As the Iran war continues into its second week, oil and global equity markets continue to deteriorate. The longer the conflict persists, the higher energy prices are likely to rise with growing consequences for the global economy and financial markets. Within a 24-hour period on Sunday and Monday, oil prices shot as high as $118 a barrel and as low as $84 a barrel, underscoring the exceptional lack of clarity about the direction of the conflict.

We acknowledge the tremendous human costs and suffering caused by this war; our thoughts are with the families and communities affected, and with our servicemen and women in uniform. We are monitoring developments closely, and our key message remains straightforward: we are here, we are fully engaged, and we believe this is a time for steadiness rather than reaction.

Whiplash as the market assesses the possibility of a longer war

While the market’s initial reaction to the conflict was somewhat muted, several recent developments have raised the possibility of a more prolonged conflict. The first was President Trump’s demand on Friday for Iran’s unconditional surrender, followed by Iran’s announcement yesterday of Mojtaba Khamenei — who, as the son of Ayatollah Ali Khamenei, is thought to be ideologically aligned with the previous regime — as the country’s new supreme leader. Finally, Iran has not signaled a willingness to negotiate with Israel and the U.S.

This is likely to be a period where the tenor of commentary can shift rapidly, and the situation on the ground can change quickly. This is unlikely to be the last moment of market whiplash associated with the conflict, which is all the more reason to remain cautious in making any adjustments to our portfolio.

A few key takeaways

During challenging markets, it’s important to look through the barrage of negative news to identify meaningful lessons for investors. We think several are worth highlighting:

First, globally diversified portfolios were well-positioned coming into the conflict. Global stocks across the board finished February with handsome year-to-date gains. International developed and emerging markets stocks were up double digits.

Table 1: Year-to-date returns of major indexes before the conflict began and as of March 9

| |

As of Feb. 27 |

As of March 9 |

| S&P 500 |

0.7% |

-0.5% |

| Developed markets ex-U.S. |

10.1% |

1.1% |

| Emerging markets |

14.8% |

3.7% |

| U.S. aggregate bond market index |

1.8% |

1.1% |

| Global aggregate bond index (with currency hedge) |

1.7% |

0.7% |

Diversified investments in developed markets, emerging markets, and bonds were in a significantly stronger position than the S&P 500 alone before the start of the conflict. Despite dropping sharply in the early days of the conflict, international stocks and both U.S. and global bonds have outperformed U.S. equities year-to-date.

Markets are resilient in the long run

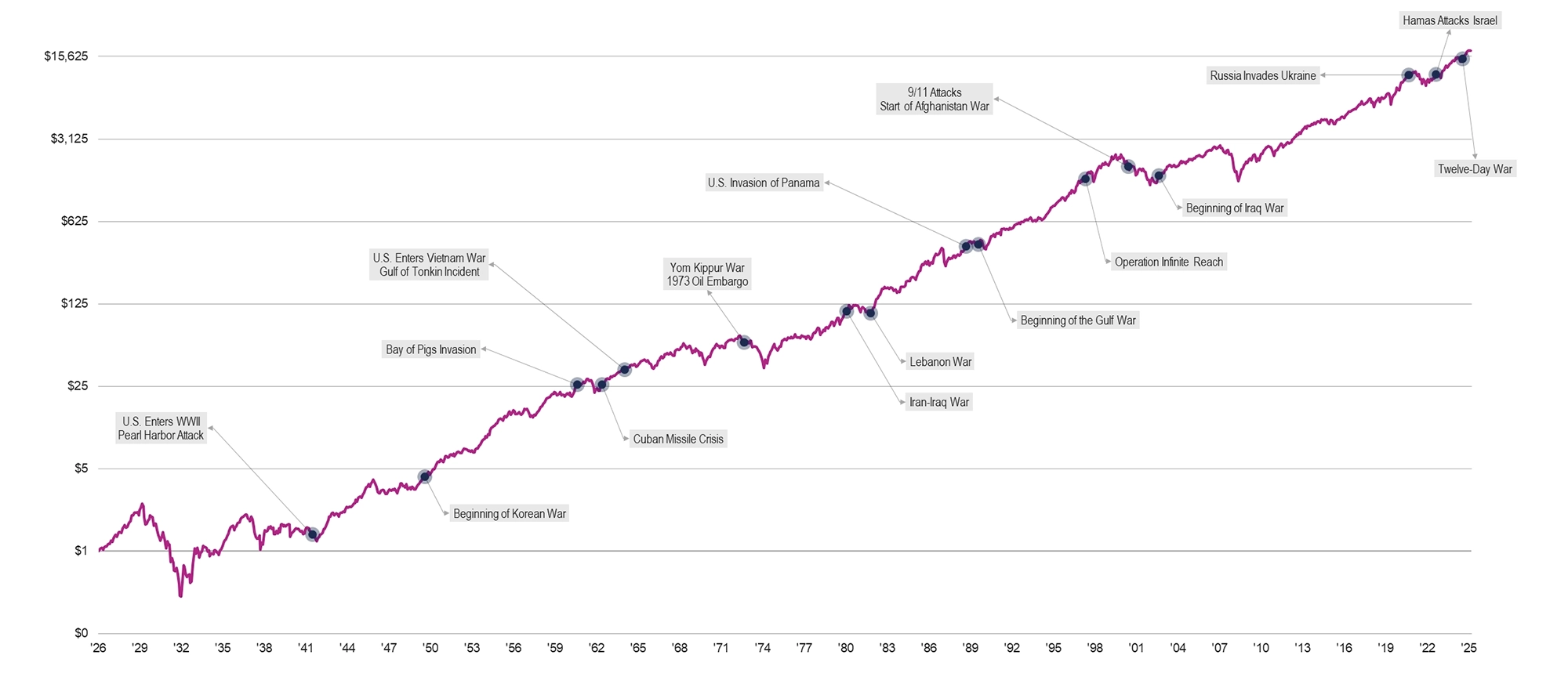

Our advice to remain calm and stay the course is informed by decades of real-world experience and nearly a century of empirical evidence (see below graphic from Avantis Investors). And what we’ve learned from such evidence is that all crises ultimately have a beginning, a middle, and an end. This one too shall end. While remaining calm and staying the course can be uncomfortable sometimes, market history teaches us that remaining well-diversified has historically been the best course of action during such crises.

Graphic 1: Markets have risen over time through major military conflicts.

The U.S. dollar remains one of the world’s most favored global safe havens

Throughout history, in times of crisis, investors have turned to the U.S. market for safety. Despite talk of the U.S. dollar losing its safe haven status, it appears investors still very much prefer to hold U.S. dollars during times of crisis. The greenback has even bested gold during the current crisis. Since the crisis began, the dollar is up around 2% while gold is down a bit more than 3%. When in doubt, the U.S. dollars remain a favorite of investors the world over.

Conclusion

Difficult times like these — and how we respond to them — ultimately determine our ability to achieve and preserve Economic Freedom™. For investors, the best recommended course of action remains clear: look past the headlines, remain broadly diversified, and stay focused on your long-term plan.

If you have questions, concerns, or simply want to talk through what you are seeing and feeling, please reach out. That is exactly what we are here for.

Click here for more insights from our CIO. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Home » Insights » Market Commentary » The Case for Calm Amid War and Oil Crisis: Insights From Our CIO

The Case for Calm Amid War and Oil Crisis: Insights From Our CIO

Donald Calcagni, MBA, MST, CFP®, AIF®

Chief Investment Officer

Mercer Advisors CIO Don Calcagni explains why this is not a moment for bold portfolio moves.

As the Iran war continues into its second week, oil and global equity markets continue to deteriorate. The longer the conflict persists, the higher energy prices are likely to rise with growing consequences for the global economy and financial markets. Within a 24-hour period on Sunday and Monday, oil prices shot as high as $118 a barrel and as low as $84 a barrel, underscoring the exceptional lack of clarity about the direction of the conflict.

We acknowledge the tremendous human costs and suffering caused by this war; our thoughts are with the families and communities affected, and with our servicemen and women in uniform. We are monitoring developments closely, and our key message remains straightforward: we are here, we are fully engaged, and we believe this is a time for steadiness rather than reaction.

Whiplash as the market assesses the possibility of a longer war

While the market’s initial reaction to the conflict was somewhat muted, several recent developments have raised the possibility of a more prolonged conflict. The first was President Trump’s demand on Friday for Iran’s unconditional surrender, followed by Iran’s announcement yesterday of Mojtaba Khamenei — who, as the son of Ayatollah Ali Khamenei, is thought to be ideologically aligned with the previous regime — as the country’s new supreme leader. Finally, Iran has not signaled a willingness to negotiate with Israel and the U.S.

This is likely to be a period where the tenor of commentary can shift rapidly, and the situation on the ground can change quickly. This is unlikely to be the last moment of market whiplash associated with the conflict, which is all the more reason to remain cautious in making any adjustments to our portfolio.

A few key takeaways

During challenging markets, it’s important to look through the barrage of negative news to identify meaningful lessons for investors. We think several are worth highlighting:

First, globally diversified portfolios were well-positioned coming into the conflict. Global stocks across the board finished February with handsome year-to-date gains. International developed and emerging markets stocks were up double digits.

Table 1: Year-to-date returns of major indexes before the conflict began and as of March 9

Diversified investments in developed markets, emerging markets, and bonds were in a significantly stronger position than the S&P 500 alone before the start of the conflict. Despite dropping sharply in the early days of the conflict, international stocks and both U.S. and global bonds have outperformed U.S. equities year-to-date.

Markets are resilient in the long run

Our advice to remain calm and stay the course is informed by decades of real-world experience and nearly a century of empirical evidence (see below graphic from Avantis Investors). And what we’ve learned from such evidence is that all crises ultimately have a beginning, a middle, and an end. This one too shall end. While remaining calm and staying the course can be uncomfortable sometimes, market history teaches us that remaining well-diversified has historically been the best course of action during such crises.

Graphic 1: Markets have risen over time through major military conflicts.

The U.S. dollar remains one of the world’s most favored global safe havens

Throughout history, in times of crisis, investors have turned to the U.S. market for safety. Despite talk of the U.S. dollar losing its safe haven status, it appears investors still very much prefer to hold U.S. dollars during times of crisis. The greenback has even bested gold during the current crisis. Since the crisis began, the dollar is up around 2% while gold is down a bit more than 3%. When in doubt, the U.S. dollars remain a favorite of investors the world over.

Conclusion

Difficult times like these — and how we respond to them — ultimately determine our ability to achieve and preserve Economic Freedom™. For investors, the best recommended course of action remains clear: look past the headlines, remain broadly diversified, and stay focused on your long-term plan.

If you have questions, concerns, or simply want to talk through what you are seeing and feeling, please reach out. That is exactly what we are here for.

Click here for more insights from our CIO. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Explore More

The Economic and Market Impact of the Iran War After One Month: Insights From Our CIO

Using Retirement Trusts to Protect and Transfer IRAs

Personal Umbrella Insurance: FAQs to Help Protect Your Wealth