Taking a career break is a significant decision, especially for women. The “motherhood penalty” refers to the financial setbacks women face when they leave the workforce to care for their children, affecting both their immediate wages and lifetime earnings. On average, women working full-time earn about 84% of what their male counterparts make.1 This disparity can widen for those who take career breaks. For instance, in 2023, full-time working mothers earned $17,000 less annually than full-time working fathers, potentially leading to a $510,000 wage gap over a 30-year career.2 Consequently, women often have lower average incomes in retirement, resulting in reduced financial stability in their later years.

When considering extended maternity or caregiving leave, financial implications are undoubtedly significant. However, it’s equally important to reflect on the personal needs and rewards associated with each choice. A 2024 international study revealed that mothers returning to the workforce experienced better work relationships, felt more appreciated by colleagues, and enhanced their time management and problem-solving skills.3

Evaluating personal and family needs

Nearly a quarter of mothers cite their primary motivation for leaving their jobs as the desire to stay home with their children.4 If being a stay-at-home mom is a feasible and comfortable option for your family, it might be worth embracing the “motherhood advantage” rather than focusing on the so-called “penalty.” For example, 70% of stay-at-home moms report feeling less stressed compared to working mothers, and their children are 32% less likely to experience anxiety or depression.5

Mothers also highlight the importance of flexibility and affordable childcare when deciding whether to return to the workforce. Negotiating leave options, part-time schedules, or remote work with your employer can significantly aid in balancing professional and personal responsibilities.

When you decide to return to work, it’s natural to feel pangs of guilt and the urge to apologize. Instead, try transforming these feelings into expressions of gratitude. You have the opportunity to use your skills, education, and energy to support your family. It’s both a right and a privilege — take pride in earning financial compensation for your hard work. Whether driven by passion for your profession or a desire for financial independence, embrace your decision to return to paid work with confidence and satisfaction.

Considering financial strategies

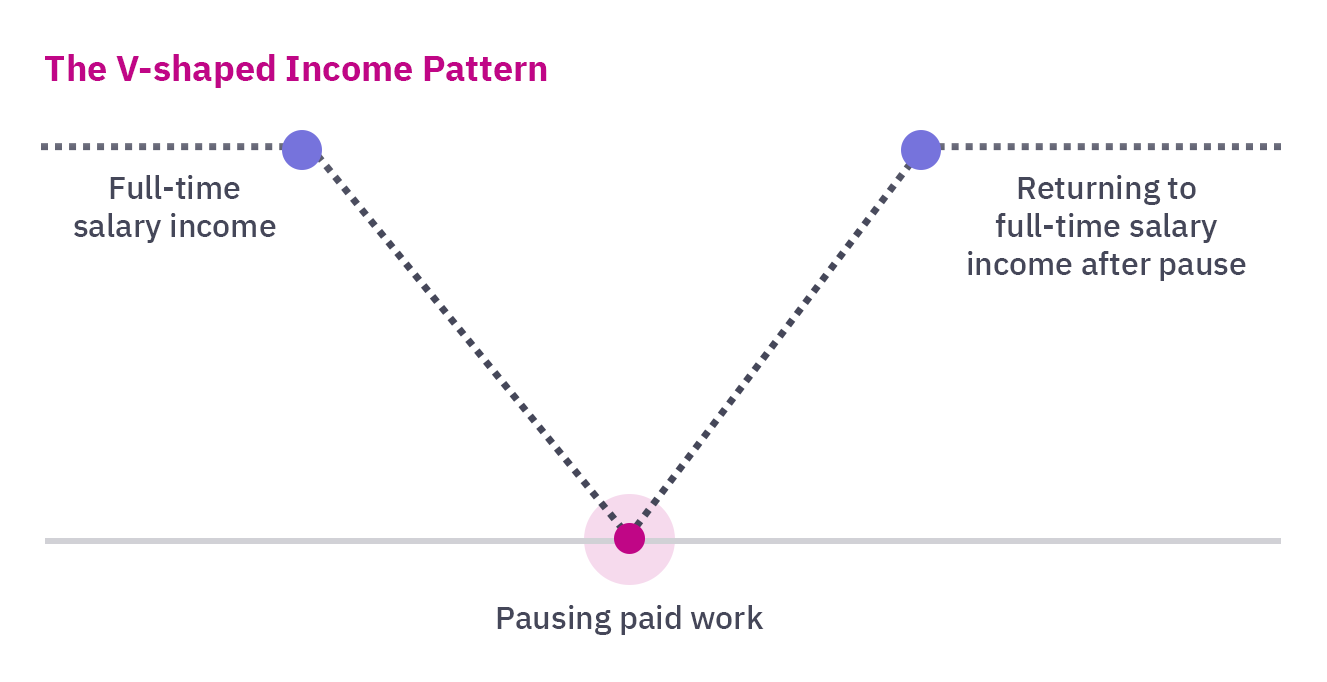

Customizing a financial plan is always important, but it’s particularly crucial for women affected by the V-shaped income pattern, which represents going from a full-time salaried position to no income and then returning to a full-time salaried position. Whether you return to the workforce months after leaving your job or take a career break for years, having a comprehensive financial plan can help you keep track of investments, retirement, or savings accounts; make strategic life decisions at meaningful milestones; guide your children’s future; and secure your own long-term financial security.

Here are a few saving strategies to incorporate into your “economic self-care routine” if you are taking a career break or caregiving leave:

- 529 college savings plan: Do not sacrifice your retirement savings to pay for your child’s college degree! It’s important to find the right balance between planning for retirement and college expenses. A 529 college savings plan is a fantastic way to invest in future education expenses — the funds grow tax-free, and the gains are not taxable if used for qualifying educational expenses. For baby and birthday gifts, you could request contributions to a 529 or put an equivalent amount of gift money received into the college fund. At a child’s birth, that 18-year runway gives compounding interest ample time to do its magic. Gifting a legacy of education with a 529 plan is ideal for grandparents!

- Roth individual retirement account (IRA): Don’t miss opportunities to leverage tax savings and strategies when your income shifts. A classic example is contributing to a Roth IRA versus a Traditional IRA. When your income is at a lower tax level, a deductible contribution to a Traditional IRA may not be advantageous. Assets in a Roth IRA grow tax-free and there is no tax due when withdrawn at retirement. There are even exemptions that allow for earlier withdrawals free of penalties.

- Health savings account (HSA): Another tax-free vehicle you can use to grow savings is an HSA. If you are enrolled in a high-deductible health care plan, you can contribute annually to an HSA, which creates a cushion to cover medical expenses. However, if you are able to avoid drawing down on the funds, the contributions can continue to grow tax-free. The HSA , with its tax-deductible contribution, can serve in long-term planning as a quasi-retirement fund.

|

Returning to the workforce

Perhaps you’ve had, or are, an invaluable female mentor in your professional life. The international study revealed that women supporting each other with shared experiences and expertise enable a mother’s career progression. In addition, having a support network that includes family, friends, and the community can help boost your career advancement. Closer to home, if you have a partner sharing responsibilities, asking for an equitable contribution to family and household care — if it doesn’t already exist — will likely allow you to feel more empowered to pursue your professional goals. Studies have shown that when husbands and wives are both working full-time, the woman still spends about 2 hours per week more on caregiving and 2 1/2 hours more on housework.9

You can take control of your career and earning power by seeking out organizations that accommodate women in caregiving roles, as well as offer programs for women returning to work. While your career is on pause, consider continuing your education or getting certified in a specialty. Network with professionals in your field, whether in-person, through social media, or professional online platforms.

Taking charge

Unfortunately, our society is still many years away from closing the wage gap that women experience as well as the “penalty” for having children. Women who leave full-time work have a wage drop of 5% to 20% compared to men who have a wage increase, or “fatherhood bonus,” of 6%.10 It’s up to each individual woman to determine how they will navigate the professional and financial challenges of taking a career break. While the challenges are significant, they are not insurmountable.

With careful planning and a supportive network, you can navigate extended maternity or caregiving leave successfully, ensuring that your professional and personal lives are enriched. Ultimately, recognizing and addressing these key areas can help empower you to make informed choices that align with your long-term goals and wellbeing.

At Mercer Advisors, almost 50% of our client-facing associates are women. We help women create plans that fit their needs. If you are interested in having a financial partner who understands women and wealth, let’s talk.

- “Gender Pay Gap Statistics In 2024,” Forbes Advisor, March 1, 2024.

- “What is the Motherhood Penalty? New Gender Pay Gap Report Explained,” MSN, July 8, 2024.

- “The Impact of Motherhood on Women’s Career Progression: A Scoping Review of Evidence-Based Interventions,” MDPI, March 26, 2024.

- “The number of stay-at-home mothers rose dramatically in the US last year,” Quartz, May 16, 2023.

- “Stats Show Benefits of Stay at Home Mom: Less Stress, Savings, Happiness,” Gitnux, July 17, 2024.

- “Women Experience a ‘Motherhood Penalty.’ For Dads, There’s a Wage ‘Bonus’,” CNBC, March 26, 2024.

- “What You Need to Know About the Gender Wage Gap,” U.S. Department of Labor Blog, March 12, 2024.

- “Employers woo women back to work from career breaks,” Financial Times, Oct. 16, 2023.

- “More women are out-earning their husbands but still picking up a heavier load at home,” CNBC, May 24, 2023.

- “The Motherhood Penalty in the Workplace,” Psychology Today, Feb. 13, 2023.