In 2016, Standard & Poor’s announced its decision to add an eleventh sector to the S&P 500 Index – real estate. This change was made effective August 31, 2016. At the time, market pundits predicted massive inflows to REITs from investors seeking to capitalize on the sector’s addition to the market’s most popular U.S. equity index.

And indeed investors did exactly that – in the two-week period following real estate’s addition to the S&P 500 Index, retail and professional investors alike poured over $3 billion into REIT funds. Not to be outdone by Standard & Poor’s, Congress and the White House doubled down on real estate in late 2017 with the passage of the passage of the Tax Cuts and Jobs Act (TCJA), which granted preferential tax treatment to REIT dividends. The new tax law effectively capped taxes on REIT dividends at 29.5% (which were previously taxed as ordinary income at rates as high as 39.6%). In light of so much favorable news, the argument for overweighting REITs seemed pretty ironclad at the time. If ever investors could time a good entry point into an asset class, late 2016 and 2017 was it.

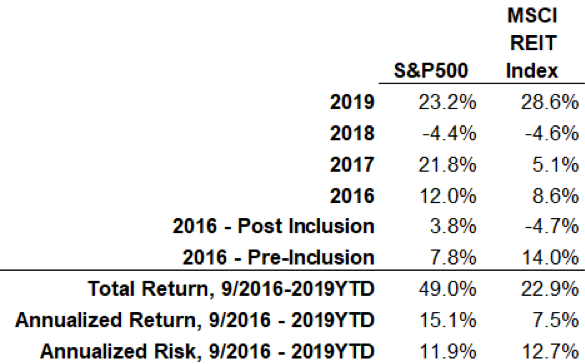

Using the MSCI REIT Index as a proxy for REITs, below I compare REITs to the returns of the S&P 500 Index since 2016 when real estate was added to the index. Since that time, the S&P 500 has outperformed the MSCI REIT Index on both an absolute and risk-adjusted basis, with the S&P 500 (inclusive of REITs) besting the REIT Index 43% to 23% on a cumulative basis subsequent to its inclusion in the S&P 500. On an annualized basis, the S&P 500 outperformed the MSCI REIT Index by 7.6% per year.

But a more granular analysis shows that timing asset classes based on news and tax policy is an exercise in futility. Investors who poured into REITs hoping to cash in on the sector’s new inclusion in the index were rewarded with negative returns the rest of the year. The return on REITs in 2016 prior to their inclusion in the S&P 500 was a staggering 14%; REIT returns post-inclusion were -4.7% for the remainder of 2016. The following year proved no better, with the S&P 500 Index outperforming REITs by nearly 17% in 2017. Those investors who, in response to the TCJA, overweighed REITs in late 2017 fared no better; they were disappointed in 2018 when the S&P outperformed REITs, this time by 0.2% (In the 2018, the S&P 500 returned -4.4% versus -4.6% for REITs).

REITs have posted strong returns in 2019. Through October 31, REITs have returned 28.6% versus 23.2% for the S&P 500. Alas, this is why investors are now suddenly bullish on them (recency bias, anyone?). But investors who entered REITs in late 2016 have a long way to go before they break-even on their market-timing decision; since that time, even in light of 2019’s strong returns, REITs are still underperforming the broad market by over 26%.

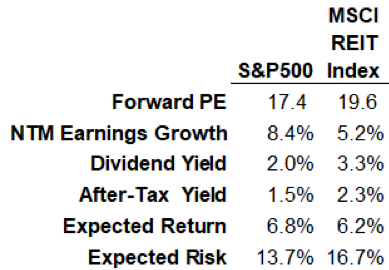

Does this mean now is a good time to overweight REITs, given their underperformance? Predicting market or asset class performance is difficult at best. But two fundamentals tell us that investors would be wise not to overweight REITs. With a forward price-to-earnings ratio of 19.6 times next year’s earnings, REITs are not very attractive. This means REITs are trading at a premium to the S&P 500 Index, which is currently priced at 17.4 times next year’s earnings. Said differently, REITs are about 13% more expensive than the broad market.

What do investors get for this premium pricing? Lower forecasted earnings growth of only 5.2% in 2020, versus 8.4% for the S&P 500. The math doesn’t support overweighting REITs.

Trying to outsmart the market by making outsized bets on specific sectors or asset classes is difficult at best and impossible at worst. Investors seeking to construct portfolios that differ significantly from the broad market should proceed with extreme caution. This isn’t to say there aren’t factors that have been shown to outperform the market over the long term. Indeed there are – many of them, like value and quality – that investors should continue to own as part of a long-term diversified investment strategy. But there is no evidence that a specific sector – no matter how good the news – will or should outperform the market over any horizon.

I advise clients to continue to take a globally diversified approach to investing while avoiding the urge to overweight specific sectors.

As published in advisorperspectives.com, December 11, 2019