When you invest, you accept that the future is uncertain. Some risks are measurable, where we can estimate the odds. Others, like an unexpected war, come with outcomes that simply cannot be measured in advance. Right now, the conflict with Iran falls squarely in that second category, and we’ve heard from many of you asking the same question: Will this push the U.S. into recession?

We acknowledge that headlines about war and recession carry real weight, regardless of what the data shows however, our short answer is “probably not,” and below is how we’re thinking through it.

What do we know?

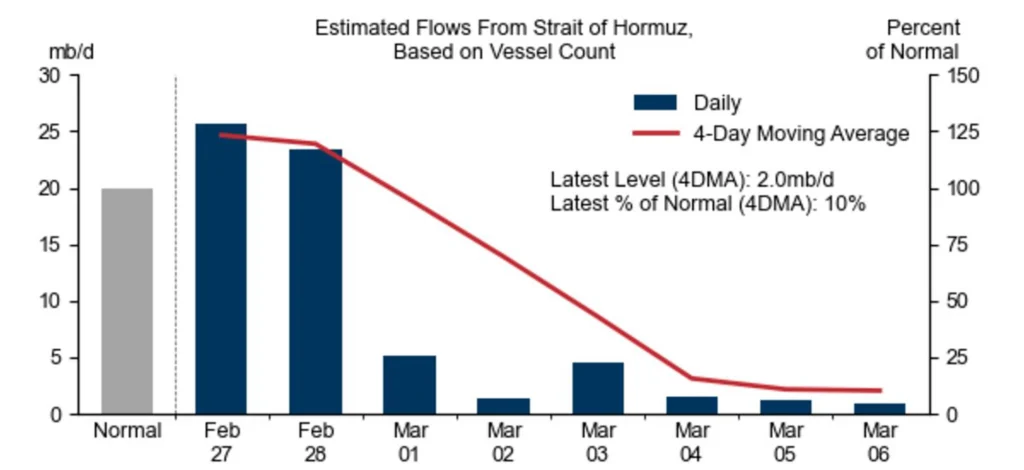

Since the outbreak of the war, energy shipments through the Strait of Hormuz have fallen approximately 90%. Typically, 20 million barrels per day of such products flow through the Strait (see gray bar below), which accounts for roughly 25% of the global seaborne oil trade. The most recent data shows just 2 million barrels per day (blue bar on the right) getting through.

Chart 1: Average Daily Flows Through the Strait of Hormuz Are Down 90%

Vessel count as percent of normal is based on an average of Bloomberg, S&P, and Kpler data on the daily number of oil tankers crossing the Strait of Hormuz, relative to Jan 1- Feb 14 average. Flows are estimated by applying this proportion to assumed normal flows of 20 million barrels/day. Source: Bloomberg, S&P Global, Kpler, Goldman Sachs, Mercer Advisors, as of 3/9/26.

There is currently limited ability to redirect these flows via regional pipelines in the short term, but that pipeline capacity accounts for less than half of the reduction in shipments through the Strait. This means the global economy is facing a significant energy supply shock.

On March 12, the International Energy Agency announced plans to release 400 million barrels from global reserves of its member countries. That sounds like a lot, and it helps, but at current reduced flow rates, it would only offset the shortfall for roughly three weeks.

This assumes that demand stays constant, and it’s important to note that slower economic activity could reduce oil demand and ease prices.

What do supply shocks mean for the economy?

A supply shock is when something disrupts the availability of a key resource. In this case, that is oil. When oil becomes scarce, prices at the pump and across the economy rise. When prices rise, businesses and consumers feel the squeeze, and economic growth can slow.

Economists call the combination of rising prices and slowing growth stagflation. This term tends to make people nervous, largely because of its association with the difficult 1970s. However, based on market signals thus far, a repeat of the 1970s does not appear likely.

Would an oil shock push the U.S. into recession?

Currently, we believe no. The outcome will depend on how high prices rise, how long they stay elevated, and whether other headwinds emerge for the economy alongside this supply shock.

Here’s what the data shows:

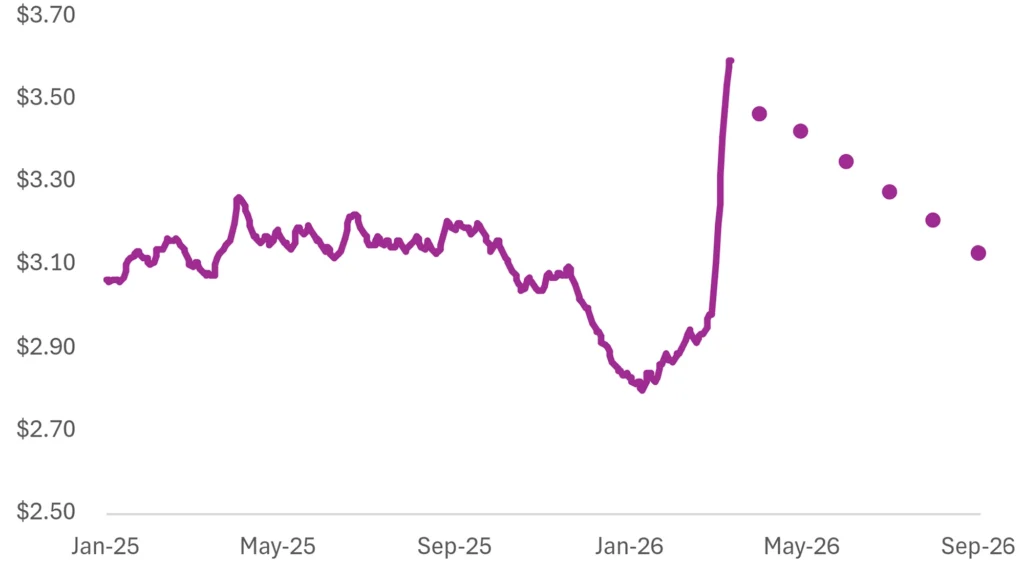

Gas prices are a useful real-time indicator. Before the conflict, the national average was just under $3 per gallon. By Wednesday, March 11, it was $3.54. That’s a noticeable jump. However, futures markets (essentially, what traders expect gas to cost in the future) are pricing September gasoline at roughly $2.55 per gallon. Add typical taxes, and that implies retail gasoline prices falling back to around $3.10 by fall. In other words, the market currently expects the price spike to be temporary.

Chart 2: National Average Retail Gasoline Prices

Dots show expected gasoline prices based on current futures plus 55 cents for taxes. Source: American Automobile Association, Bloomberg Finance, LP, Mercer Advisors, as of 3/12/26.

Estimates of the impact

To put some numbers around the economic impact, JPMorgan estimates that a prolonged 10% increase in oil prices raises the inflation rate by about 0.1 percentage points and reduces economic growth by about 0.15 percentage points. Oil is currently about 30% higher than pre-conflict levels. Therefore, if prices stayed here over the course of the year (which markets don’t expect) that would add roughly 0.3 percentage points to inflation and shave about 0.45 percentage points off growth over the next year.

That’s a headwind, but not a devastating one: the U.S. economy grew more than 2% in real terms last year and was forecasted to grow at about the same rate before the conflict began.

One caveat worth noting: Gasoline prices are only one mechanism through which the U.S. will feel the effect of higher oil prices. Other costs, such as fertilizer, are likely to be adversely impacted as planting season begins. Higher planting costs such as these could translate into higher food costs in coming months.

Additional context

Structural changes in the U.S. economy in recent decades also reduce the potential negative impact of an adverse oil supply shock. Today, the U.S. is a net oil exporter, meaning the U.S. produces so much oil that it exports more than it imports from abroad. Higher oil prices still hurt consumers, but domestic producers benefit and offset some of the impact in measures of aggregate economic growth.

The energy intensity of the U.S. economy is also lower now than in past decades (though it remains higher than in many other developed countries). In other words, the U.S. economy burns less oil per unit of GDP than in the past, which dampens the impact of oil price spikes on economic production and consumption.

Finally, some recent historic context: When Russia invaded Ukraine in early 2022, oil prices spiked 45% and helped push inflation to 9%. The U.S. still avoided recession, though it was a difficult period for markets and household budgets.

Key takeaways

- The price spike of oil is expected to be temporary, as markets are currently pricing in return to near-normal gas prices by fall. That could change, but it’s an important baseline.

- A recession is not the most likely outcome, yet. Based on current price levels and market expectations, the supply shock alone is not large enough or sustained enough to stall the U.S. economy. It would take significantly higher oil prices, held for a longer period, to tip the scales.

- Inflation will likely feel the impact before growth does. You’ll likely notice higher prices at the gas station before any broader economic slowdown shows up. Inflation will feel the impact before growth does. That’s the typical pattern with supply shocks.

This remains a fluid situation, and we are monitoring it closely. While uncertainty is uncomfortable, it is not the same as a downturn. We will keep you updated as conditions evolve, and as always, please don’t hesitate to reach out with questions.

Click here for more insights from our CIO and investment team. Not a Mercer Advisors client but interested in more information? Let’s talk.

Home » Insights » Market Commentary » Will War with Iran Push the U.S. into Recession?

Will War with Iran Push the U.S. into Recession?

David Krakauer, CFA®, CRPS®

Vice President, Portfolio Management

The dramatic increase in oil prices has not thus far reached a level that would tip the U.S. economy into recession.

When you invest, you accept that the future is uncertain. Some risks are measurable, where we can estimate the odds. Others, like an unexpected war, come with outcomes that simply cannot be measured in advance. Right now, the conflict with Iran falls squarely in that second category, and we’ve heard from many of you asking the same question: Will this push the U.S. into recession?

We acknowledge that headlines about war and recession carry real weight, regardless of what the data shows however, our short answer is “probably not,” and below is how we’re thinking through it.

What do we know?

Since the outbreak of the war, energy shipments through the Strait of Hormuz have fallen approximately 90%. Typically, 20 million barrels per day of such products flow through the Strait (see gray bar below), which accounts for roughly 25% of the global seaborne oil trade. The most recent data shows just 2 million barrels per day (blue bar on the right) getting through.

Chart 1: Average Daily Flows Through the Strait of Hormuz Are Down 90%

Vessel count as percent of normal is based on an average of Bloomberg, S&P, and Kpler data on the daily number of oil tankers crossing the Strait of Hormuz, relative to Jan 1- Feb 14 average. Flows are estimated by applying this proportion to assumed normal flows of 20 million barrels/day. Source: Bloomberg, S&P Global, Kpler, Goldman Sachs, Mercer Advisors, as of 3/9/26.

There is currently limited ability to redirect these flows via regional pipelines in the short term, but that pipeline capacity accounts for less than half of the reduction in shipments through the Strait. This means the global economy is facing a significant energy supply shock.

On March 12, the International Energy Agency announced plans to release 400 million barrels from global reserves of its member countries. That sounds like a lot, and it helps, but at current reduced flow rates, it would only offset the shortfall for roughly three weeks.

This assumes that demand stays constant, and it’s important to note that slower economic activity could reduce oil demand and ease prices.

What do supply shocks mean for the economy?

A supply shock is when something disrupts the availability of a key resource. In this case, that is oil. When oil becomes scarce, prices at the pump and across the economy rise. When prices rise, businesses and consumers feel the squeeze, and economic growth can slow.

Economists call the combination of rising prices and slowing growth stagflation. This term tends to make people nervous, largely because of its association with the difficult 1970s. However, based on market signals thus far, a repeat of the 1970s does not appear likely.

Would an oil shock push the U.S. into recession?

Currently, we believe no. The outcome will depend on how high prices rise, how long they stay elevated, and whether other headwinds emerge for the economy alongside this supply shock.

Here’s what the data shows:

Gas prices are a useful real-time indicator. Before the conflict, the national average was just under $3 per gallon. By Wednesday, March 11, it was $3.54. That’s a noticeable jump. However, futures markets (essentially, what traders expect gas to cost in the future) are pricing September gasoline at roughly $2.55 per gallon. Add typical taxes, and that implies retail gasoline prices falling back to around $3.10 by fall. In other words, the market currently expects the price spike to be temporary.

Chart 2: National Average Retail Gasoline Prices

Dots show expected gasoline prices based on current futures plus 55 cents for taxes. Source: American Automobile Association, Bloomberg Finance, LP, Mercer Advisors, as of 3/12/26.

Estimates of the impact

To put some numbers around the economic impact, JPMorgan estimates that a prolonged 10% increase in oil prices raises the inflation rate by about 0.1 percentage points and reduces economic growth by about 0.15 percentage points. Oil is currently about 30% higher than pre-conflict levels. Therefore, if prices stayed here over the course of the year (which markets don’t expect) that would add roughly 0.3 percentage points to inflation and shave about 0.45 percentage points off growth over the next year.

That’s a headwind, but not a devastating one: the U.S. economy grew more than 2% in real terms last year and was forecasted to grow at about the same rate before the conflict began.

One caveat worth noting: Gasoline prices are only one mechanism through which the U.S. will feel the effect of higher oil prices. Other costs, such as fertilizer, are likely to be adversely impacted as planting season begins. Higher planting costs such as these could translate into higher food costs in coming months.

Additional context

Structural changes in the U.S. economy in recent decades also reduce the potential negative impact of an adverse oil supply shock. Today, the U.S. is a net oil exporter, meaning the U.S. produces so much oil that it exports more than it imports from abroad. Higher oil prices still hurt consumers, but domestic producers benefit and offset some of the impact in measures of aggregate economic growth.

The energy intensity of the U.S. economy is also lower now than in past decades (though it remains higher than in many other developed countries). In other words, the U.S. economy burns less oil per unit of GDP than in the past, which dampens the impact of oil price spikes on economic production and consumption.

Finally, some recent historic context: When Russia invaded Ukraine in early 2022, oil prices spiked 45% and helped push inflation to 9%. The U.S. still avoided recession, though it was a difficult period for markets and household budgets.

Key takeaways

This remains a fluid situation, and we are monitoring it closely. While uncertainty is uncomfortable, it is not the same as a downturn. We will keep you updated as conditions evolve, and as always, please don’t hesitate to reach out with questions.

Click here for more insights from our CIO and investment team. Not a Mercer Advisors client but interested in more information? Let’s talk.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors.

The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. This information is not intended as a recommendation or solicitation to buy, sell, or hold, any particular security or to engage in any particular investment strategy. Different types of investments involve varying degrees of risk, investments mentioned in this document may not be suitable for all investors. Investments are subject to market risk, including the possible loss of principal. Past performance may not be indicative of future results. Future investment performance cannot be guaranteed. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Portfolio management strategies such as diversification, asset allocation, and rebalancing do not ensure a profit or guarantee against loss. Indices are unmanaged and index returns do not include fees or expenses typically incurred in the management of an investment portfolio. Indices are not available for direct investment.

This content may contain forward looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.

Explore More

The 7 Most Common Wealth Management Mistakes — and How to Avoid Them

The Case for Calm Amid War and Oil Crisis: Insights From Our CIO

Strategic Giving: How Women Are Redefining Philanthropy