Like many of you, we’ve been closely following the news around escalating military actions involving Iran and the resulting volatility in global markets. We know this kind of coverage can raise difficult questions — not only for the world, but about your families, and your financial lives as well. Please know that we are watching closely too, and that our most important message right now is a simple one: we are here, we are attentive, and we believe this is a time for steadiness, not reaction.

What has happened?

Two major developments have reintroduced significant geopolitical uncertainty in the past two weeks.

First, the Supreme Court ruling on tariffs

On Feb. 20, 2026, the Supreme Court issued a 6-3 decision ruling that the sweeping tariffs imposed by the Trump administration under the International Emergency Economic Powers Act exceeded the president’s legal authority. The ruling invalidated a substantial portion of the tariff regime that has been in place over the past year. The administration has since moved quickly to invoke alternative legal authority, and trade policy continues to evolve. The situation remains fluid, with new measures announced and legal challenges likely to continue.

Second, recent military strikes on Iran

This past Saturday, Feb. 28, the U.S. and Israel launched a coordinated military operation targeting Iranian leadership and military infrastructure. Iran has responded with retaliatory strikes in the region, and the conflict appears to be ongoing and expanding.

Before turning to any discussion of markets, we want to pause and acknowledge what this means on a human level. War brings loss of life, loss of safety, and loss of certainty for people on all sides. Our thoughts are with the families and communities affected around the world, and among our own servicemen and women. The financial implications of these global events, while important to address, are secondary to that human reality.

The “Fog of War” and why this is not a moment for big investment moves

Military strategists speak of the “fog of war”: the idea that during conflict, information is incomplete, rapidly changing, and often contradictory. That description fits the current environment precisely. In the days since the strikes on Iran, the situation has shifted by the hour: new retaliatory actions, diplomatic statements from allies and adversaries, evolving reports on casualties and infrastructure, and conflicting signals about where this leads next.

This fog is precisely why we believe it would be a mistake to make significant portfolio changes right now. Large, reactive moves made in moments of maximum uncertainty, when headlines are loudest and emotions are highest, can be among the costliest decisions investors can make. Acting on incomplete information, in either direction, is speculation. And speculation is not a strategy. We are watching, assessing, and resisting the urge to forecast outcomes that no one can reliably predict.

A note on the Strait of Hormuz

One development worth understanding is the potential impact on global energy markets. The Strait of Hormuz, a narrow waterway between Iran and the Arabian Peninsula, is one of the most strategically critical energy chokepoints in the world. Approximately 20% of all seaborne oil globally and 20% of the world’s liquefied natural gas pass through this strait daily. Any sustained disruption to traffic through Hormuz would have significant implications for global energy prices.

Markets have already begun reacting to this risk, with oil prices rising meaningfully since the strikes were announced. We are monitoring this closely, as energy prices have downstream effects on inflation, corporate costs, and consumer spending. That said, we want to be careful not to extrapolate. Energy markets have navigated geopolitical shocks before, and outcomes have varied widely.

Key indicators we are watching

Rather than making predictions, we believe it is more useful to identify the signposts we are tracking as this situation develops:

- Oil prices: A key barometer of perceived disruption risk to Middle East supply. As of Tuesday afternoon, the benchmark Brent crude index is up 13.4% since Friday. Sustained elevated prices would feed through to inflation and corporate margins.

- Gold: A traditional safe-haven asset. Rising gold prices reflect investor demand for stability and are one signal of broad risk sentiment. So far, gold is down about 3.1%.

- Interest rates (U.S. Treasuries): Markets are watching whether the Fed’s path is complicated by any energy-driven inflation. Treasury yields are a window into those expectations. The yield on the 10 year Treasury climbed to 12 basis points and the 30-year up 10 basis points.

- The U.S. Dollar: The dollar tends to strengthen in risk-off environments. Significant moves in either direction carry implications for international investments and trade competitiveness. The dollar has strengthened 1.6%.

- Defense stocks: Already elevated given the global security environment, defense sector performance reflects both government spending expectations and the broader geopolitical temperature. Defense stock, as measured by the S&P 500 Aerospace and Defense Industry was up 0.4%.

- The VIX: Often called the “fear index,” the VIX measures expected volatility in the S&P 500. Elevated readings signal heightened uncertainty; we watch for both spikes and the pace of any subsequent normalization. The VIX climbed 20%, the highest since mid-November 2025.

These indicators, taken together, give us a more complete picture of how markets are processing this news than any single headline. Outside of energy markets that are most immediately impacted, capital markets seem to be taking more of a “wait-and-see” approach by not currently exhibiting irregularly sharp movements. We will continue monitoring the situation and will communicate if meaningful shifts occur.

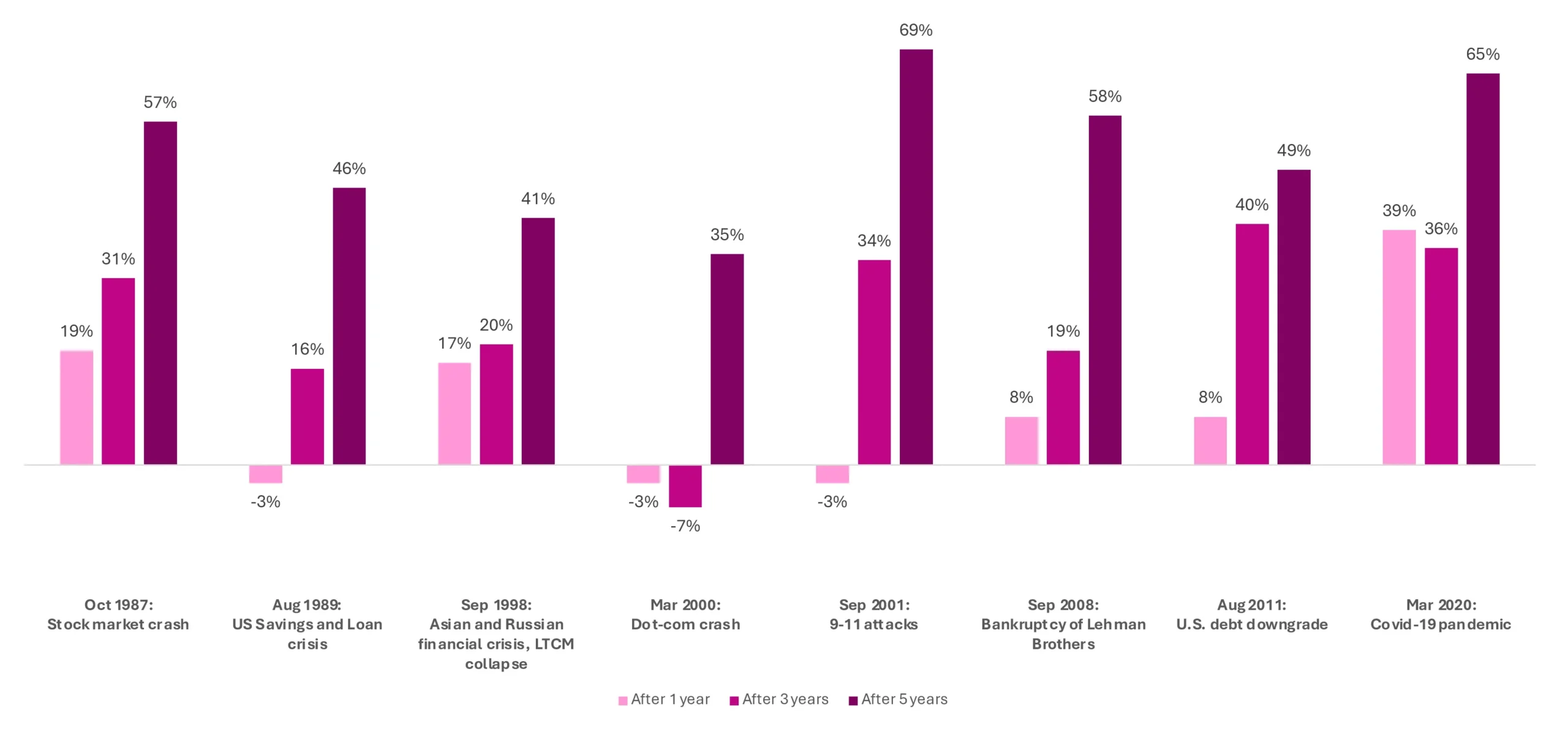

History as our guide

In moments of uncertainty, it can be grounding to look at how markets have responded to past crises. The accompanying chart illustrates the performance of a diversified 60/40 portfolio in the years following several major historical shocks — including the 1987 stock market crash, the U.S. savings and loan crisis, the dot‑com collapse, the September 11th attacks, the global financial crisis, the U.S. debt downgrade, and the COVID‑19 pandemic.

Figure 1: The market’s response to crisis

Cumulative total return of a balanced 60% stocks/40% bonds strategy

Source: Dimensional Fund Advisors. For informational purposes only and illustrative purposes only, not intended as a recommendation of Dimensional Fund Advisors or Dimensional’s investment strategies. Represents cumulative total returns of a Dimensional Index Allocation invested on the first day of the following calendar month of the event noted. Assumes all strategies have been rebalanced monthly. All performance results of the Dimensional Index Allocations are based on performance of indices with model/backtested asset allocations; the performance was achieved with the benefit of hindsight, it does not represent actual investment strategies. The model’s performance does not reflect advisory fees or other expenses associated with the management of an actual portfolio. There are limitations inherent in model allocations. In particular, model performance may not reflect the impact that economic and market factors may have had on the advisor’s decision making if the advisor were actually managing client money. Past performance is no guarantee of future results. The Dimensional Indices used in the construction of the Dimensional Index Allocations represent academic concepts that may be used in portfolio construction. The Dimensional Index Allocations and the indices are not available for direct investment or for use as a benchmark. The Dimensional Index Allocation and index returns are not representative of actual portfolios and do not reflect costs and fees associated with an actual investment.

Resilience after market stress

While each event triggered immediate market stress — and in several cases negative one‑year returns — the pattern that emerges over longer horizons is one of resilience. Across all events shown, the five‑year cumulative returns were positive, often significantly so. For example, five‑year returns following past crises ranged from the mid‑30% range to nearly 70%. Although the path was rarely smooth, investors who maintained a disciplined, long‑term approach were historically rewarded as markets recovered.

The chart does not predict what will happen next — but it does remind us that, through a wide range of crises over many decades, markets have recovered every time so far.

Three things to remember right now

- We are paying close attention, so you don’t have to react. Monitoring markets and geopolitical developments in real time is our job. We are actively reviewing portfolios, stress-testing exposures, and staying in close contact with our research partners. You do not need to act on every headline. That burden belongs to us, not you.

- Uncertainty is not a reason to abandon your plan; it is a reason to trust it. The portfolios we have built are designed for environments exactly like this one. Diversification across and within asset classes does not eliminate volatility, but it does help mitigate the effects of these events, however dramatic. Reacting to the fog of war by making large portfolio moves trades one risk for another, often at the worst possible moment

- History is on the side of the patient investor. Markets have recovered from every major crisis on record — wars, financial collapses, geopolitical shocks, and pandemics. The investors who benefited were not those who predicted the outcomes correctly; they were those who stayed diversified, remained disciplined, and resisted the pull of panic. We believe the same principle applies today.

If you have questions, concerns, or simply want to talk through what you are seeing and feeling, please reach out. That is exactly what we are here for.

Click here for past insights about wealth management and other interesting topics. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Home » Insights » Market Commentary » A Return of Geopolitical Uncertainty

A Return of Geopolitical Uncertainty

David Krakauer, CFA®, CRPS®

Vice President, Portfolio Management

Mercer Advisors VP of Portfolio Management David Krakauer explains what to watch amid the Iran conflict and why this is a moment not to overreact.

Like many of you, we’ve been closely following the news around escalating military actions involving Iran and the resulting volatility in global markets. We know this kind of coverage can raise difficult questions — not only for the world, but about your families, and your financial lives as well. Please know that we are watching closely too, and that our most important message right now is a simple one: we are here, we are attentive, and we believe this is a time for steadiness, not reaction.

What has happened?

Two major developments have reintroduced significant geopolitical uncertainty in the past two weeks.

First, the Supreme Court ruling on tariffs

On Feb. 20, 2026, the Supreme Court issued a 6-3 decision ruling that the sweeping tariffs imposed by the Trump administration under the International Emergency Economic Powers Act exceeded the president’s legal authority. The ruling invalidated a substantial portion of the tariff regime that has been in place over the past year. The administration has since moved quickly to invoke alternative legal authority, and trade policy continues to evolve. The situation remains fluid, with new measures announced and legal challenges likely to continue.

Second, recent military strikes on Iran

This past Saturday, Feb. 28, the U.S. and Israel launched a coordinated military operation targeting Iranian leadership and military infrastructure. Iran has responded with retaliatory strikes in the region, and the conflict appears to be ongoing and expanding.

Before turning to any discussion of markets, we want to pause and acknowledge what this means on a human level. War brings loss of life, loss of safety, and loss of certainty for people on all sides. Our thoughts are with the families and communities affected around the world, and among our own servicemen and women. The financial implications of these global events, while important to address, are secondary to that human reality.

The “Fog of War” and why this is not a moment for big investment moves

Military strategists speak of the “fog of war”: the idea that during conflict, information is incomplete, rapidly changing, and often contradictory. That description fits the current environment precisely. In the days since the strikes on Iran, the situation has shifted by the hour: new retaliatory actions, diplomatic statements from allies and adversaries, evolving reports on casualties and infrastructure, and conflicting signals about where this leads next.

This fog is precisely why we believe it would be a mistake to make significant portfolio changes right now. Large, reactive moves made in moments of maximum uncertainty, when headlines are loudest and emotions are highest, can be among the costliest decisions investors can make. Acting on incomplete information, in either direction, is speculation. And speculation is not a strategy. We are watching, assessing, and resisting the urge to forecast outcomes that no one can reliably predict.

A note on the Strait of Hormuz

One development worth understanding is the potential impact on global energy markets. The Strait of Hormuz, a narrow waterway between Iran and the Arabian Peninsula, is one of the most strategically critical energy chokepoints in the world. Approximately 20% of all seaborne oil globally and 20% of the world’s liquefied natural gas pass through this strait daily. Any sustained disruption to traffic through Hormuz would have significant implications for global energy prices.

Markets have already begun reacting to this risk, with oil prices rising meaningfully since the strikes were announced. We are monitoring this closely, as energy prices have downstream effects on inflation, corporate costs, and consumer spending. That said, we want to be careful not to extrapolate. Energy markets have navigated geopolitical shocks before, and outcomes have varied widely.

Key indicators we are watching

Rather than making predictions, we believe it is more useful to identify the signposts we are tracking as this situation develops:

These indicators, taken together, give us a more complete picture of how markets are processing this news than any single headline. Outside of energy markets that are most immediately impacted, capital markets seem to be taking more of a “wait-and-see” approach by not currently exhibiting irregularly sharp movements. We will continue monitoring the situation and will communicate if meaningful shifts occur.

History as our guide

In moments of uncertainty, it can be grounding to look at how markets have responded to past crises. The accompanying chart illustrates the performance of a diversified 60/40 portfolio in the years following several major historical shocks — including the 1987 stock market crash, the U.S. savings and loan crisis, the dot‑com collapse, the September 11th attacks, the global financial crisis, the U.S. debt downgrade, and the COVID‑19 pandemic.

Figure 1: The market’s response to crisis

Cumulative total return of a balanced 60% stocks/40% bonds strategy

Source: Dimensional Fund Advisors. For informational purposes only and illustrative purposes only, not intended as a recommendation of Dimensional Fund Advisors or Dimensional’s investment strategies. Represents cumulative total returns of a Dimensional Index Allocation invested on the first day of the following calendar month of the event noted. Assumes all strategies have been rebalanced monthly. All performance results of the Dimensional Index Allocations are based on performance of indices with model/backtested asset allocations; the performance was achieved with the benefit of hindsight, it does not represent actual investment strategies. The model’s performance does not reflect advisory fees or other expenses associated with the management of an actual portfolio. There are limitations inherent in model allocations. In particular, model performance may not reflect the impact that economic and market factors may have had on the advisor’s decision making if the advisor were actually managing client money. Past performance is no guarantee of future results. The Dimensional Indices used in the construction of the Dimensional Index Allocations represent academic concepts that may be used in portfolio construction. The Dimensional Index Allocations and the indices are not available for direct investment or for use as a benchmark. The Dimensional Index Allocation and index returns are not representative of actual portfolios and do not reflect costs and fees associated with an actual investment.

Resilience after market stress

While each event triggered immediate market stress — and in several cases negative one‑year returns — the pattern that emerges over longer horizons is one of resilience. Across all events shown, the five‑year cumulative returns were positive, often significantly so. For example, five‑year returns following past crises ranged from the mid‑30% range to nearly 70%. Although the path was rarely smooth, investors who maintained a disciplined, long‑term approach were historically rewarded as markets recovered.

The chart does not predict what will happen next — but it does remind us that, through a wide range of crises over many decades, markets have recovered every time so far.

Three things to remember right now

If you have questions, concerns, or simply want to talk through what you are seeing and feeling, please reach out. That is exactly what we are here for.

Click here for past insights about wealth management and other interesting topics. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Explore More

Washington’s Income Tax Debate: Capital Gains, the Millionaires’ Tax, and What Comes Next

Estate Planning for Women Who Expect to Live — and Lead — Longer

The Stock Market Was Strong Entering the Turmoil of the Iran War