Ready to learn more?

With the 2020 elections fast approaching, you may be wondering how presidential elections will affect your portfolio. The good news is, you’re not alone. There’s a widely held belief that elections influence stock market performance. This seems logical enough—elections can and do have implications for business, tax, and regulatory policies that invariably affect the economy and markets. Further, those with deeply held political beliefs like to think their chosen political party is “best” for markets. But to paraphrase a quote from Mark Twain, it’s not what we know that gets investors into trouble; it’s what we know for sure that just isn’t so. Despite what many of us want to believe, there’s no evidence that presidential elections or who occupies the White House have any effect on stock market returns.

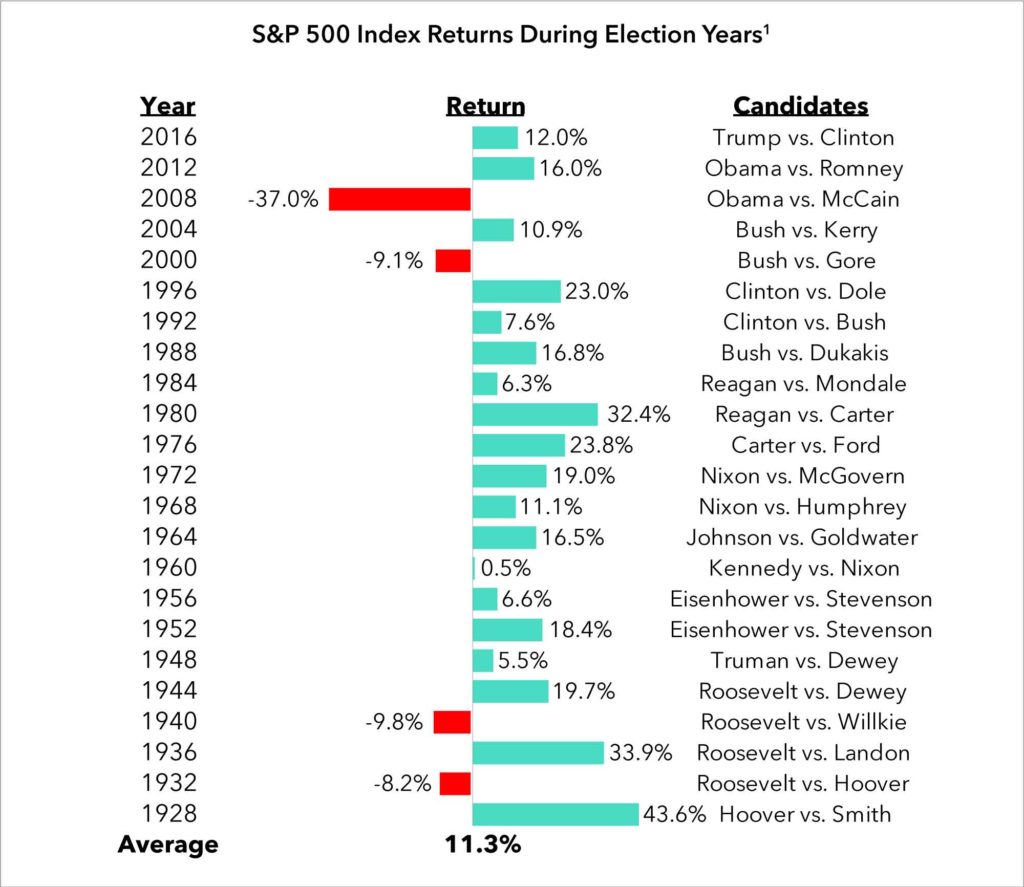

Since 1928, there have been 23 elections resulting in 14 different presidents. In in each of those years, the average return for the S&P 500 Index was 11.3%, a return that closely mirrors the average non-election year return of 11.8%. Further, returns were positive 87% of the time versus only 67% of the time in non-election years. Subsequently, there’s no evidence that presidential elections either negatively or positively influence year returns, but there is evidence that investors should remain invested in stocks during election years.

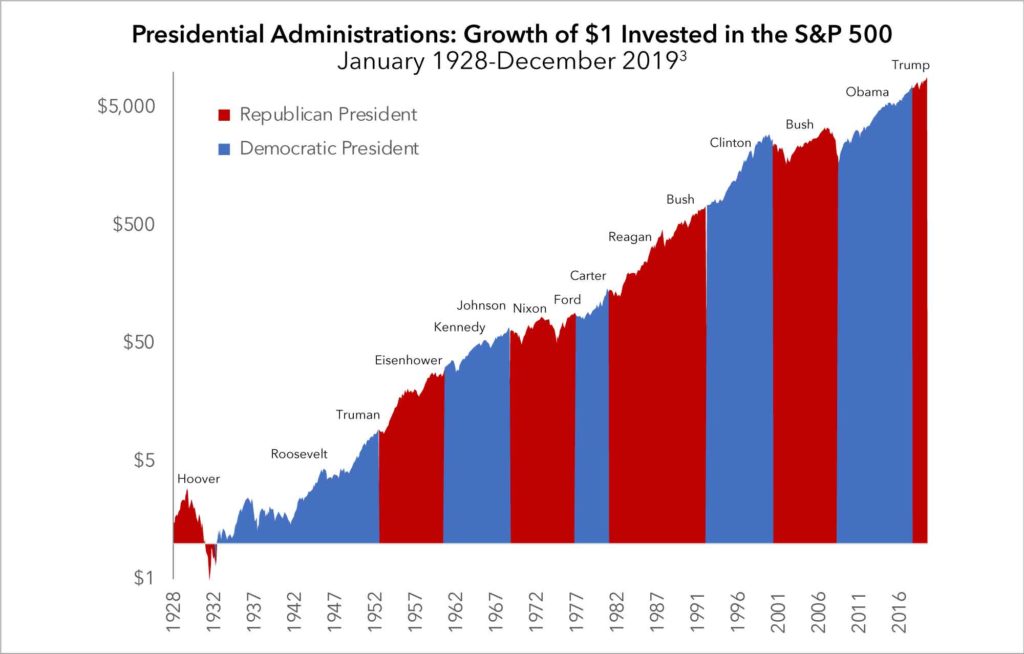

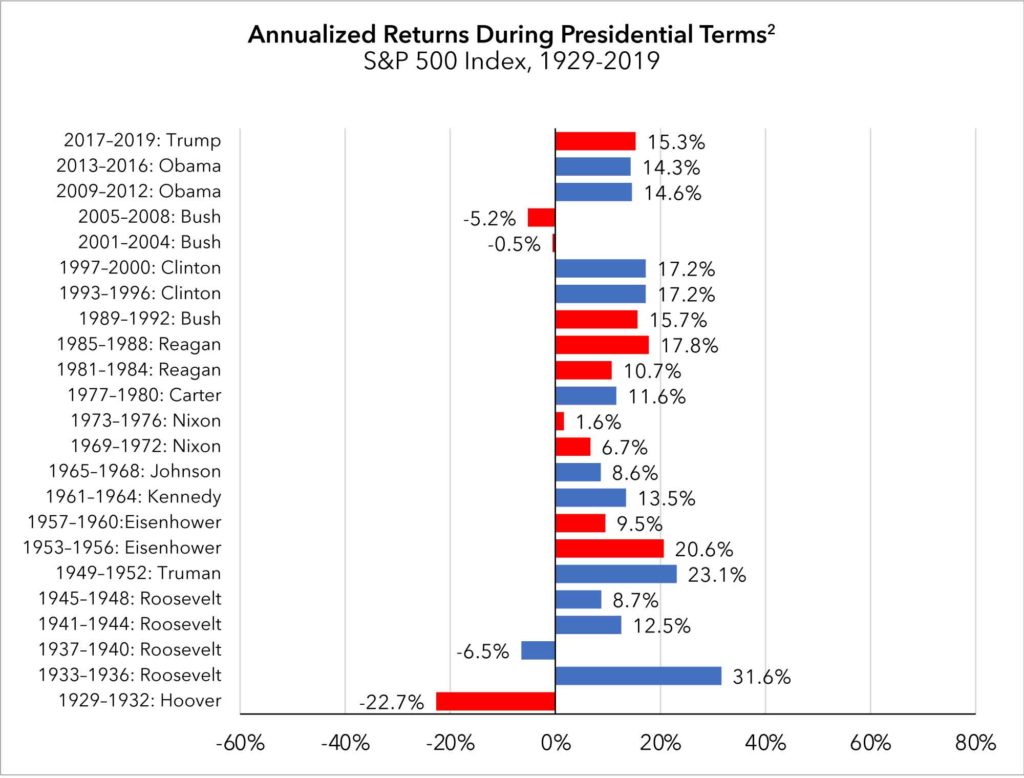

Since 1928, market returns under Democratic administrations have averaged 13.9% annually versus 6.3% annually under Republican administrations. For some investors, this is all the information they need; however, it’s important to realize that there’s a significant difference between simply describing historical results and drawing conclusions from historical results. To draw reliable conclusions from any data, a scientific approach would require the data to be statistically significant and definitionally precise. We’ll see in a moment that this data is lacking in both these areas. It’s also important to take into account whether other more complex factors might explain market returns under various administrations, such as Congressional control, an economic depression, or a sub-prime mortgage crisis. Subsequently, there are at least three major problems with drawing conclusions from this data:

First, the sample size is exceptionally small. We’ve had only 14 different presidential administrations since 1928; 7 Democrats and 7 Republicans (8 if we count President Ford as his own administration). Suffice it to say, we don’t have enough information to reliably draw any material conclusions. For example, had Gore won in 2000 instead of Bush, or had Republicans won in 1932 or 2009, the difference in average returns between the two parties goes away almost entirely (or even flips). My point isn’t to rewrite history, but to highlight just how sensitive the averages are to changes in only one or two data points.

Second, it’s exceptionally difficult, if not impossible, to draw any cause and effect relationships between a given political party and specific market returns because presidents and political parties are poor proxies for economic policies. For example, President Bill Clinton signed the North American Free Trade Agreement (generally viewed as pro-business) whereas President Trump killed consideration of the Trans-Pacific Partnership (a NAFTA-like free trade agreement) and erected a number of protectionist trade barriers (generally viewed as anti-business). Additionally, President John F. Kennedy cut taxes whereas President George H. Bush increased taxes. Even if political parties were reliable proxies for specific economic policies, it’s not even entirely clear which economic policy prescriptions are best for markets. Even professional economists often disagree.

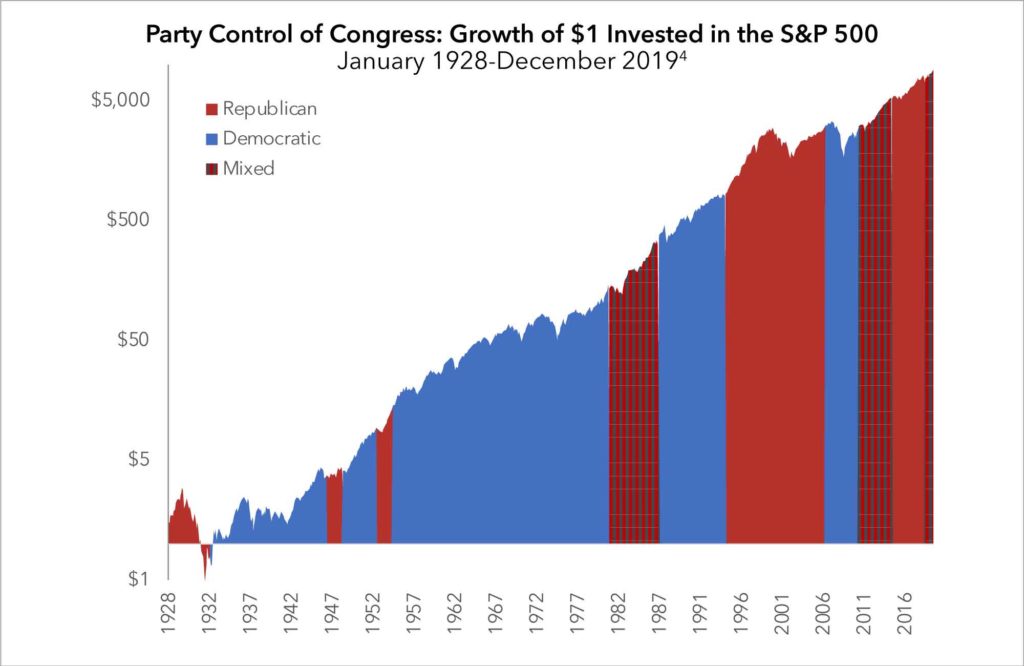

Finally, presidents don’t make and pass laws; Congress does. Laws are most often the result of political horse-trading; rarely does one party get everything it wants. For example, stock market returns were highest—15.1% annually—when Democrats occupied the White House and Republicans controlled Congress. Who owns these stellar returns, Congress or the White House? A further complication is that Congress consists of two chambers, the House and the Senate; as a result, Congress itself is often divided. These political realities only further aggravate attempts to draw cause-and-effect relationships between market returns, individual presidents, different combinations of Congressional control, or political parties.

Over the past 9 decades, we have had 14 different presidential administrations that saw hotly contested elections, several impeachments, multiple wars, a number of economic and geopolitical crises, and even the terrorist attacks of 9/11. Administrations, regardless of political party, have managed to work through these and a myriad of other challenges to our democracy and economic well-being. And, through it all, the S&P 500 has delivered a compound annual return of 9.9% to investors. Overall, markets were positive in 73% of all calendar years since 1928. The only reliable conclusion one can draw is that despite who occupies the White House, markets continue to be reliable venues for building wealth over time.