Investors who have avoided the temptation to chase speculative assets were spared sharp losses in recent weeks in the gold, silver, and cryptocurrency markets. At Mercer Advisors, we have long argued that these assets are speculative and not something that should be part of a fiduciary-centered portfolio.

How significant was the sell-off?

In the immediate aftermath of the announcement that President Trump intended to nominate Kevin Warsh as the next chair of the Federal Reserve, gold and silver had their worst day since 1980 (see Figure 1). Bitcoin has also declined significantly since Warsh’s announcement.

Figure 1. Price changes in gold, silver, and Bitcoin versus global stocks and global bonds

Past performance is no guarantee of future returns. You cannot invest in an index. Global Stocks: MSCI All-Country World IMI Index. Global Bonds: Bloomberg Global Aggregate Bond Index USD Hedged. Source: MSCI, Bloomberg Finance, LP, Standard & Poors, CoinGecko, YCharts, Mercer Advisors, as of 2/11/26.

What caused gold, silver, and crypto to plunge?

The decisions of the Federal Reserve, and changes in its leadership, are always closely watched by financial markets.

The Warsh announcement precipitated a sharp decline in speculative asset prices, as many investors assessed that he would be more vigilant against inflation and a decline in the U.S. dollar than some other contenders to lead the central bank. Warsh had been at the Fed from 2006 to 2011 and, in the years immediately following his departure, staked out a hawkish anti-inflation viewpoint. He has since moderated that stance, expressing views more closely aligned with the president, who has called for lower interest rates. While it remains to be seen exactly what Warsh might do at the central bank, the market’s verdict was swift.

How does Mercer Advisors view gold, silver, and crypto?

At Mercer Advisors, we have never recommended speculative assets because we believe it conflicts with our fiduciary duty to our clients and our approach to stewardship of their assets. A previous post made the case for why Bitcoin should not be considered an investable asset, even when it was on an upswing.

Just a few days before the Warsh announcement, we responded to the question: “Are gold and silver a good hedge right now?” by explaining that we don’t view gold and silver as investable assets, but rather as speculative assets which tend to be more volatile. Volatility, of course, means assets swing both up and down. Recently, that volatility has been to the upside. But that volatility can just as easily (and unpredictably) shift to the downside when sentiment changes — resulting in meaningful drags on performance.

What is meant by an investable asset?

To be an investable asset, it must meet three criteria:

- The asset should generate current (or future expected) cash flows.

- Investors’ ownership rights of the asset should be well defined and enforceable in U.S. courts of law.

- Investors should be able to buy and sell freely and securely through a regulated market (whether public or private).

Investable assets, therefore, include stocks, bonds, private equity, real estate, and more. These assets generate a stream of profits, dividends, or interest payments that provide a basis for asset valuations.

What is meant by a speculative asset?

Investments that don’t pass these tests are speculative in nature. Gold, silver, and Bitcoin do not generate cash flows. Further, cryptocurrencies including Bitcoin lack clear ownership rights and well-established regulation. Collectibles or exotic cars would be other examples of assets we’d classify as speculative.

Speculative assets tend to trade on short-term investor sentiment since they lack underlying cash flows. This month has been a case in point. The president nominated someone who had openly been on his short list to lead the Federal Reserve – news that’s not shocking by itself – but that lead to a dramatic shift in short-term investor sentiment.

While one may be able to sometimes sell these assets at a profit, if lucky on timing, we view this as essentially a speculative gamble, rather than a strategy that fiduciaries can stand behind.

Do speculative assets have a role to play in portfolios?

For most long-term investors, allocating capital to these types of assets is not a prudent portfolio strategy.

- Over the long term, speculative assets have not had returns to justify the amount of risk involved, both in terms of volatility and (in some cases) even the investment’s risk of total loss.

- Speculative assets have not provided reliable diversification benefits. For those interested in a deeper dive, we’ve included an appendix at the end of this piece demonstrating how gold has been neither a reliable diversifier nor a reliable hedge against certain adverse outcomes.

Our takeaways

- Our fiduciary duty is upheld by avoiding non‑investable assets. Acting in a fiduciary capacity requires disciplined decision‑making based on our clients’ best interests, not speculation. Some investors may get lucky gambling on commodities or other speculative assets (some people get lucky in a casino), but luck is not a strategy. Our role is to provide thoughtful, evidence‑based investment guidance designed to grow and protect wealth.

- Diversify with an evidence-based approach. While broad diversification across and within asset classes is important, it must be intentional. The diversification benefits of speculative assets have historically been inconsistent and unpredictable, meaning they appear randomly rather than systematically. Effective diversification is built from purposeful portfolio construction, not scattershot inclusion of high‑volatility, low‑reliability assets.

- Discuss your underlying concerns and goals. If you’re feeling tempted by speculative assets like gold, silver, or crypto, talk to your advisor. This is an opportunity to understand your goals, clarify your worries, and likely identify more reliable solutions that align with your long‑term objectives. There are almost always better, more prudent ways to meet investment needs than taking on unnecessary speculation.

Click here for past insights about wealth management and other interesting topics. Not a Mercer Advisors client but interested in more information? Let’s talk.

Appendix

For those interested in a deeper dive, the following statistics underpin our views:

A metric for diversification

Diversification can be evaluated using correlation, a statistical measure of how closely two sets of data move together.

- Correlation exists on a scale of 1 to -1.

- 1 means the two data series move together in lockstep.

- 0 means that there is no relationship.

- -1 means they move opposite to each other.

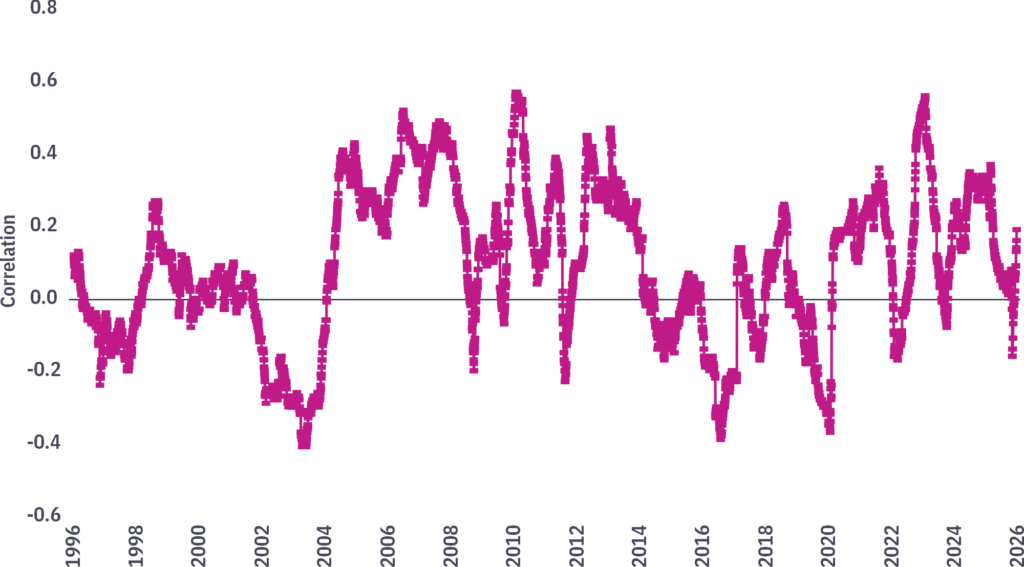

Consider the correlation between gold and global stocks in Appendix Figure 1:

Appendix Figure 1: Six-month rolling correlation between the price of gold vs. global stocks

Global Stocks: MSCI All-Country World IMI Index. Source: MSCI, Bloomberg Finance, LP, Mercer Advisors, as of 2/6/26.

Note: gold is shown as an example because it illustrates a longer history of performance than that of crypto.

What is the takeaway from this chart? The relationship has varied over time in an unpredictable way. Gold has had no stable relationship with equities. This is an example of how the volatility of their performance makes speculative assets, at best, random diversifiers.

What drives gold prices?

Proponents of gold make many (and shifting) claims about the asset. Gold has sometimes been claimed to correlate with trends in real interest rates, = to hedge against inflation, or to protect against growing U.S. deficits. The table below compares the monthly correlation of gold prices with all three of those economic trends over three-plus decades:

Correlation in monthly change (Jan. 1994 – Dec. 2025)

| |

Real Fed Funds |

Consumer Price Index |

Deficit as a % of GDP |

| Gold |

-0.04 |

0.03 |

-0.04 |

Source: Bureau of Labor Statistics, Federal Reserve, U.S. Treasury Department, Bloomberg Finance LP, Mercer Advisors, as of 12/31/2025

The table shows that, for all three measures, the correlations are remarkably close to zero. In other words, there is virtually no relationship between gold and the three commonly proposed “drivers” of gold prices in recent history.

Click here for past insights about wealth management and other interesting topics. Not a Mercer Advisors client but interested in more information? Let’s talk.

Home » Insights » Market Commentary » Why We Don’t Speculate on Gold, Silver, and Crypto: Insights From Our CIO

Why We Don’t Speculate on Gold, Silver, and Crypto: Insights From Our CIO

Donald Calcagni, MBA, MST, CFP®, AIF®

Chief Investment Officer

Mercer Advisors CIO Don Calcagni explains why gold, silver, and crypto should be considered “speculative assets” that do not belong in most portfolios.

Investors who have avoided the temptation to chase speculative assets were spared sharp losses in recent weeks in the gold, silver, and cryptocurrency markets. At Mercer Advisors, we have long argued that these assets are speculative and not something that should be part of a fiduciary-centered portfolio.

How significant was the sell-off?

In the immediate aftermath of the announcement that President Trump intended to nominate Kevin Warsh as the next chair of the Federal Reserve, gold and silver had their worst day since 1980 (see Figure 1). Bitcoin has also declined significantly since Warsh’s announcement.

Figure 1. Price changes in gold, silver, and Bitcoin versus global stocks and global bonds

Past performance is no guarantee of future returns. You cannot invest in an index. Global Stocks: MSCI All-Country World IMI Index. Global Bonds: Bloomberg Global Aggregate Bond Index USD Hedged. Source: MSCI, Bloomberg Finance, LP, Standard & Poors, CoinGecko, YCharts, Mercer Advisors, as of 2/11/26.

What caused gold, silver, and crypto to plunge?

The decisions of the Federal Reserve, and changes in its leadership, are always closely watched by financial markets.

The Warsh announcement precipitated a sharp decline in speculative asset prices, as many investors assessed that he would be more vigilant against inflation and a decline in the U.S. dollar than some other contenders to lead the central bank. Warsh had been at the Fed from 2006 to 2011 and, in the years immediately following his departure, staked out a hawkish anti-inflation viewpoint. He has since moderated that stance, expressing views more closely aligned with the president, who has called for lower interest rates. While it remains to be seen exactly what Warsh might do at the central bank, the market’s verdict was swift.

How does Mercer Advisors view gold, silver, and crypto?

At Mercer Advisors, we have never recommended speculative assets because we believe it conflicts with our fiduciary duty to our clients and our approach to stewardship of their assets. A previous post made the case for why Bitcoin should not be considered an investable asset, even when it was on an upswing.

Just a few days before the Warsh announcement, we responded to the question: “Are gold and silver a good hedge right now?” by explaining that we don’t view gold and silver as investable assets, but rather as speculative assets which tend to be more volatile. Volatility, of course, means assets swing both up and down. Recently, that volatility has been to the upside. But that volatility can just as easily (and unpredictably) shift to the downside when sentiment changes — resulting in meaningful drags on performance.

What is meant by an investable asset?

To be an investable asset, it must meet three criteria:

Investable assets, therefore, include stocks, bonds, private equity, real estate, and more. These assets generate a stream of profits, dividends, or interest payments that provide a basis for asset valuations.

What is meant by a speculative asset?

Investments that don’t pass these tests are speculative in nature. Gold, silver, and Bitcoin do not generate cash flows. Further, cryptocurrencies including Bitcoin lack clear ownership rights and well-established regulation. Collectibles or exotic cars would be other examples of assets we’d classify as speculative.

Speculative assets tend to trade on short-term investor sentiment since they lack underlying cash flows. This month has been a case in point. The president nominated someone who had openly been on his short list to lead the Federal Reserve – news that’s not shocking by itself – but that lead to a dramatic shift in short-term investor sentiment.

While one may be able to sometimes sell these assets at a profit, if lucky on timing, we view this as essentially a speculative gamble, rather than a strategy that fiduciaries can stand behind.

Do speculative assets have a role to play in portfolios?

For most long-term investors, allocating capital to these types of assets is not a prudent portfolio strategy.

Our takeaways

Click here for past insights about wealth management and other interesting topics. Not a Mercer Advisors client but interested in more information? Let’s talk.

Appendix

For those interested in a deeper dive, the following statistics underpin our views:

A metric for diversification

Diversification can be evaluated using correlation, a statistical measure of how closely two sets of data move together.

Consider the correlation between gold and global stocks in Appendix Figure 1:

Appendix Figure 1: Six-month rolling correlation between the price of gold vs. global stocks

Global Stocks: MSCI All-Country World IMI Index. Source: MSCI, Bloomberg Finance, LP, Mercer Advisors, as of 2/6/26.

Note: gold is shown as an example because it illustrates a longer history of performance than that of crypto.

What is the takeaway from this chart? The relationship has varied over time in an unpredictable way. Gold has had no stable relationship with equities. This is an example of how the volatility of their performance makes speculative assets, at best, random diversifiers.

What drives gold prices?

Proponents of gold make many (and shifting) claims about the asset. Gold has sometimes been claimed to correlate with trends in real interest rates, = to hedge against inflation, or to protect against growing U.S. deficits. The table below compares the monthly correlation of gold prices with all three of those economic trends over three-plus decades:

Correlation in monthly change (Jan. 1994 – Dec. 2025)

Source: Bureau of Labor Statistics, Federal Reserve, U.S. Treasury Department, Bloomberg Finance LP, Mercer Advisors, as of 12/31/2025

The table shows that, for all three measures, the correlations are remarkably close to zero. In other words, there is virtually no relationship between gold and the three commonly proposed “drivers” of gold prices in recent history.

Click here for past insights about wealth management and other interesting topics. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Explore More

The Economic and Market Impact of the Iran War After One Month: Insights From Our CIO

Using Retirement Trusts to Protect and Transfer IRAs

Personal Umbrella Insurance: FAQs to Help Protect Your Wealth