’t there yet. Inflation is still running a little hotter than the Fed prefers. The unemployment rate is still quite low. But the latest economic data is pointing in the direction that would eventually prompt the Fed to cut rates.

Expectations for lower interest rates disproportionately benefit the outlook for small cap companies. About one-third of the companies in the Russell 2000 have floating point debt, and around 40% of the companies are unprofitable.

This means that if interest expense comes down, some of these companies that are currently unprofitable should be able to lower their debt payments and return to profitability. This is a key part of what’s underpinning optimism about smaller cap companies that, until recently, had been laggards.

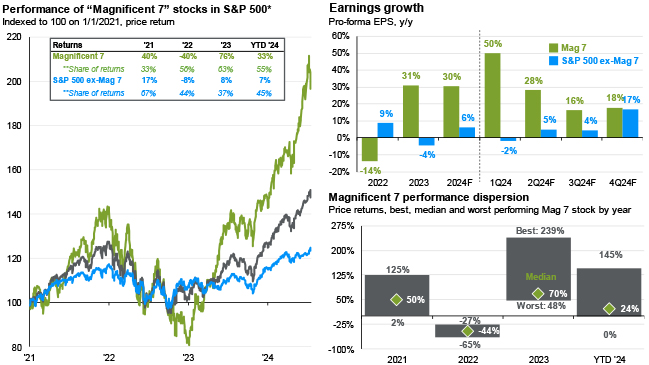

Next, for the Megacap tech stocks which had dominated the market for the past 18 months, earnings growth is expected to fall back in line. This septet of companies – dubbed the Magnificent Seven and consisting of Tesla, Nvidia, Alphabet, Meta (Facebook), Microsoft, Apple, and Amazon – had been outperforming the market.

According to JPMorgan data, the Magnificent Seven have climbed 33% so far this year. The other 493 companies in the S&P 500 are up just 7%. Just those seven companies are responsible for 55% of the market’s returns since 2021. (Chart below, on left)

*Magnificent 7 includes AAPL, AMZN, GOOG, GOOGL, META, MSFT, NVDA and TSLA. Earnings estimates for 2024 are forecasts based on consensus analyst expectations. **Share of returns represent how much each group contributed to the overall return. Numbers are always positive despite negative performance in 2022. Guide to the Markets – U.S. Data are as of June 30, 2024.

These returns have not been unwarranted. In the first quarter, the Magnificent Seven had year-over-year pro-forma earnings per share growth of 50%, compared to -2% for the rest of the S&P 500.

What matters now is expected earnings growth going forward. Here the outlook provided by JPMorgan’s Guide to the Markets is relevant. By the fourth quarter, they expect the year-over-year measure of earnings per share growth to be 18% for the Magnificent Seven, and 17% for the rest of the market. (Chart above, top right)

All of this leads to a thesis that small caps might outperform large caps, especially those major tech stocks which had such high valuations. We’re seeing this happen in real time.

What should investors do, if anything, about all of this?

This July’s market rotation illustrates several important aspects of our philosophy in constructing broadly-diversified and regularly-rebalanced portfolios. When a portfolio is broadly diversified across companies, it means that if seven companies have large gains like the Magnificent Seven, then they were already in the portfolio. Such portfolios already owned the winners. The episode also underscores why rebalancing is so important. When we regularly rebalance our portfolios, it means selling those assets that were leaders, and taking those profits, and then rebalancing into assets that have been laggards but may be poised to rise. Such rebalancing is a check against human instinct. It might feel more intuitive to hold onto our recent winners and unload our recent losers, but the history of investing shows this to be folly.

Key takeaways

Maintain a long-term perspective. It’s easy to get caught up in major market movements and wish you’d perfectly anticipated it. Market leadership unpredictably rotates, and all asset classes eventually have their day. Trying to time or guess tomorrow’s winners is a fool’s errand.

Stay diversified. Portfolios should already include at least market-weight allocations to small cap and value stocks. A well-diversified portfolio, by definition, already includes allocations to small cap, mega cap tech, and much more.

Systematically rebalance. Not all asset classes move in unison, and that’s a good thing. It’s how we helps smooth out the bumps in markets over time. Rebalancing a portfolio, by definition, sells recent winners and buys recent losers. A diversified portfolio that’s systematically rebalanced within and across asset classes, over the past year, would have been selling mega cap tech (which had outperformed small cap stocks) and buying small cap stocks. That means it should be well positioned for a period in which small caps stocks outperform big tech.

Your advisor can help determine how best to diversify your portfolio to suit your needs and goals in addition to answering your questions about market rotation. Not a Mercer Advisors client but interested in more information? Let’s talk.

[1] Langley, Karen. “A Stock-Market Rotation of Historic Proportions Is Taking Shape,” The Wall Street Journal, July 22, 2024.