Roth IRAs were established in 1997 and named after former Delaware Sen. William Roth. These accounts were designed to be funded with after-tax dollars, unlike traditional IRA contributions which are funded with pre-tax money and often qualify for a tax deduction.

Roth IRA balances are not subject to taxation and all future withdrawals are generally tax-free. Withdrawals from a traditional IRA count as taxable income.

Roth IRA holders do not have to take a required minimum distribution (RMD) from their account each year. By contrast, the account holder of a traditional IRA must take a yearly RMD starting at age 73 (age 75 if born in 1960 or later).

Because of these key distinctions, Roth conversion strategies can be advantageous for people with large traditional IRA balances who expect to pay as much or more income tax in retirement as they are paying now.

One of the best times to convert IRA funds to a Roth IRA is during the “trough years.” This is the period after you retire but before RMD rules apply.

Advantages of a Roth IRA conversion

When making a Roth conversion, the tax is paid on retirement savings today, in exchange for tax-free growth for the future. As shown below, conversions during “trough years” can keep a person in a lower tax bracket. This can help avoid a larger tax bill. It can also help keep future RMDs from facing higher tax rates.

| Implementing Systematic Roth Conversions

Remain in lower tax brackets, avoiding higher tax rates today, while helping to ensure your future RMDs won’t be subject to higher tax rates when you retire.

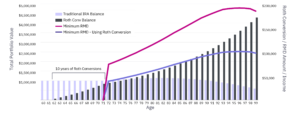

Performance quoted is past performance and is not indicative of future results. For Illustrative Purposes Only. Source: www.kitces.com. Long-Term Value of Proactive Roth Conversions Converting annual growth of IRA reduced future required minimum distributions.

Performance quoted is past performance and is not indicative of future results. Assumes IRA balance of $1M at age 60 with 6% growth year-over-year. Roth conversions occur from 62 years old to 72 years old and assumes all IRA growth is converted to the Roth on an annual basis. *For Illustrative Purposes Only. |

As a result of converting $60,000 — equivalent to 6% annual growth in the traditional IRA balance — to a Roth IRA each year from ages 62 to 72, the retiree in this hypothetical example would have a balance of more than $2 million at age 85.

This is possible because the person can let their Roth IRA grow tax-free while relying on RMDs from their traditional IRA as income. If left untouched, the Roth IRA balance in this example could potentially reach nearly $5 million by the time the retiree was 100.

Roth conversion benefits for inherited accounts

For non-spouse beneficiaries who inherit an IRA after the owner dies, the SECURE Act applies. As of Jan. 1, 2020, the Act requires the inherited IRA balance to be distributed by the end of the 10th year. The 10-year period starts the year following the original owner’s death. Some exceptions to inherited IRA rules may apply.

Roth conversion tax planning helps ensure that the inherited retirement account balance is tax-free — relieving beneficiaries of the taxable income impact from the 10-year withdrawal requirement.

Does a Roth conversion make sense in 2026?

It does, in specific situations. Let’s say you have a traditional IRA that you’ve been paying into for years. Once you retire, you and your spouse start drawing Social Security within one year. You also have income from savings and investment account withdrawals.

This mix may push you into a higher tax bracket. Then, any IRA withdrawals may be taxed at a higher rate. Converting a traditional IRA to a Roth IRA can help reduce your overall tax burden.

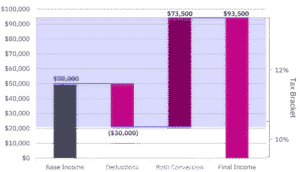

Practical Example for 2026

- Let’s look at an example of a married couple with a base income of $110,000.

- When they start RMDs at age 73, they may add $60,000 to their other income. Instead of waiting to start RMDs, they can move that $60,000 to a Roth IRA during their “trough years.” Their taxable income is still going to be $170,000 (which falls within the 22% bracket), but that money can continue to grow tax-free. It will also be unaffected by future required distributions.

- By strategically managing conversions to stay within the 22% or 24% bracket, they can avoid being pushed into the 32% bracket or higher in future years, when RMDs become mandatory.

Key considerations when planning conversions

When planning Roth conversions for 2026, consider:

- Current vs. future tax rates: If you expect to be in a higher tax bracket in retirement, converting now at a lower rate makes sense. Also, consider the “widow’s penalty” if your spouse is much younger and/or healthier and will file taxes as a single filer after you pass away.

- Income timing: The period between retirement and age 73 (when RMDs begin) often presents the best opportunity for conversions.

- Medicare premiums: Higher income from conversions may affect Medicare Part B and Part D premiums (IRMAA), so plan conversion amounts carefully. However, higher income from RMDs in later life could cause permanently higher premiums. Consider taking an IRMAA hit in a few years rather than paying it from age 73 until death.

- State taxes: Consider your state’s tax treatment of Roth conversions, especially if you’re planning to relocate in retirement.

- Long-term growth potential: The longer your money has to grow tax-free in a Roth IRA, the more advantageous the conversion becomes.

Taking action

If you’re considering a Roth IRA conversion, it’s important to weigh the current factors that apply to your specific situation as well as how things may change during your retirement. Strategic conversion planning requires careful analysis of:

- Your current and projected future tax brackets

- The IRA conversion timing and amount — to optimize tax efficiency

- Coordination with Social Security claiming strategies

- Impact on Medicare premiums and other income-tested benefits

- Estate planning objectives for your beneficiaries

For personalized retirement tax planning advice tailored to your situation, contact your wealth advisor. Not already a Mercer Advisors client?

-

No, Roth conversion recharacterizations were eliminated by the Tax Cuts and Jobs Act of 2017. Once you complete a Roth conversion, it is permanent and cannot be reversed or “undone.” This makes careful planning essential before executing a conversion. You should be confident in your decision and ensure you have funds available outside the IRA to pay the conversion taxes.

-

The tax you pay depends on the amount converted and your total taxable income for the year. The converted amount is added to your ordinary income and taxed at your marginal rate.

For example, if you’re married filing jointly with $150,000 in income and convert $50,000, that conversion would be taxed at the 22% rate (based on 2026 tax brackets), resulting in approximately $11,000 in additional federal tax. Additionally, you would be just below the IRMAA threshold so you would not pay any additional Medicare premiums. Strategic planning can help you convert amounts that will keep you in your current or next-lowest bracket — rather than pushing you into significantly higher rates.

-

The optimal age for a Roth conversion is typically during your “trough years” – the period between retirement and age 73 when RMDs begin. This window allows you to convert at potentially lower tax rates before required distributions push you into higher brackets.

However, conversions can make sense at any age if you expect to be in a higher tax bracket in the future. Consider factors such as current income, retirement timeline, and long-term tax projections when determining the best timing for your situation.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. Hypothetical examples are for illustrative purposes only.