There continues to be elevated media interest (much of it quite negative in tone) in private credit, driven largely by a handful of high-profile but isolated incidents that have spooked some investors.

The private credit landscape

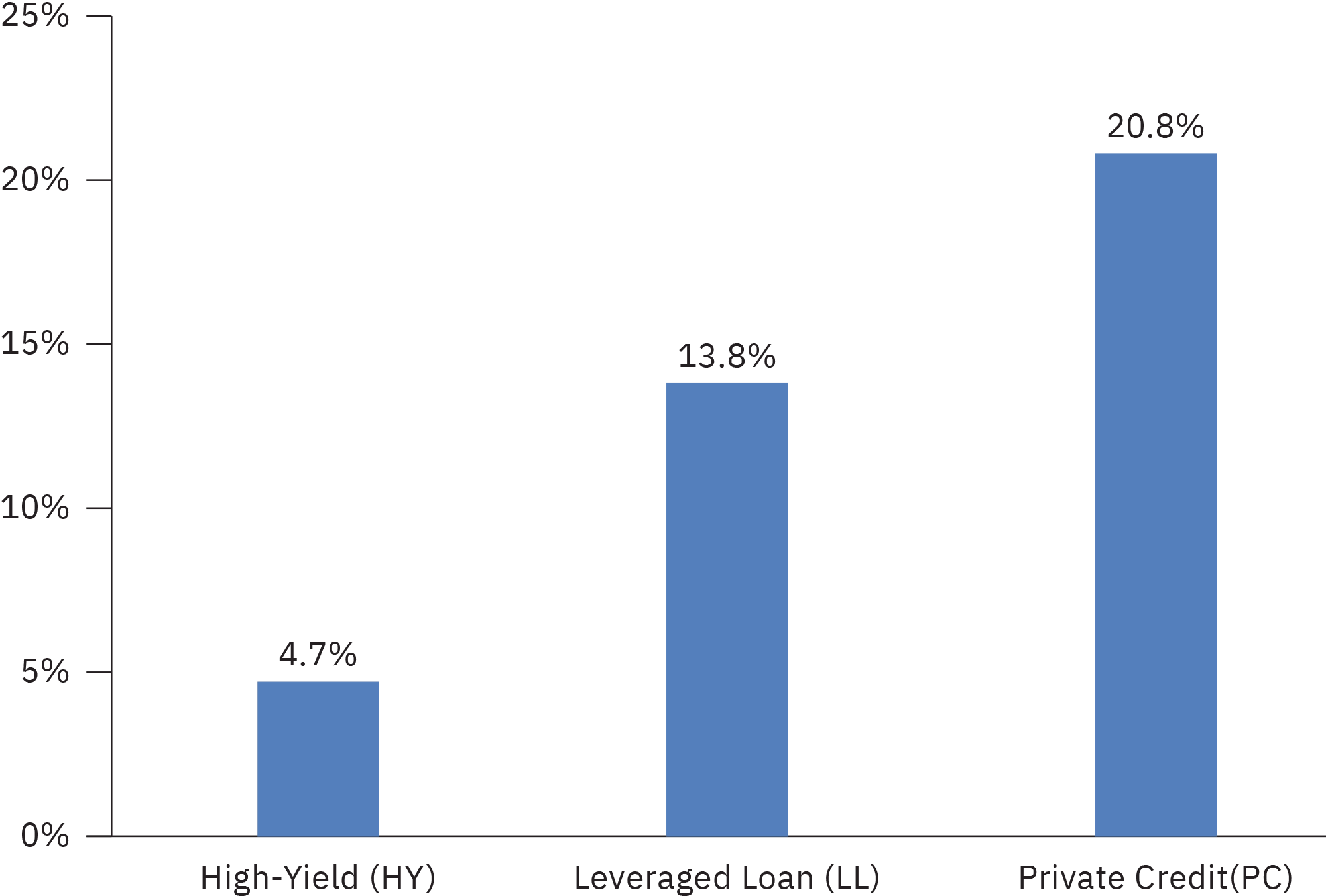

Private credit describes a wide range of privately originated loans (outside the banking system or bond market) to non-public or middle-market companies. The loans are typically floating-rate, high-yield, and negotiated directly with borrowers.

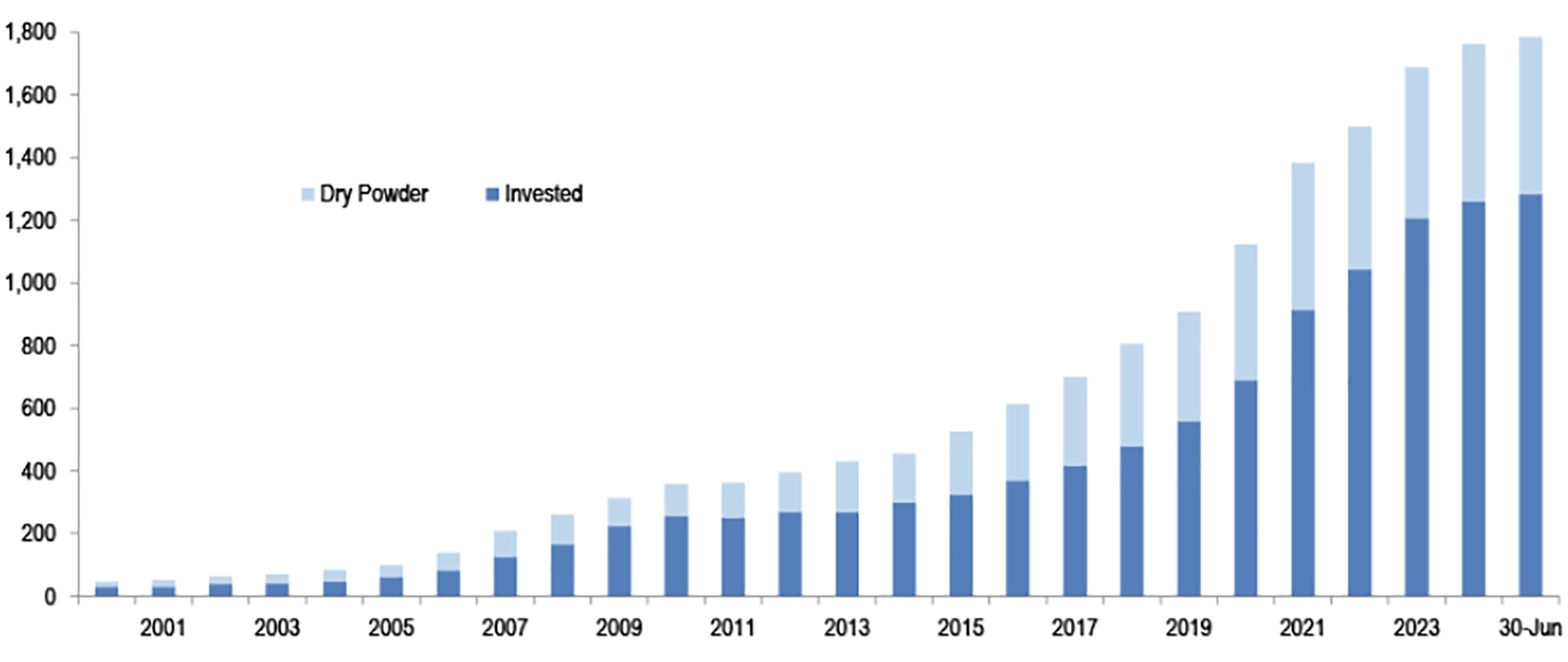

The media has long been interested in the asset class because it has grown very rapidly since the Global Financial Crisis. Much coverage of the asset conveys a vague sense that somehow this growth will end badly. However, similar fears are sometimes raised for virtually any of today’s elevated asset classes —whether that is private credit, U.S. equities, real estate, and so on.

Why has private credit grown so much?

Private credit has grown since the financial crisis of 2007-09 because it filled a gap left by banks as they stepped back from middle-market lending.

For investors, private credit has offered an attractive yield premium relative to public fixed income investments. For borrowers, private credit loans have offered speed, availability, and bespoke financing solutions. There has been increasing institutional adoption and long-term capital support for the asset class.

These basic developments are not intrinsically concerning.

What’s driving current concerns?

Investor concerns have evolved over the past year, starting with liquidity issues, followed by company‑specific headlines, and most recently expanding to questions about the composition of loan portfolios.

- Liquidity concerns: A report from Moody’s last summer warned about what they described as intensifying liquidity risks in private credit. (We responded at the time: How We Manage Private Market Risks.) Moody’s highlighted that retail investors generally prefer high liquidity, especially during times of market stress but private investments, by design, are illiquid.

- Deal-specific news: Last fall, two firms backed by private credit loans collapsed: the sub-prime auto lender Tricolor (which faced fraud allegations) as well as car parts supplier First Brands. This got extra attention when JPMorgan CEO Jamie Dimon said on an earnings call, “My antenna goes up when things like that happen. I probably shouldn’t say this, but when you see one cockroach, there’s probably more.” Then last month, Blue Owl Capital, a private credit fund manager, changed its redemption strategy.

- Concerns around the quality of loan portfolios: While private credit spans many industries, a relatively large share of borrowers are software companies. Some market participants worry that software‑as‑a‑service businesses could face rapid disruption from artificial intelligence. If this disruption were to materialize quickly, it could impair the ability of certain borrowers to repay their loans.

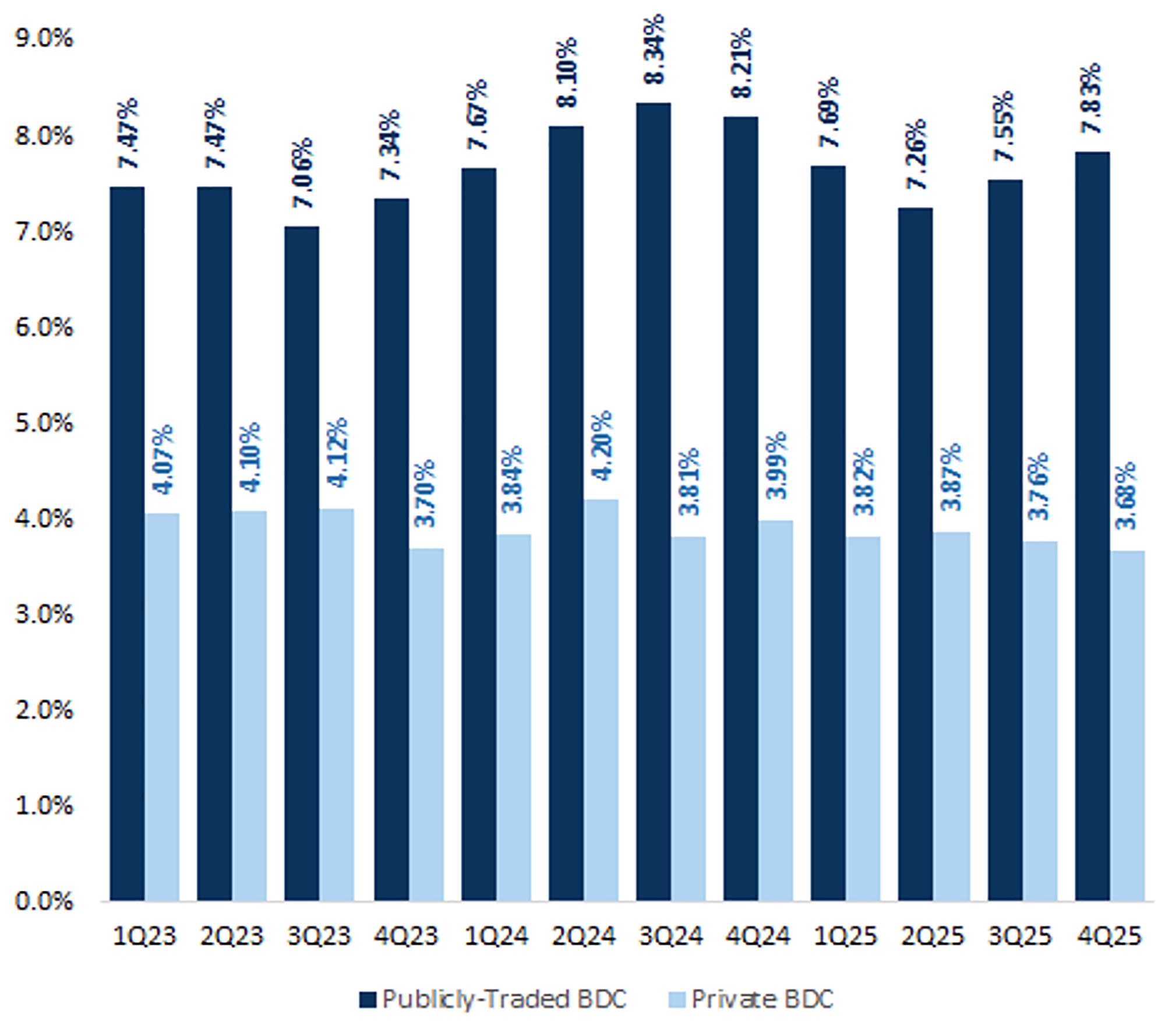

Another concern relates to the increased use of Payment‑in‑Kind (PIK) interest. With PIK, interest is added to the loan balance instead of being paid in cash. As a result, the total amount of outstanding debt grows over time. Rising reliance on PIK structures can be a signal that some borrowers are experiencing reduced capacity to service their loans through regular cash payments.

The difference between outflows and fund performance

Some investors have sought to exit private credit investments, as Moody’s warned. But we should distinguish between (1) a sentiment-driven desire to exit private credit funds, and (2) whether the underlying loans within those funds are performing poorly.

At this stage, there isn’t strong evidence to suggest the underlying loans in private credit portfolios are distressed. A prime example: When Blue Owl was in the news last month, it sold $1.4 billion of its loan portfolio at 99.7% of par value to four institutional investors in an arms-length transaction. Sophisticated, institutional investors paying 99.7% of par value for a large loan portfolio is not what we would expect in a distressed sale of loans of deteriorating in quality.

What is Mercer Advisors take on private credit?

Our current view is that while there are concerns about the high concentration of software companies in private credit as an asset class, overall, the underlying portfolios of loans appear to be fine.

The biggest issue is a classic investor-investment mismatch in this space. Some private credit investment funds have aggressively courted retail investors who, in many cases, did not understand the limited liquidity of their investments. Private credit is not designed to be like a bond ETF that you can easily sell whenever you’d like.

We believe that private credit is only suitable for investors who can forgo liquidity on that portion of their portfolio for at least 7-10 years in exchange for higher yields. Suitable investors should have sufficient liquidity elsewhere in their balance sheet, so they don’t need to tap long-term assets for unexpected needs. Additionally, private credit is a risky asset, therefore investors should be willing to withstand drawdowns and periods of negative performance.

As with all private investments, it is paramount that investors understand they are giving up liquidity in exchange for higher expected returns.

Main takeaways for investors

Private credit continues to occupy an important place within the broader investment landscape. For investors who understand the long‑term commitment required, private credit can still serve as a valuable source of yield and diversification. Our approach to private credit is centered around three core tenants that help manage the inherent risks of this asset class.

- Manager selection generally drives outcomes: Private credit is an asset class where historically the best managers have significantly outperformed the worst managers. We should not be surprised that some managers have had poor performance or seen individual investments get in trouble. This doesn’t mean investors should avoid the asset class entirely, but it does mean they need to focus on cycle‑tested underwriting, disciplined credit selection, covenant strength, and risk controls. At Mercer Advisors, we carefully vet fund managers before and after making allocations.

- Diversification helps reduce idiosyncratic risks: Spreading exposure across managers, sectors, borrowers, structures, and vintages helps avoid concentration in individual companies or areas experiencing stress (such as software, or PIK-heavy financing).

- Allocation sizing and illiquidity planning are essential: Private credit is inherently illiquid, regardless of vehicle structure, and should be sized as a long‑term allocation. Much of the current consternation could have been avoided if the investors in question better understood the liquidity characteristics of their investments. Upfront conversations about liquidity, time horizon, and portfolio balance are critical to successful implementation.

Click here for more insights from our CIO and investment team. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Alternative or Private investments are subject to limited liquidity and greater risks than those associated with traditional investments and are not suitable for all investors. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Home » Insights » Market Commentary » Is There a Crisis Brewing in Private Credit?

Is There a Crisis Brewing in Private Credit?

David Krakauer, CFA®, CRPS®

Vice President, Portfolio Management

VP of Portfolio Management David Krakauer analyzes why the current concerns about private credit may be overblown.

There continues to be elevated media interest (much of it quite negative in tone) in private credit, driven largely by a handful of high-profile but isolated incidents that have spooked some investors.

The private credit landscape

Private credit describes a wide range of privately originated loans (outside the banking system or bond market) to non-public or middle-market companies. The loans are typically floating-rate, high-yield, and negotiated directly with borrowers.

The media has long been interested in the asset class because it has grown very rapidly since the Global Financial Crisis. Much coverage of the asset conveys a vague sense that somehow this growth will end badly. However, similar fears are sometimes raised for virtually any of today’s elevated asset classes —whether that is private credit, U.S. equities, real estate, and so on.

Why has private credit grown so much?

Private credit has grown since the financial crisis of 2007-09 because it filled a gap left by banks as they stepped back from middle-market lending.

For investors, private credit has offered an attractive yield premium relative to public fixed income investments. For borrowers, private credit loans have offered speed, availability, and bespoke financing solutions. There has been increasing institutional adoption and long-term capital support for the asset class.

These basic developments are not intrinsically concerning.

What’s driving current concerns?

Investor concerns have evolved over the past year, starting with liquidity issues, followed by company‑specific headlines, and most recently expanding to questions about the composition of loan portfolios.

Another concern relates to the increased use of Payment‑in‑Kind (PIK) interest. With PIK, interest is added to the loan balance instead of being paid in cash. As a result, the total amount of outstanding debt grows over time. Rising reliance on PIK structures can be a signal that some borrowers are experiencing reduced capacity to service their loans through regular cash payments.

The difference between outflows and fund performance

Some investors have sought to exit private credit investments, as Moody’s warned. But we should distinguish between (1) a sentiment-driven desire to exit private credit funds, and (2) whether the underlying loans within those funds are performing poorly.

At this stage, there isn’t strong evidence to suggest the underlying loans in private credit portfolios are distressed. A prime example: When Blue Owl was in the news last month, it sold $1.4 billion of its loan portfolio at 99.7% of par value to four institutional investors in an arms-length transaction. Sophisticated, institutional investors paying 99.7% of par value for a large loan portfolio is not what we would expect in a distressed sale of loans of deteriorating in quality.

What is Mercer Advisors take on private credit?

Our current view is that while there are concerns about the high concentration of software companies in private credit as an asset class, overall, the underlying portfolios of loans appear to be fine.

The biggest issue is a classic investor-investment mismatch in this space. Some private credit investment funds have aggressively courted retail investors who, in many cases, did not understand the limited liquidity of their investments. Private credit is not designed to be like a bond ETF that you can easily sell whenever you’d like.

We believe that private credit is only suitable for investors who can forgo liquidity on that portion of their portfolio for at least 7-10 years in exchange for higher yields. Suitable investors should have sufficient liquidity elsewhere in their balance sheet, so they don’t need to tap long-term assets for unexpected needs. Additionally, private credit is a risky asset, therefore investors should be willing to withstand drawdowns and periods of negative performance.

As with all private investments, it is paramount that investors understand they are giving up liquidity in exchange for higher expected returns.

Main takeaways for investors

Private credit continues to occupy an important place within the broader investment landscape. For investors who understand the long‑term commitment required, private credit can still serve as a valuable source of yield and diversification. Our approach to private credit is centered around three core tenants that help manage the inherent risks of this asset class.

Click here for more insights from our CIO and investment team. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Alternative or Private investments are subject to limited liquidity and greater risks than those associated with traditional investments and are not suitable for all investors. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Explore More

Washington’s Income Tax Debate: Capital Gains, the Millionaires’ Tax, and What Comes Next

Estate Planning for Women Who Expect to Live — and Lead — Longer

The Stock Market Was Strong Entering the Turmoil of the Iran War