Deciding when to start collecting Social Security is a milestone in retirement planning. Claiming benefits too soon may leave money on the table, while waiting too long could mean you don’t fully benefit from what you’ve earned. That’s where your Social Security break-even age comes in.

What is the Social Security break-even age?

The break-even age is the point at which the total amount of Social Security benefits you’d receive by claiming early equals the amount you’d receive by delaying. For most people, this age falls between 78 and 81.

Here’s how it works:

- Claim early: You’ll receive smaller checks, but more of them since you’ll start collecting Social Security benefits sooner.

- Delay benefits: Your monthly payment will be larger, but you’ll collect fewer checks overall.

When the cumulative totals of those two choices line up, you’ve hit your break-even point.

Knowing your break-even age matters

Understanding your Social Security break-even age can help you make a more informed retirement income strategy. Your outlook on longevity and lifestyle should help guide your choice.

- If you expect to live beyond your break-even age, delaying benefits could increase your lifetime payout.

- If health concerns or family history suggest you may not live past that age, claiming early may allow you to enjoy benefits sooner.

The role of full retirement age

Your full retirement age (FRA) — between ages 65 and 67, depending on your birth year — affects how your benefits are calculated. If you:

- Claim before FRA: Benefits are reduced permanently.

- Claim at FRA: You’ll receive your full benefit amount.

- Delay past FRA (up to age 70): Benefits can increase each month you wait.

FRA based on birth year

| Year of Birth | Full Retirement Age |

|---|---|

| 1937 or earlier | 65 |

| 1938 | 65 and 2 months |

| 1939 | 65 and 4 months |

| 1940 | 65 and 6 months |

| 1941 | 65 and 8 months |

| 1942 | 65 and 10 months |

| 1943 – 1954 | 66 |

| 1955 | 66 and 2 months |

| 1956 | 66 and 4 months |

| 1957 | 66 and 6 months |

| 1958 | 66 and 8 months |

| 1959 | 66 and 10 months |

| 1960 and over | 67 |

How to calculate your break-even age

While an online Social Security calculator can simplify the math, you can also estimate manually in a few steps.

- Get your benefit estimates: Check your Social Security statement for projected benefits at age 62, FRA, and 70.

- Find the difference: Multiply the early benefit by the number of months you’d delay.

- Apply the formula: Divide the missed amount by the monthly difference. Add that result to the delayed age to find your break-even age.

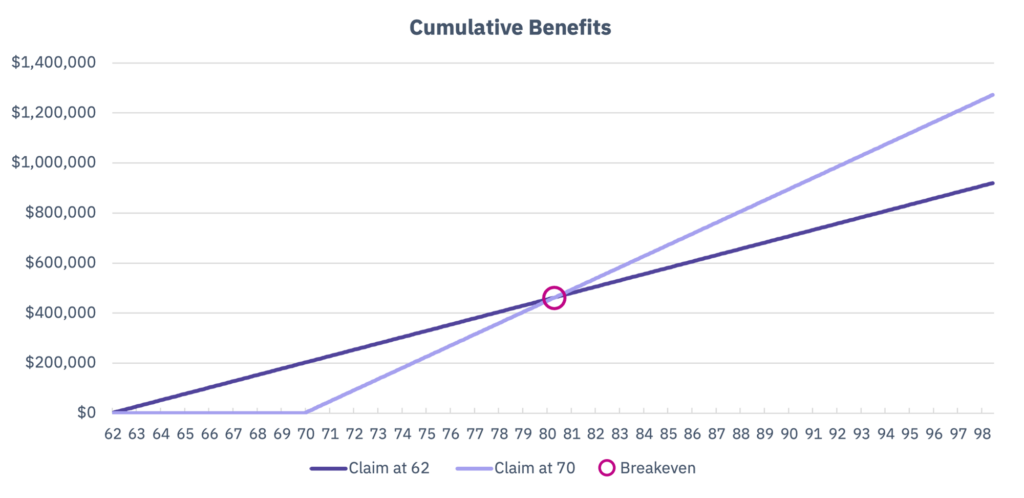

For example, if Bill’s Social Security benefits are $2,100/month at age 62 and $3,720/month at age 70, his:

- Monthly difference is $1,620

- Missed opportunity cost is $2,100 x 96 months = $201,600

- Break-even point is $201,600 / $1,620 = 124 months (about 10 years)

- Break-even age is 80 (70 + 10 = 80)

In this case, if Bill lives beyond age 80, it’s more profitable if he waits until age 70 to claim Social Security benefits.

Other factors to consider before claiming

While the break-even age is a helpful benchmark, it’s not the only factor in your decision. Consider:

- Financial goals: Immediate cash flow vs. long-term security.

- Other income sources: Pensions, savings, or investments can affect timing.

- Current expenses: Debt, medical costs, or lifestyle needs may influence you to claim earlier.

- Health and longevity: Family history and personal health play a major role.

- Work plans: Continuing to work could increase your future benefit.

- Investment returns: The higher your rate of return on investible assets, the sooner you would generally want to claim benefits.

- Inflation: Since Social Security benefits are adjusted for inflation, delaying benefits could make more sense in higher inflationary environments.

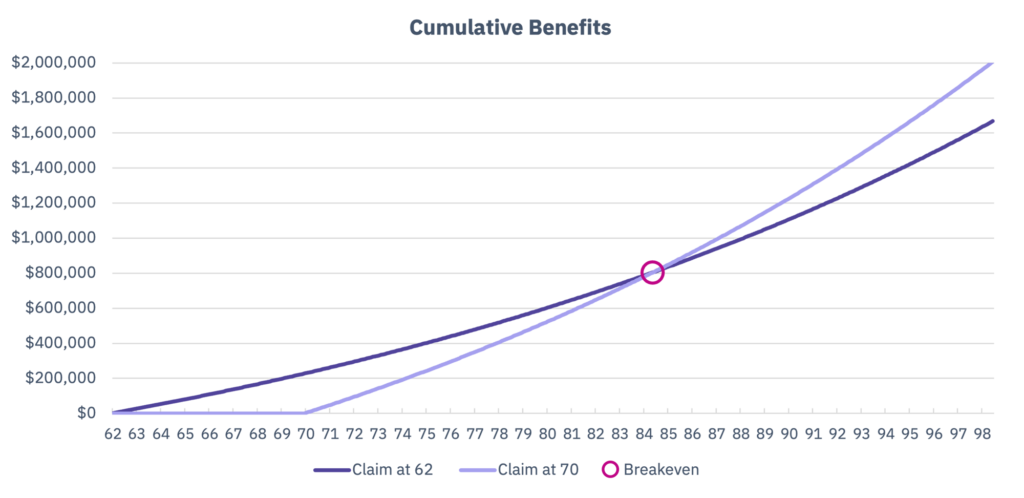

Looking back at our example for Bill, if he could invest his benefits at a real rate of return of 3% (approximately inflation plus 3%), it would take about four years longer to break even from the delay.

Your Social Security break-even age offers valuable insight into whether claiming early or delaying aligns best with your retirement plans. But it’s only one piece of the puzzle. Balancing it with your financial goals, health, lifestyle, and income needs can help you make the best decision for your future.

Visit our library of Social Security articles to learn more.

For more information, contact your wealth advisor. Not a client?

Mercer Advisors Inc. is a parent company of Mercer Global Advisors Inc. and is not involved with investment services. Mercer Global Advisors Inc. (“Mercer Advisors”) is registered as an investment advisor with the SEC. The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. The hypothetical example above is for illustrative purposes only. Third-party links are presented for information and educational purposes only.

For financial planning advice specific to your circumstances, talk to a qualified professional at Mercer Advisors.

Certified Financial Planner Board of Standards, Inc. (CFP Board) owns the CFP® certification mark, the CERTIFIED FINANCIAL PLANNER® certification mark, and the CFP® certification mark (with plaque design) logo in the United States, which it authorizes use of by individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.