A recap of our Monday, April 6, 2020, webinar (updated as of April 22, 2020)

U.S. small businesses affected by the COVID-19 crisis qualified for forgivable loans along with other benefits under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. This Guide is a recap of an educational webinar we hosted to help small-business owners and sole proprietors evaluate their options under the CARES Act. You can also replay the webinar in our online Resource Center.

Please note, as of April 16, the SBA emergency loan program had run out of funds, but received additional funds of up to $310B through new legislation passed in Congress April 23. The information that is provided in this guide is for information purposes and is not intended to replace tax or legal advice specific to your situation. To navigate to the recently added ‘Precautions to Avoid Small Business Loan Fraud’, click here.

On June 3, 2020, the Paycheck Protection Program Flexibility Act (PPPFA) of 2020 was signed into law to give borrowers additional time and flexibility to use the Paycheck Protection Program (PPP) loan proceeds. Please refer to this link for updates on the PPP program as of June 3, 2020.

Businesses and nonprofits with 500 or fewer employees that have experienced economic uncertainty as result of the novel coronavirus pandemic. This piece of the overall CARES legislation seeks to help businesses remain open, pay their employees, provide benefits, and cover other expenses during this crisis. Sole proprietors can also receive assistance.

Small businesses can choose one of the following three CARES Act relief options to help with payroll costs:

Two other CARES relief programs are also available:

All applications:

Sole Proprietors/Self Employed:

Entities:

Applicants with employees will need the following:

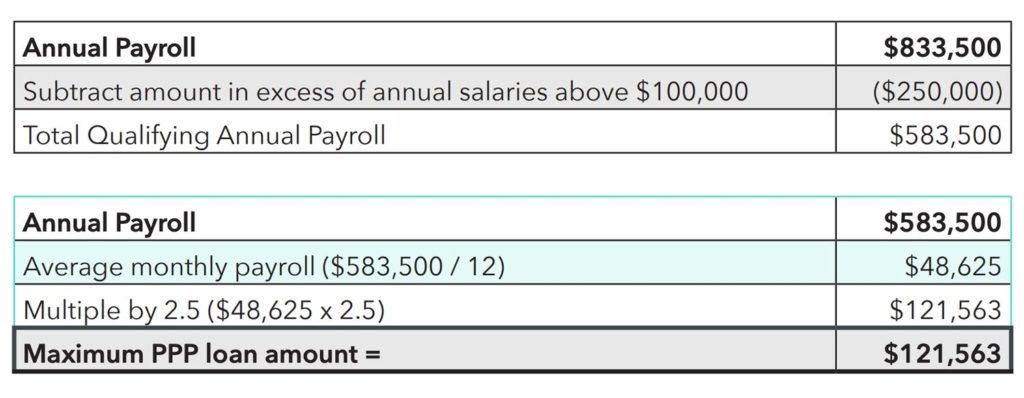

To determine your maximum loan amount, calculate your business’s average monthly payroll costs—capped at $100,000 annually for each employee—and multiply the average by 2.5. In general, borrowers can calculate annual payroll costs using either the previous 12 months or the calendar year 2019. Also, the cap of $100,000 is for cash compensation, and not for non-cash benefits, such as employer contributions to retirement plans, premiums for group healthcare coverage, and payment of state and local taxes assessed on compensation of employees.

You will not be required to repay the amount that you spend on qualifying costs to maintain your staff and payroll during the eight weeks after you receive the loan. However, no more than 25% of the forgiven amount can be applied to non-payroll costs, such as mortgage interest, rent, or utilities.

The eight week period begins on the date the lender makes the first disbursement of the PPP loan to the borrower. The lender must make the first disbursement of the loan no later than 10 calendar days from the date of loan approval.

Any borrowed amount beyond what you spent on qualifying costs must be repaid. Your amount of loan forgiveness could also be reduced if you decrease your full-time employee headcount or reduce salaries and wages by more than 25% for any employee who earned less than $100,000 in 2019.

The interest rate is fixed at 1.00%. All payments are deferred for six months—though interest will accrue over that period—and the repayment period is two years. No collateral or personal guarantee is required.

For more details, consult this PPP fact sheet.

Here is a hypothetical case study: A dentist office with eight employees, including the owner, had to close March 28 due to COVID-19 restrictions. It expects to reopen with four employees on May 1 and bring back the remaining four employees on May 25.

The business borrows its maximum allowable PPP loan amount based on the following calculations:

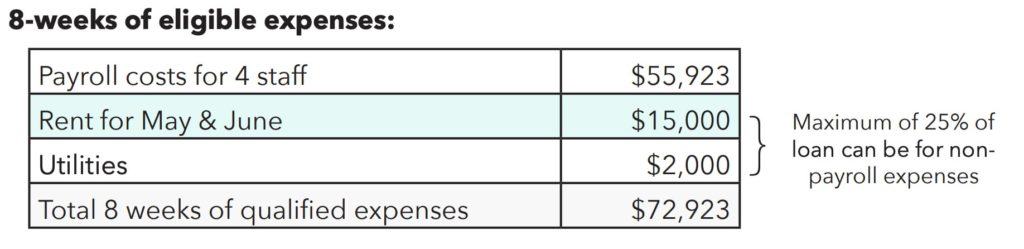

From the loan origination date of April 30, 2020 through the end of June 2020, the dentist office incurs $72,923 of qualifying expenses:

In addition, the office continued to pay its four idled employees $21,154—bringing the total eligible expenses to $94,077. With that amount forgiven, the business must repay just $27,486.

You determine payroll expenses by using your net income, which is the amounts you entered on tax schedules C and F (profit and loss from the business).

We recommend consulting with your financial and tax advisors before you choose an option. Generally speaking, the PPP option may be better for a business with higher-salaried staff while the Employee Retention Credit is a more appropriate choice for covering lower salaries and wages. If you prefer not to incur a loan, then deferring your payroll tax obligation may be the most attractive choice.

Up to $2 million; for a loan of $200,000 or less, no personal guarantee is required. The EIDL interest rate is fixed at 3.5% and the loan can be repaid over 30 years. An EIDL is not forgivable, however.

When you apply for an EIDL, the lender is required to pay $10,000 within three days. The three-day countdown starts when the lender acknowledges receipt of the loan application. This amount does not have to be repaid—regardless of whether your EIDL application is approved.

Yes—but your business cannot apply EIDL and PPP funds toward the same expenses. For example, you would not be allowed to count your May and June rent payments, or the salaries and wages for specific employees, as eligible costs under both loans.

No, you can only choose one of those actions.

U.S. Small Business Administration (SBA) lending institutions are currently accepting applications, and the available funds are limited, so you should apply as soon as possible.

If you receive any calls, emails, or other communications claiming to be from the Treasury Department or the SBA offering you grants or stimulus payments in exchange for personal financial information, do not respond. Neither the Treasure Department nor the SBA makes such calls. In addition, don’t provide any private information, especially not social security numbers, credit card details, or banking information. Scammers could use this information to apply for a loan on your behalf―and you’ll be on the hook for paying it back.

If someone or some entity says they can get you a loan faster for a fee, don’t buy it. Loans under the new CARES Act are set up so that business owners will not have to pay any kind of related fees―this includes application fees, package fees, and closing fees. If a company or person is telling you they can get you an SBA loan under the new PPP in a matter of hours, steer clear. If a company offers you a quick advance that’s unrelated to the new PPP or any other stimulus package, you should also be leery, as you may run into rapid repayment terms at exorbitant interest rates.

While lenders don’t have to be on the SBA’s preferred lender’s list to process these loans, they do have to apply for SBA certification before granting your loan, and there’s no telling how long that will take. We recommend you go through a bank with whom you already have a relationship. That familiarity with your company might make the lending process easier. If not, then we recommend you go through a federally backed credit union or traditional SBA lender, as they’ll be the most familiar with the program. The Treasury Department requires that all new loans to small businesses comply with the Know Your Customer (KYC) requirement for anti-money laundering purposes. KYC is a costly and time-consuming process and puts the risk of error on the banks’ shoulders. It is one reason why some of the largest banks are only offering these loans to existing customers whom they already know.

Check the following websites daily for new information and official requirements associated with each specific relief program:

Mercer Advisors is also posting frequent updates about the CARES Act and other coronavirus-related topics on our “Insights for Navigating Recent Events” Resource Center.