It has been just over a month since the war in Iran began. Even for those closely following events, it has been difficult to judge whether the conflict is de‑escalating or intensifying. While the path ahead remains uncertain, the available data thus far allows conclusions to be reached about the impact on oil markets, the economy, and financial markets.

The impact on global oil markets

The conflict has dramatically reduced the amount of oil being shipped through the Strait of Hormuz, the source of about one-fifth of the world’s seaborne oil, causing a dramatic spike in oil and gas prices.

- Oil transit through the Strait of Hormuz is at a standstill, representing the largest disruption in global oil markets in history, according to the International Energy Agency.

- Oil prices have risen 40% since the outbreak of the conflict, with Brent Crude at $101 per barrel as of this writing.

- The U.S. national average gas price surpassed $4 per gallon this week– the highest since the early months of Russia’s invasion of Ukraine.

- The inflationary impact is immediate. The Cleveland Fed’s real-time inflation forecast, for example, now expects 3.9% headline PCE inflation in the first quarter of 2026, up from an expectation of 2.7% before the war began.

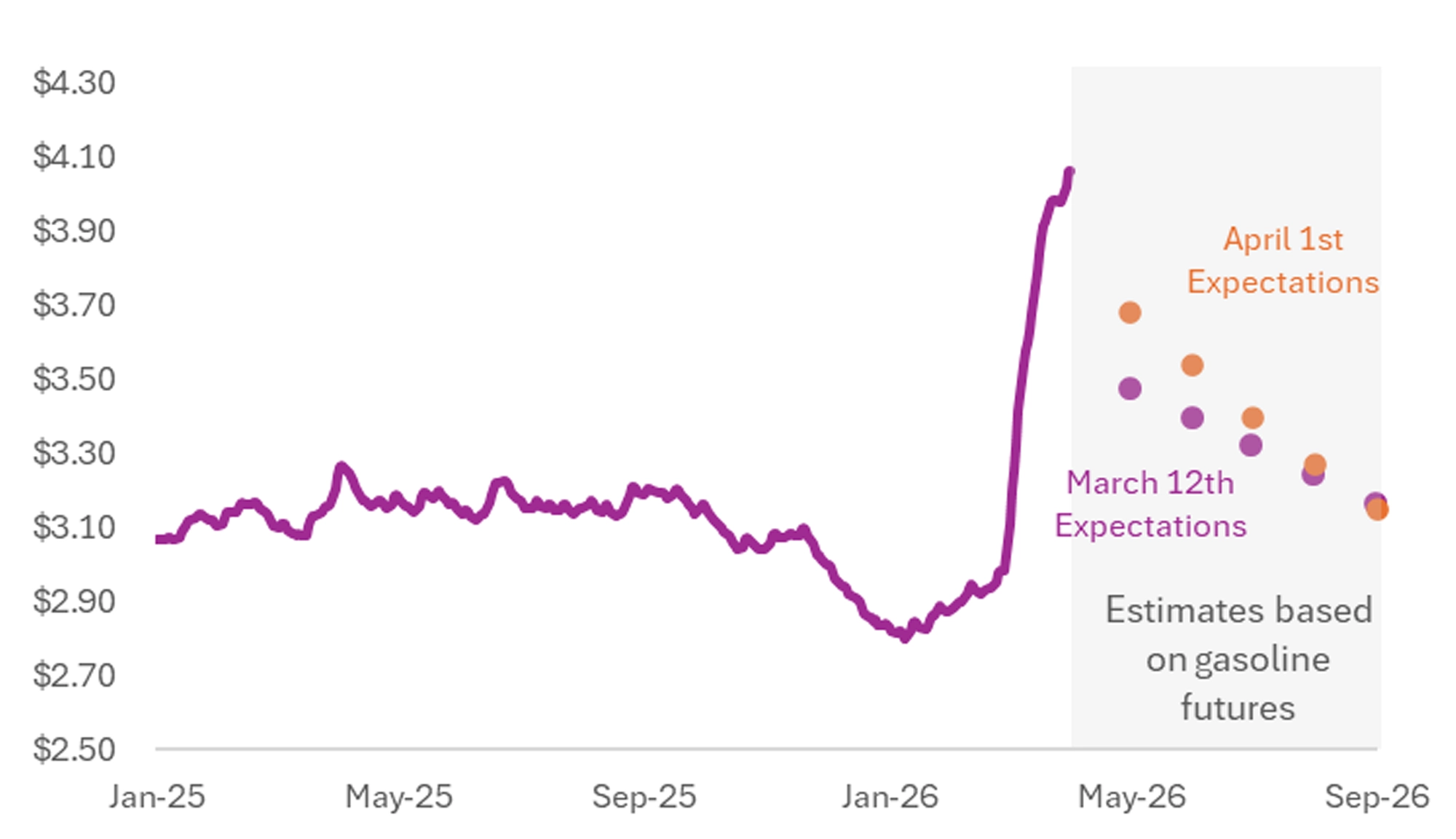

Looking ahead, what matters most about growth and inflation is not just how high oil prices rise, but how long they remain elevated and whether additional headwinds emerge. As the chart below shows, markets expect gasoline prices to ease over time. That is encouraging, though expectations remain higher than they were just two weeks ago, and prices over the next five months are still expected to exceed 2025 levels.

Figure 1: Expected U.S. Retail Gasoline Prices

Note: Expected gasoline prices based on current futures plus 55 cents for taxes. Source: American Automobile Association, Bloomberg Finance, LP, Mercer Advisors calculations, as of April 1, 2026.

Monitoring economic impacts

Most economic indicators are backward-looking and released with a lag. Consequently, it’s still too early to know with any certainty about the war’s ultimate economic impacts. In the meantime, here are several things our team continues to monitor:

- Inflation expectations: Near-term inflation expectations have surged, corresponding with higher oil and commodity prices. So far, markets anticipate the conflict will be short-lived. Longer-term inflation expectations remain anchored.

- Supply chain disruptions: The Strait of Hormuz is a primary trade channel not just for oil but for commodities such as fertilizer (30% of world supply), helium, and sulfur. Such disruptions increase the cost of production and should eventually result in higher prices for food and other consumer products.

- Growth: While higher inflation is a headwind to growth, the biggest risk is not the initial spike in energy prices, but whether prices remain elevated long enough to stall the economy. If oil prices ease over the coming months — as futures markets currently expect — the drag on growth should fade. The data suggests U.S. GDP growth would likely slow temporarily but remain positive, driven by AI and government spending tailwinds. Current data suggests a recession to be unlikely. One difference between past energy crises, the U.S. is now a net oil exporter. Higher oil prices can induce greater investment by domestic producers, which could partially offset the negative impacts of reduced consumption in measures of aggregate economic growth.

- Interest rates have jumped on inflation fears, which in turn weigh on interest-sensitive sectors like housing. The average rate for a 30-year fixed rate mortgage according to Freddie Mac was 6.38% as of March 31, up from 5.98% before the war began. Higher mortgage interest rates have reduced demand for new mortgage applications (a gauge of housing demand) according to the Mortgage Bankers Association’s weekly index.

The market reaction

Bond markets have come under pressure amid inflation and growth concerns. The 2‑year Treasury yield has risen about 40 basis points, while the 30‑year is up roughly 30 basis points. (Higher yields mean lower bond prices.)

The Fed: Before the conflict, markets expected the Federal Reserve to cut interest rates twice this year. Now, markets expect no rate cuts for the remainder of the year.

Equity markets are down around the world. Consider the following:

- Since before the beginning of the war, on February 27, the S&P 500 has returned -5.0%; international stocks, as measured by the MSCI All-Country World Ex-US Index, have returned -10.7%.

- That said, international stocks had delivered strong year-to-date returns prior to the war, up 11.33% through February 27. On a year-to-date basis, international stocks are down -0.60% versus -4.4% for the S&P 500.

- Perhaps surprisingly, U.S. defense and aerospace companies, as measured by the iShares U.S. Aerospace & Defense ETF (ITA), have so far underperformed the broad market, returning -10.3% since the outbreak of the conflict. This is a reminder that many factors influence market prices, not just headlines, and that “obvious” investment theses do not exist.

Key takeaways

The situation in Iran remains fluid, and a healthy dose of humility is required when forecasting oil markets, the economy, or financial markets. After one month, nevertheless, several conclusions stand out:

- Energy and other input costs have risen sharply, but markets still expect these increases to be temporary. If the market’s expectations prove accurate, gasoline prices and other upward price pressures should ease as the year progresses.

- Higher oil and commodity prices will result in higher inflation in the short run, but growth indicators remain resilient. The data currently suggests a coming recession would be unlikely. This can naturally change as more post-February 27 economic data comes in.

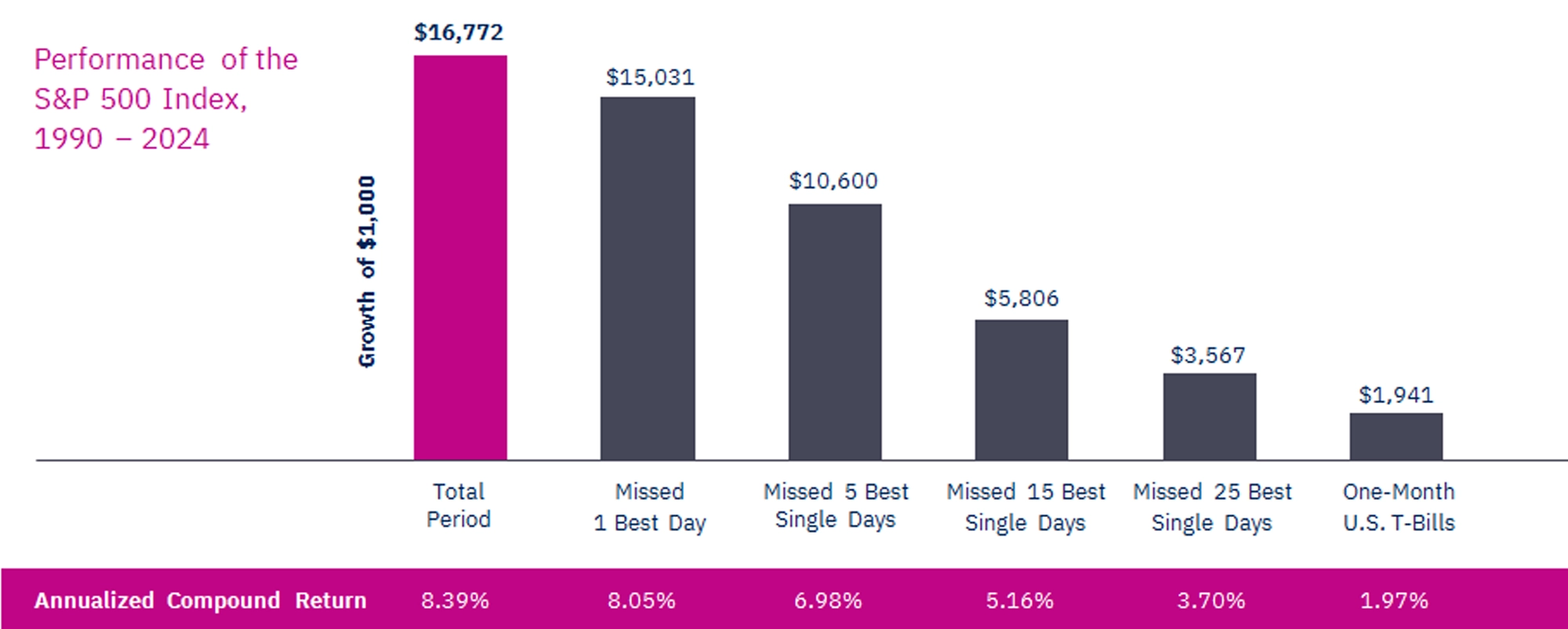

- Financial markets have declined, yet history suggests recoveries often arrive sooner than expected. During periods of turmoil, investors may feel tempted to move to cash and wait for calm, but Figure 2 below illustrates why this approach can be harmful (see also: The Fallacy of Selling and Waiting Until Markets Calm Down: Insights From Our CIO). Missing even a handful of the market’s best days—often during rebounds—can significantly reduce long‑term returns. For this reason, we believe the best strategy is to stay invested and broadly diversified. No one can reliably predict when markets will turn higher.

Figure 2: Effect of missing the market’s best days

Click here for more insights from our CIO and investment team. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Home » Insights » Market Commentary » The Economic and Market Impact of the Iran War After One Month: Insights From Our CIO

The Economic and Market Impact of the Iran War After One Month: Insights From Our CIO

Donald Calcagni, MBA, MST, CFP®, AIF®

Chief Investment Officer

The conflict is ongoing and rapidly evolving, but early evidence shows the extent of the economic impact

It has been just over a month since the war in Iran began. Even for those closely following events, it has been difficult to judge whether the conflict is de‑escalating or intensifying. While the path ahead remains uncertain, the available data thus far allows conclusions to be reached about the impact on oil markets, the economy, and financial markets.

The impact on global oil markets

The conflict has dramatically reduced the amount of oil being shipped through the Strait of Hormuz, the source of about one-fifth of the world’s seaborne oil, causing a dramatic spike in oil and gas prices.

Looking ahead, what matters most about growth and inflation is not just how high oil prices rise, but how long they remain elevated and whether additional headwinds emerge. As the chart below shows, markets expect gasoline prices to ease over time. That is encouraging, though expectations remain higher than they were just two weeks ago, and prices over the next five months are still expected to exceed 2025 levels.

Figure 1: Expected U.S. Retail Gasoline Prices

Note: Expected gasoline prices based on current futures plus 55 cents for taxes. Source: American Automobile Association, Bloomberg Finance, LP, Mercer Advisors calculations, as of April 1, 2026.

Monitoring economic impacts

Most economic indicators are backward-looking and released with a lag. Consequently, it’s still too early to know with any certainty about the war’s ultimate economic impacts. In the meantime, here are several things our team continues to monitor:

The market reaction

Bond markets have come under pressure amid inflation and growth concerns. The 2‑year Treasury yield has risen about 40 basis points, while the 30‑year is up roughly 30 basis points. (Higher yields mean lower bond prices.)

The Fed: Before the conflict, markets expected the Federal Reserve to cut interest rates twice this year. Now, markets expect no rate cuts for the remainder of the year.

Equity markets are down around the world. Consider the following:

Key takeaways

The situation in Iran remains fluid, and a healthy dose of humility is required when forecasting oil markets, the economy, or financial markets. After one month, nevertheless, several conclusions stand out:

Figure 2: Effect of missing the market’s best days

Click here for more insights from our CIO and investment team. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Explore More

Using Retirement Trusts to Protect and Transfer IRAs

Personal Umbrella Insurance: FAQs to Help Protect Your Wealth

S Corporation Losses, Trusts, and Termination