When you’re focusing on building wealth, insurance can feel like a task already handled — something you set up years ago, then filed away and rarely revisit. But if your insurance strategy isn’t connected to your overall wealth plan, there’s a possibility that important gaps exist. And those gaps may not surface until you need the coverage most.

Mercer Advisors takes a distinct approach. Rather than treating insurance as a stand-alone product category, we integrate insurance planning directly into your comprehensive financial picture alongside investment management, tax strategy, and estate planning. The result is a coordinated strategy designed to reflect your goals, your family’s needs, and the full complexity of your financial life.

Why integrated insurance planning matters

It’s common to accumulate insurance policies over time, such as life coverage from an employer, an auto policy, a homeowners plan, or perhaps a disability policy from a previous job. Each was likely selected in a moment of need, often through a different provider, and is rarely reviewed in relation to the others, complicating an uncoordinated effort.

That fragmented approach can create unintentional risk. A gap in a policy could undermine the protection you believed you had. Standard homeowners and auto policies, for example, carry liability limits that may not be adequate if a serious accident or lawsuit results in damages that exceed those limits.

Asset protection planning requires more than simply having coverage. It requires having the right coverage, in the right amounts, coordinated across your entire financial plan.

What a coordinated insurance review looks like

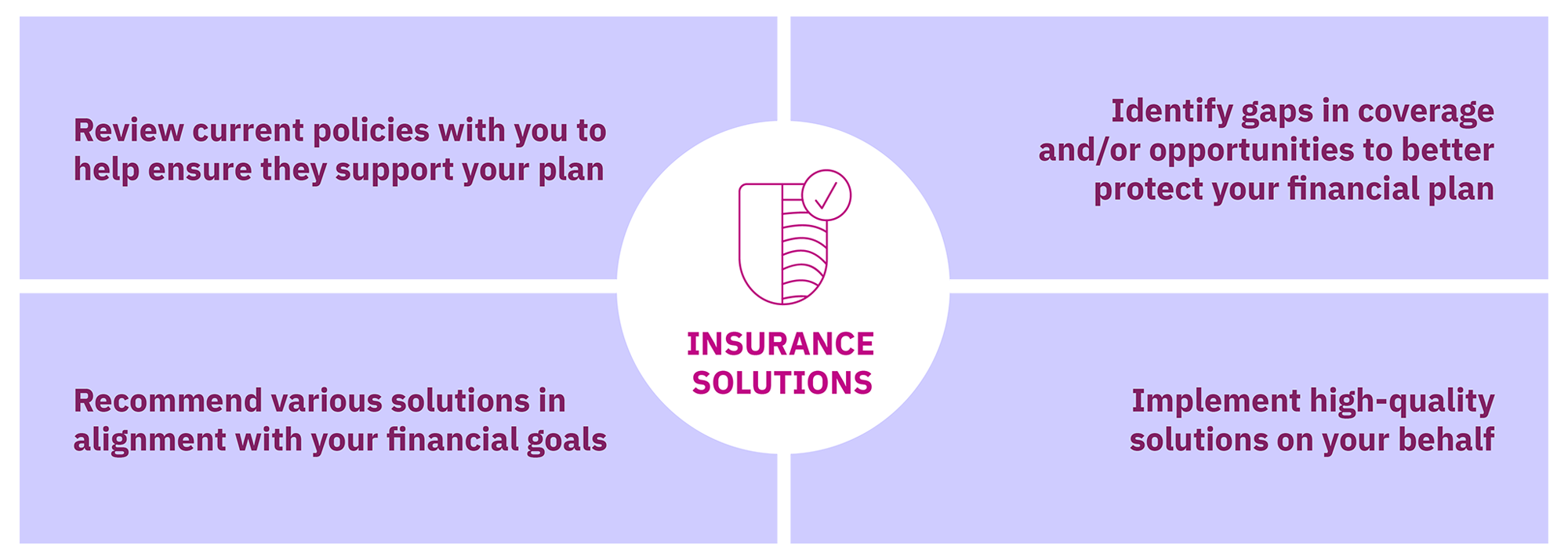

At Mercer Advisors, your insurance planning begins with your wealth advisor, who works directly with our internal Insurance Solutions Team. Together, they conduct a thorough review of your existing policies — examining what you have, what it covers, how it fits your current financial goals, and where potential gaps may exist.

This review is comprehensive by design. It considers:

- Whether your current policies align with your estate planning goals.

- Whether you are using life insurance effectively as a wealth transfer or legacy tool.

- Whether your liability coverage is calibrated to your current asset base.

- Whether disability and long-term care policies adequately protect your income and savings.

- Whether high-value assets like real estate, collections, recreational vehicles, or business interests are properly insured.

If your existing coverage is optimal, no changes are necessary. If it isn’t, our insurance specialists identify options, evaluate them against your broader wealth plan, and present a clear recommendation. Every decision is yours to make. Our Insurance Solutions Team is designed to educate.

The role of insurance in wealth preservation

Insurance isn’t just a safety net — it’s a strategic tool in long-term wealth preservation and cashflow protection. For those who have built meaningful assets, several types of coverage deserve particular attention.

Life insurance as a wealth transfer tool

Permanent life insurance can play an important role in estate planning. It offers liquidity to help cover estate taxes, potentially eliminating the need for heirs to liquidate investments or real estate at an inopportune time. It can also be used to leave a legacy to the people or organizations that matter most to you. Because tax consequences vary significantly depending on how a policy is structured, coordination with your tax and estate planning team is essential.

Disability insurance as income protection

Your ability to earn income is one of your most valuable assets. Disability insurance protects that earning power if illness or injury prevents you from working. A gap in coverage can put long-term financial plans at serious risk if the unexpected occurs.

Umbrella insurance as a liability shield

Even if you have comprehensive auto and homeowners policies, you can face liability exposure that exceeds standard policy limits. If a judgment exceeds your coverage, creditors may pursue your personal assets. Personal umbrella insurance provides an additional layer of protection, which is especially important as litigation costs rise and digital activity and social media continue to expand the definition of personal liability risk.

Long-term care coverage

As the cost of professional caregiving continues to increase, planning for potential long-term care needs is an important component of protecting accumulated savings.

Whether through a traditional long-term care policy or a hybrid life insurance solution with a long-term care rider, the right solution depends on your age, health, financial goals, and how this coverage fits into your overall wealth management strategy.

Why one team can make the difference

Working with a unified team that coordinates insurance alongside your investments, taxes, and estate plan can change what’s possible. Your wealth advisor doesn’t know just your portfolio — your wealth advisor knows your full financial picture. That context shapes every insurance recommendation.

When tax strategy and insurance planning are considered together, it becomes possible to structure life insurance coverage in ways that can reduce estate tax exposure. When estate planning and liability coverage are reviewed in tandem, this helps ensure that trusts, property holdings, and other assets are properly protected. Many advisors working in silos, without that broader context, may miss these connections entirely.

Mercer Advisors also maintains working relationships with dozens of highly-rated insurance carriers. That means our Insurance Solutions Team can assess options from multiple providers to identify coverage that fits your situation. And because we use advanced insurance planning tools, we can model potential outcomes and illustrate how different coverage scenarios interact with your broader wealth plan.

Keeping your coverage current

Your insurance needs aren’t static. As your wealth grows, your family changes, and your goals evolve, your coverage should too. We recommend an annual insurance review to make sure your protection remains aligned with your life. During that review, we’ll examine whether policy goals remain valid, whether beneficiary designations are current, whether coverage limits reflect your current exposure, and whether any lapses or premium changes need to be addressed.

Insurance planning that keeps pace with your financial life is insurance planning that can work effectively.

Bottom line

If your insurance policies were put in place separately from your financial plan, it’s possible that they may not be working together as effectively as they could. Mercer Advisors brings insurance planning into the same conversation as your investments, taxes, and estate strategy — so every piece of your financial life is designed to be protected, coordinated, and working toward your goals.

Ready to see how your insurance coverage fits your broader wealth plan?

Contact a Mercer Advisors wealth advisor today.

-

Integrated insurance planning is the practice of coordinating your insurance coverage — life, disability, liability, and long-term care — with your broader financial plan, including your investments, tax strategy, and estate plan, so that all elements can work together designed to protect your wealth.

-

A comprehensive wealth plan typically considers life insurance for legacy and estate planning purposes, disability insurance to protect income, personal umbrella insurance to extend liability coverage beyond standard policy limits, and long-term care insurance to help cover potential caregiving costs later in life.

-

A nuclear verdict is a jury award of $10 million or more. These awards have increased significantly in recent years, making it more important than ever to ensure your liability coverage — including umbrella insurance — is calibrated to your current asset base and risk exposure.3

-

An insurance review conducted by a team that understands your full financial picture is an effective way to identify gaps. At Mercer Advisors, our Insurance Solutions Team reviews your existing policies alongside your wealth, estate, and tax plan to help determine whether your coverage is comprehensive and properly coordinated.

-

We recommend an annual review as well as a review following any major life change — such as a change in net worth, the acquisition of a new property, a family milestone, a business event, or a change in beneficiary status.

-

Mercer Advisors has an internal Insurance Solutions Team that works alongside your wealth advisor to conduct reviews and identify coverage options. We work with a number of highly-rated insurance carriers to present options suited to your individual situation.

-

Mercer Advisors Insurance Services, LLC (MAIS) is a wholly owned subsidiary of Mercer Advisors Inc. MAIS provides individual life, disability, long term care coverage, and property and casualty coverage through various insurance companies. For Mercer Global Advisors clients who wish to purchase insurance products, MAIS has entered into a non-exclusive referral agreement with Strategic Partner(s), where the Strategic Partner will provide necessary services relative to the marketing, placement, and servicing of the insurance products, including without limitation preparing and presenting illustrations, supporting the underwriting process, assisting with the completion and execution of applications, delivering policies, and servicing in-force business. MAIS and the Strategic Partner will be listed as either “agents” or “co-agents” on the policies. While Mercer Global Advisors does not receive a referral fee, Strategic Partner receives a percentage of the commission revenue. MAIS and Strategic Partner do have a revenue sharing agreement.

-

A stand-alone insurance agent typically evaluates coverage needs in isolation — without visibility into your investment portfolio, tax situation, or estate plan. An integrated team can identify how your insurance interacts with each of those areas, helping to ensure your coverage is not just adequate on its own but optimally positioned in your full financial strategy.

-

There is no universal answer. A hybrid policy eliminates the “use it or lose it” issue common with traditional long-term care policies, and it offers more premium payment flexibility and the potential to build cash value. However, it may reduce the death benefit available to beneficiaries, and coverage limits may differ from stand-alone long-term care policies. The right choice depends on your age, health, financial goals, and overall wealth plan.

1,3 “Tort Reform Gains Ground as Nuclear Verdicts Reshape Liability Landscape.” Risk & Insurance, July 31, 2025.

2 “Understanding Long-Term Care Costs in 2026.” The Care Compass, June 22, 2026.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy.

Mercer Advisors is not a law firm and does not provide legal advice to clients. All Estate planning document preparation and other legal advice are provided through select third parties, with which Mercer Advisors has a contractual relationship. Mercer Advisors Tax Services, LLC, does not provide financial audit, assurance, compilations, or forensic accounting services. Insurance products are provided by Mercer Advisors Insurance Services, LLC (MAIS), which places individual life, disability, long term care coverage, and property and casualty coverage through select insurance companies.