Taking a systematic, rules-based approach to investing within asset classes is a foundational pillar of our investment philosophy at Mercer Advisors.

In this piece, we explain how we execute this pillar via factor investing, an academically rigorous and peer-reviewed systematic approach that identifies assets with quantifiable characteristics, or factors, that are associated with higher expected returns.

Why active investing often disappoints as a default

Many investors still fall victim to the thinking that the key to successful investing is great stock selection and market timing. This fallacy is very much on display throughout the financial press and television. The notion that a financial virtuoso can outperform the market through hard work, raw talent, and superior intellect is appealing.

In practice, this is difficult to do consistently.

Decades of research suggests that, net of fees, most active approaches to portfolio management struggle to consistently justify their cost. As Mark Carhart’s seminal 1997 paper “On Persistence in Mutual Fund Performance” in the Journal of Finance put it: “The results do not support the existence of skilled and informed mutual fund portfolio managers.”

Empirical analysis of active manager performance since Carhart’s paper reinforces this conclusion. At any given point in time, some fund managers have had a good year. But over time, outperformance does not persist. Table 1 shows how many fund managers in a given category outperformed their benchmark. For example, only 11% of large-cap fund managers outperformed the S&P 500 over the past five years,. Over a 15-year window, not a single one of these major equity fund categories has had more than 16% of fund managers who have beaten their index. Those are exceptionally poor odds.

Table 1: Percentage of funds that outperformed their benchmark, as of Dec. 31, 2025

Active Fund’s Success Rate |

||||

Equity Fund Category |

Comparison Index |

1 YR (%) |

5 YR (%) |

15 YR (%) |

| All Large-Cap | S&P 500® | 21.2% | 11.0% | 10.1% |

| All Domestic | S&P Composite 1500® | 20.2% | 8.5% | 6.9% |

| All Multi-Cap | S&P Composite 1500® | 32.0% | 10.0% | 7.8% |

| All Small-Cap | S&P SmallCap 600® | 59.4% | 37.3% | 10.1% |

| All Mid-Cap | S&P MidCap 400® | 44.6% | 27.7% | 15.5% |

| Global Funds | S&P World (USD) | 24.3% | 5.2% | 4.4% |

| Emerging Markets Funds | S&P Emerging Plus | 47.0% | 26.5% | 10.4% |

| International Funds | S&P World Ex-U.S. Index (USD) | 36.8% | 20.0% | 7.3% |

Source: S&P Dow Jones Indices

The consequences of choosing a lagging active manager can be meaningful: Roughly 40% of active managers from a decade ago no longer exist today, and among those that survive, excess returns have tended to be negative according to Morningstar, which measures the performance of active funds versus their passive peers across investment categories.

The rise of index investing

The poor results of many active managers helped accelerate the rise of passive (index) investing, which over the long run has often delivered competitive returns at lower costs than traditional active management. There’s a lot to like about index investing: It offers broad diversification, for example, by owning the entire S&P 500 rather than trying to pick winners and losers. Why choose between betting on blackjack, poker, and roulette when you can instead just buy the entire casino? After all, the house always wins.

Because index investing is a strong baseline, before going beyond it, investors should be confident of two things:

- Rigorous, peer-reviewed academic data supports the existence of significant and persistent long-term returns associated with index investing.

- Economic rationale supports why index investing works.

Factor investing is often described as a “third way” because it harnesses the advantages of and serves as a disciplined complement to broad-market indexing.

Figure 1. Factor investing is the third way

Factor investing relies on robust, peer-reviewed empirical research into the characteristics of stocks that have earned persistent premiums across markets and over time.

Factors are transparent and quantifiable. They use data pulled from publicly available financial statements, such as a firm’s balance sheet, income statement, or statement of cash flows. This means that factor investing can be done systematically and transparently.

In equities, the factors we target in our portfolios include value, quality, momentum, and size. We start with an index of stocks and add tilts to stocks that exhibit specific factor characteristics. Furthermore, each factor has a commonsense explanation.

- Value: Stocks with low prices relative to their fundamental value, such as book value of equity. These are companies that are “on sale.”

- Quality: Stocks with stable earnings and consistent growth. These are companies with stable business models.

- Momentum: Stocks that have outperformed in the recent past relative to their peer group. This factor captures trends developing in the market but in a systematic way rather than chasing gut feelings about companies or sectors.

- Size: Stocks with smaller market capitalizations. This factor captures nimble companies that, on average, can pivot or change more quickly.

The evidence-based approach

Identifying the most significant factors has been the work of serious and cutting-edge financial and economic research since the 1950s:

- Harry Markowitz developed a mathematical theory for diversification with his 1952 Modern Portfolio Theory. (Markowitz received the 1990 Nobel Memorial Prize in Economic Sciences, which he shared with William Sharpe and Merton H. Miller.)

- William Sharpe defined the equity premium with his 1963 Capital Asset Pricing Model. (Sharpe received the 1990 Nobel Memorial Prize in Economic Sciences, which he shared with Markowitz and Miller.)

- Eugene Fama and Kenneth French’s research found consistent outperformance in several factors, such as market, value, small cap, profitability and quality, and investment over decades of work. (Fama shared the 2013 Nobel Memorial Prize in Economic Sciences with Lars Peter Hansen and Robert J. Shiller for their work developing the Efficient Market Hypothesis.)

- Robert Novy-Marx found in 2012 that a four-factor model including market, value, momentum, and profitability factors had significant outperformance.

- Sunil Wahal found in 2020 that value and profitability factors work not only domestically, but also in international markets.

“Gas station sushi”: an analogy to understand the multi-factor approach

Rather than investing in only one factor, the evidence suggests the best approach is to balance factors together. We use the following analogy to explain why: If you’re looking only at quality, you might buy sushi from an expensive, high-end restaurant in San Francisco or Tokyo. If you were looking only at value, you might choose to buy inexpensive sushi at a local gas station. To avoid spending $1,000 on sushi or getting food poisoning, you take a balanced approach. Balancing multiple factors is aptly called multi-factor investing.

Factor investing in the long run

No strategy will win every year — or even every five years. A long-term investor, however, should focus on the probability of success over time.

With traditional active management, the probability of outperformance decreases with time (we see this in Table 1). With factor investing, however, the probability of outperformance increases with time.

Figure 2: Factors outperforming over time

Source: Dimensional Fund Advisors LP

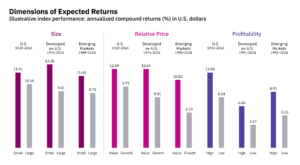

As shown in Figure 2, small cap has beaten large cap 78% of the time over any 15-year period dating back to 1927. Similarly, value has beaten growth 86% of the time, and high profitability has beaten low profitability 98% of the time over any 15-year period.

This has translated to persistent outperformance across factors and across U.S. markets, developed markets (excluding the U.S.), and emerging markets, as shown in Figure 3.

Figure 3: Magnitude of factor outperformance

Source: Dimensional Fund Advisors LP

Key takeaways

- As fiduciaries, we take an evidence-based approach to investing. The evidence suggests that traditional active management is inferior to multi-factor approaches.

- Passive investing offers broad diversification and low fees, which is a great starting point. Investors should move beyond passive investing when rigorous, peer-reviewed academic data supports the existence of strategies that can deliver persistent improved returns.

- Factor investing is a systematic, rules-based approach that we use to guide us in diversifying within asset classes. Systematically tilting portfolios toward factors is a technique that has well-demonstrated improvement in expected returns while maintaining transparency and cost-discipline.

More insights are available from our CIO and investment team.

Not a Mercer Advisors client but interested in more information?

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.