For many retirees, one of the biggest unknowns when approaching retirement is figuring out their health care costs. According to a recent study by Fidelity, the average retired 65-year-old couple may need approximately $285,000 saved (after tax) to cover health care expenses during retirement.1 Because these estimates are based on average costs, your actual costs may be more or less depending on when and where you retire, how healthy you are, and how long you’ll live.

For some, $285,000 might be a significant but manageable number. But for many retirees this number can derail even the most well-conceived retirement, because it doesn’t account for long-term care and other catastrophic events, such as a debilitating/chronic illness or injury. While there is no way you can completely plan for your health care costs in retirement, here are some steps you can take to make sure you’re covered.

Medicare is the government-sponsored health care system for US citizens aged 65 or over. It consists of Part A (hospital coverage), Part B (physician and outpatient hospital coverage), and Part D (prescription coverage). Most people do not pay any premiums for Part A (if you paid Medicare taxes while working).

For Part B, you pay a premium based on your modified adjusted gross income (Medicare uses your modified adjusted gross income as reported on your previous tax returns from two years ago to calculate your premium). Most Americans pay $135.50 per month for Part B coverage for 2019; however, Part B premiums can be as much as $460.50 per month for those with the highest incomes.2 In addition, many Americans purchase Medicare Supplement (also called Medigap) insurance to cover Part B deductibles and co-pays. There are many different Medicare Supplement plans, but the more popular plans typically cost a 65-year-old between $100–$150 per month.3

Part D varies depending on where you live and the insurance provider. According to the National Council on Aging, the nationwide average monthly Medicare Part D premium for 2019 is $33.19.4 When you add up all these costs, a “typical” retiree will spend more than $300 per month on Medicare premiums and supplemental insurance. Also, Medicare premium costs generally increase every year, while Medicare supplemental insurance costs increase every few years, depending on the company.

Also, Medicare Supplement Plan F, which pays many of the out-of-pocket costs not covered under standard Medicare (as well as the Part B deductible), will no longer be available to people who become newly eligible for Medicare on or after January 1, 2020. Individuals who already have Plan F or who are eligible to enroll before the end of 2019 can retain Plan F coverage. You can read more about these changes here.

Things to remember

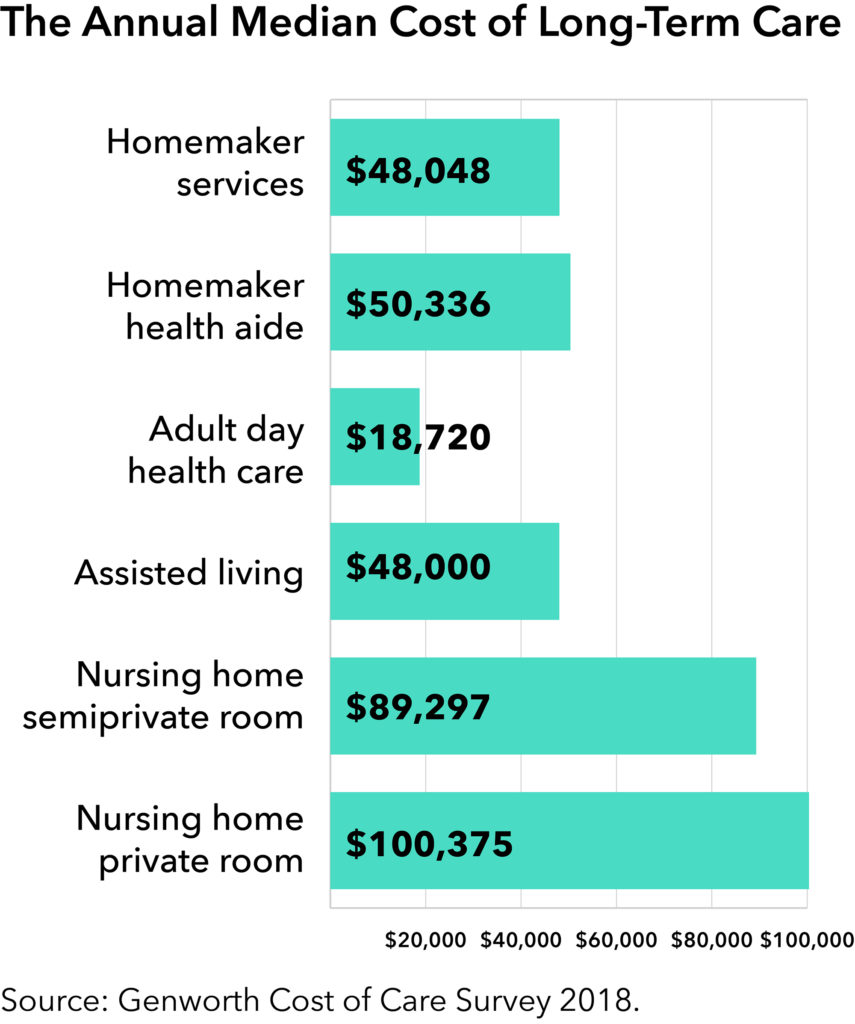

Doesn’t Medicare Cover Long-Term Care?

Doesn’t Medicare Cover Long-Term Care?Unfortunately, Medicare has very limited benefits for long-term care. It only covers care under very specific circumstances, and generally for a portion of the costs for up to 100 days for each benefit period. For example, the level of care that some retirees may require in a nursing home would not be covered by Medicare.

While you can factor in monthly Medicare premiums into your retirement plan, it’s critical to have a plan for long-term care. There are several options:

Meet with your advisor to discuss how your retirement plan addresses health care spending. This discussion may include details about your family history, liquidity needs for unexpected expenses, your options for Medicare and long-term care needs. Your advisor can help you plan ahead for the expected and unexpected life events you may face, and put a plan in place that you can rely on.

Want to learn more about Medicare and health care costs in retirement? Consider these other resources:

To Max Retirement Savings Think HSA