A financial plan isn’t just about numbers — it’s about feeling empowered and confident while also helping to protect your family’s security. Even with significant wealth, the uncertainty of “Do we have enough?” can quietly follow you.

A plan can clear that fog. It shows you exactly where you stand, how long your resources can support your lifestyle, and how confidently you can care for the people who matter most.

A solid plan helps you understand how to safeguard your family’s future, whether that means funding education, covering health care needs, or leaving a meaningful legacy. It also helps you enjoy the life you’ve worked for without second‑guessing every decision.

You’ll see whether you can retire earlier, spend more freely, or simplify complex financial choices. Meeting with an advisor now can turn guesswork into clarity, so you and your family can move forward with confidence, stability, and a stronger sense of control over the years ahead.

This guide breaks down the elements of a strong financial plan in a simple, approachable way, giving you clear steps you can act on right away. Take a few minutes to explore it, and you’ll see how small, meaningful actions today can lead to financial clarity and reassurance.

Did you know?

- Only 31% of Americans, ages 21 to 75, have determined their financial goals and have documented them in a formal plan.1

- Only 20% of Gen Xers (ages 45-60) have enough emergency savings to cover six month’s expenses or more.2

- Nearly 100% (94%) of households advised by a CFP® professional are confident in their ability to achieve their financial goals.3

The Key Parts of a Solid Financial Plan

Every family’s situation is unique, but a solid financial plan is built on a few essential building blocks. These pieces work together to help create the stability and security every family deserves.

- Cash flow: How your money moves in and out

- Net worth: What you own vs. what you owe

- Taxes: Your current tax picture

- Investments: How your money is growing

- Retirement planning: Your future income strategy

- Estate planning: Protecting your wishes and your family

- Insurance: Your financial safety net

This guide walks you through each of these core elements in a clear, approachable way, helping you understand where you are today and where you may want to go next. It’s designed to help you feel confident, informed, and in control — so you can make decisions that support your goals and your family’s future.

If you’ve been considering creating a financial plan, now could be a good time to start.

Cash Flow: Identifying How Your Money Moves

Cash flow is more than a budget — it’s a clearer picture of how your money actually works for you day‑to‑day and month‑to‑month. It’s the ongoing flow of income and expenses. When you understand that flow, you gain one of the most powerful tools for building long‑term financial stability.

When you get intentional about how your money moves, you can start using it to support your goals instead of feeling controlled by it.

A few helpful habits:

- Look at what comes in and what goes out

- Identify your essential vs. flexible spending

- Automate savings to make progress effortless

- Make small adjustments where they matter

Remember to build an emergency fund

A strong cash flow plan includes preparing for the unexpected. Set aside three to six months of living expenses in a separate, easily accessible account.

When your cash flow works

Cash flow plays a key role in your financial plan. With a healthy, intentional approach to how money comes in and goes out, you’re better positioned to:

- Build savings consistently

- Invest with confidence

- Manage unplanned expenses

- Reduce reliance on debt

- Support your long‑term goals

When you get your cash flow working for you, it becomes easier to make progress in every other part of your financial plan.

Sample worksheet

Here’s a simple snapshot of what monthly cash flow categories typically look like.

Cash Flow Tracker — Month:

| Income | Amount |

|---|---|

| Paycheck 1 | |

| Paycheck 2 | |

| Bonus/Commission | |

| Side Income | |

| TOTAL INCOME | — |

| Fixed Expenses | Amount |

| Rent/Mortgage | |

| Utilities | |

| Insurance (Auto/Home/Life) | |

| Phone/Internet | |

| Childcare/School | |

| Transportation (Loan/Transit) | |

| Subscriptions/Memberships | |

| Other Fixed | |

| TOTAL FIXED | — |

| Variable Expenses | Amount |

| Groceries | |

| Dining & Coffee | |

| Gas & Rideshare | |

| Personal Care | |

| Clothing | |

| Entertainment | |

| Gifts/Donations | |

| Miscellaneous | |

| TOTAL VARIABLE | — |

| Savings & Debt | Amount |

| Emergency Fund | |

| Retirement (401k/IRA) | |

| College/529 | |

| Brokerage Savings | |

| Extra Debt Payment (Credit Card) | |

| Extra Debt Payment (Loan) | |

| Other Savings/Debt | |

| TOTAL SAVINGS/DEBT | — |

Net Worth: A Snapshot of Your Financial Health

To determine your net worth, you’re simply creating a clear picture of what you own and what you owe. It’s the difference between your total assets and your total liabilities.

Knowing your net worth gives you a clear baseline to help improve from.

Sample worksheet

List your assets and liabilities to calculate your net worth.

| Category | Description | Asset Amount ($) | Liability Amount ($) |

|---|---|---|---|

| Cash & checking | |||

| Savings & money market | |||

| Brokerage (taxable investments) | |||

| Retirement accounts (401(k), 403(b), IRA, Roth IRA) | |||

| Education account (529) | |||

| Real estate (primary home) | |||

| Real estate (other than primary home) | |||

| Home equity line, lines of credit, or loans | |||

| Personal property (cars, jewelry, etc.) | |||

| Credit cards | |||

| Student loans | |||

| Auto loans | |||

| Other assets or liabilities | |||

| Totals | — | — | |

| Net Worth = Total Assets − Total Liabilities | — | |||

Review it regularly

Regularly tracking your net worth (once or twice a year) helps you understand your progress toward long‑term goals and provides insights into your overall financial health.

Tracking it helps you:

- See where you’re making progress

- Spot debts worth tackling

- Confirm your savings are building real growth

Over time, you want to see liabilities shrinking and assets growing. But it’s also normal for net worth to fluctuate based on markets, savings patterns, or life events.

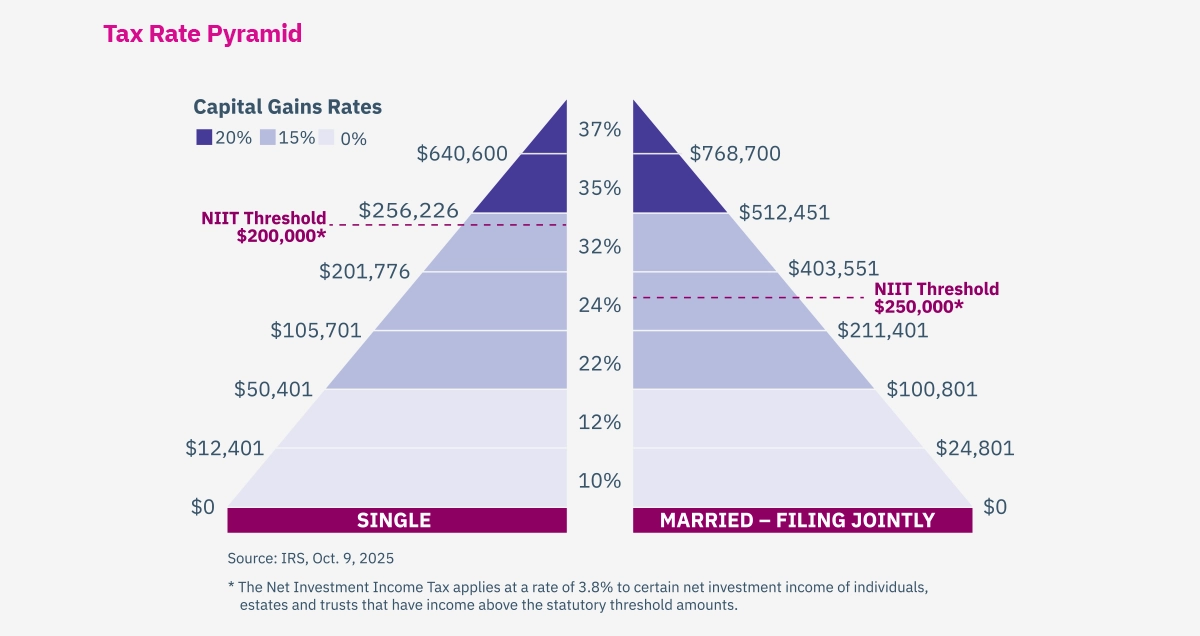

Taxes: Keeping More of What You Earn

Taxes affect almost every financial decision. You don’t need to know every detail, but you should have a general understanding of your tax bracket and options.

Here are some helpful things to keep in mind.

Current tax bracket

Your tax bracket is the rate applied to the last dollar you earn — not all your income. Because the U.S. uses a progressive system, income is taxed in layers, so even if you’re in a higher bracket, much of your income may still be taxed at lower rates.

Knowing your bracket helps you understand:

- The value of deductions

- Whether pre‑tax or Roth contributions are better

- When shifting income or expenses might help

Pre‑tax vs. Roth contributions

Using a mix of both may be able to help you manage taxes over time.

- Pre‑tax: Lowers taxable income today; taxes are paid when you withdraw in retirement. Works well if you expect to be in a lower bracket later.

- Roth: Taxes are paid now; qualified withdrawals (including growth) are tax‑free in retirement. Helpful if you expect higher income in the future or want more flexibility later on.

Credits or deductions

Credits and deductions can both reduce your tax bill, but in different ways. Understanding which ones apply to you helps ensure you keep more of what you earn.

- Deductions lower taxable income (pre‑tax 401(k), IRA, or HSA contributions).

- Credits reduce the tax you owe dollar‑for‑dollar (child tax credit, education credits, energy‑efficient home credits).

Timing income or expenses

The timing of income and certain expenses can influence how much tax you owe.

Examples:

- If you expect lower income next year, delaying income could keep you in a lower bracket.

- If income may rise, accelerating deductions, like charitable gifts or property taxes, may help this year.

- Timing IRA withdrawals can sometimes help retirees stay within lower brackets.

- Investors may consider timing gains and losses to offset each other.

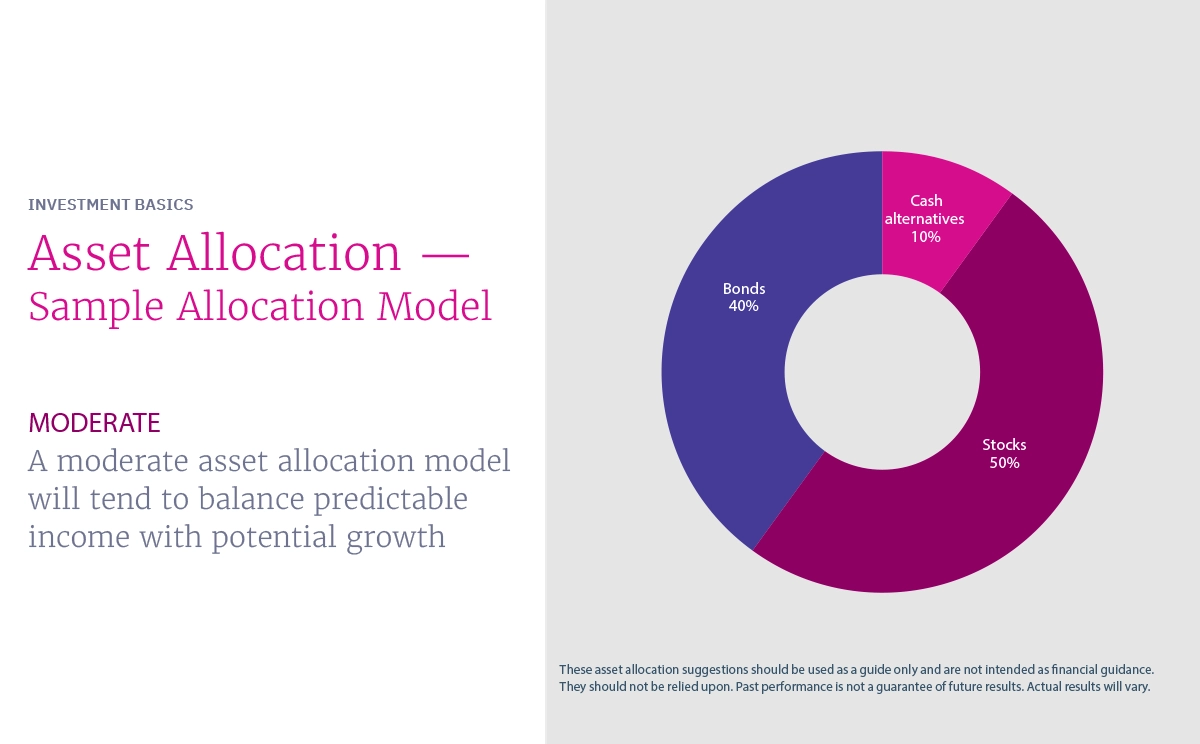

Investments: Making Sure Your Money Is Working The Right Way

When you check in on your investments, a few simple questions can help you stay on track and make sure your portfolio still fits your life today.

Is your mix of stocks, bonds, and cash appropriate?

Your investment mix (or “asset allocation”) should match your goals and how long you plan to invest. Reviewing this helps you stay balanced by not taking too much risk but not being too conservative either.

Does your risk level feel comfortable?

Market ups and downs can feel different at different stages of life. Make sure the level of risk in your portfolio still lines up with how much volatility you’re comfortable with.

Have your goals or timelines changed recently?

If life plans have shifted — like moving sooner, changing careers, or adjusting retirement timing — your investments may need a refresh. Aligning your portfolio with your current goals keeps your strategy focused and intentional.

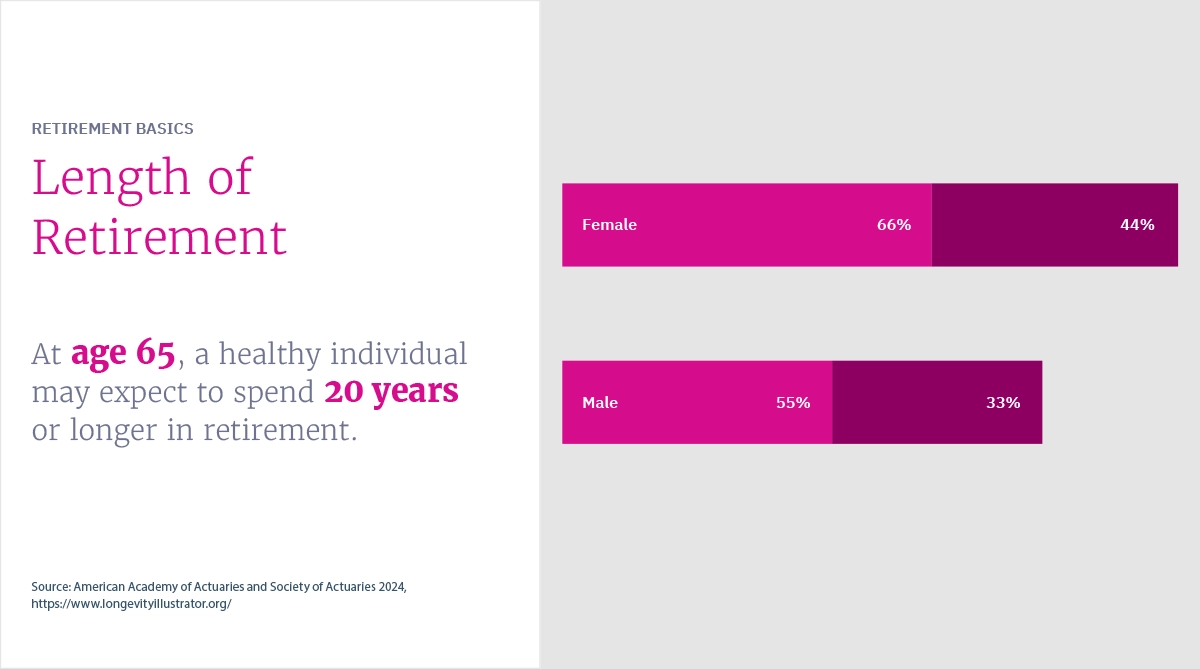

Retirement Planning: Preparing for the Future You Want

Retirement planning doesn’t need to feel overwhelming. A few thoughtful check‑ins can help you see whether you’re moving steadily toward the lifestyle you want later on.

Are you saving consistently?

Even small, steady contributions can grow significantly over time. Consistency matters more than perfection.

Do traditional, Roth, or mixed contributions make sense?

Traditional (pre‑tax) and Roth (after‑tax) contributions affect your taxes differently now and in retirement. Choosing the right mix can help you manage taxes today and build flexibility for the future.

How much future income will you need?

Think about what you want your retirement to look like — travel, hobbies, family time — and what it may cost. Having a rough estimate helps you know if you’re on track.

How might Social Security fit in?

Social Security is just one piece of your retirement income. Understanding when you plan to claim benefits can help clarify how much additional savings you’ll need to support your lifestyle.

Estate Planning: Protecting the People You Love

Estate planning is really about ensuring your wishes are honored and your family is supported if something unexpected happens.

- Revocable living trust with a pour‑over will, or a last will and testament: A will lays out how you want your assets distributed, names guardians for minor children, and appoints someone to manage your estate. A pour‑over will works alongside a trust by moving any remaining assets into the trust when you pass. A revocable living trust gives you flexibility to manage your assets during life and after death, and it helps your estate avoid probate — the often lengthy, public court process for validating a will.

- Health care power of attorney and living will (advance care directive): A health care power of attorney lets you choose someone you trust to make medical decisions if you’re unable to. A living will outlines your preferences for medical treatment, especially near the end of life. Together, these documents help ensure your wishes are honored and decision‑making is easier for loved ones.

- HIPAA authorization: A HIPAA authorization gives your chosen person permission to access your private medical information. This helps them communicate with doctors, make informed decisions, and even manage medical bills if you’re unable to yourself.

- Financial powers of attorney: Financial powers of attorney allows someone you trust to handle day‑to‑day financial matters on your behalf. You can tailor this document to grant as much or as little authority as needed, and for the timeframe that feels right for you.

- Irrevocable trusts: An irrevocable trust can help reduce estate taxes, protect assets from creditors, and ensure money is distributed under specific conditions. It can also support long‑term care planning while helping preserve eligibility for certain government benefits.

Insurance Considerations: Are you Properly Covered?

Insurance protects your family, your income, and your assets. Adequate coverage reinforces the strength of your overall financial plan.

Life insurance

Life insurance provides financial support to your loved ones if you pass away, helping cover expenses like income replacement, debts, or future goals. It’s a simple way to protect your family’s financial stability.

Disability insurance

Disability insurance replaces part of your income if an illness or injury keeps you from working. It helps ensure you can continue covering essential expenses during unexpected setbacks.

Long‑term care coverage

Long‑term care insurance helps pay for ongoing support — like in‑home care, assisted living, or nursing care — if you need help with daily activities later in life. It can ease the financial burden on both you and your family.

Homeowners, auto, and umbrella insurance

Homeowners and auto insurance protect your property, vehicles, and liability if something goes wrong. An umbrella policy adds an extra layer of coverage, helping safeguard your assets in the event of major accidents or unexpected claims.

Ready to Create a Financial Plan of Action?

We offer comprehensive wealth management through a family office-like structure, bringing together expertise in financial planning, investment management, tax planning and preparation, estate planning, insurance solutions, and more into one integrated offering.

For 40 years, Mercer Advisors has been trusted to help families amplify and simplify their financial lives.

As a fiduciary, we are obligated to always operate in your best interest.

1 “2025 Financial Planning Longitudinal Study.” Certified Financial Planner Board of Standards Center for Financial Planning, Inc., 2026.

2 “Bankrate’s 2026 Emergency Savings Report.” Bankrate, Jan. 21, 2026.

3 “Charles Schwab 2025 Modern Wealth Survey.” Charles Schwab & Co., Inc., July 2025.

“Mercer Advisors” is a brand name used by several affiliated legal entities owned by Mercer Advisors, Inc., including, Mercer Global Advisors, Inc., an SEC registered investment adviser providing investment advisory and family office services; Mercer Advisors Private Asset Management, Inc., an SEC registered investment adviser providing discretionary investment management services to affiliated private funds; Mercer Advisors Tax Services LLC, a tax services and accounting firm; Heim, Young and Associates, Inc., (MA Brokerage Solutions) a broker/dealer, member FINRA/SIPC; and Mercer Advisors Insurance Services, LLC (MAIS) an insurance agency.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. Hypothetical examples are for illustrative purposes only.