On Thursday of last week President Biden signed the $1.9 trillion American Rescue Plan Act into law. As with all government spending, questions invariably arise around if and how the spending might impact the economy, inflation, and capital markets. But with the economy already on the road to recovery, is this new relief package really needed?

The bill comes at a time when COVID cases have fallen significantly from their mid-January highs. The 7-day rolling average for new infections hit a high in mid-January of about 250,000 per day. They’ve since fallen nearly 80% to a 7-day moving average of about 55,000 daily new cases. With daily vaccinations now averaging about 2.5 million, public health experts predict the American public could reach herd immunity by late summer. All of this is to say that this bill comes at a time when the economy was already expected to experience a vigorous recovery in GDP growth later this year (and, subsequently, a recovery in corporate earnings and jobs creation). The challenge, the bill’s proponents argue, is twofold: first, helping American families bridge the gap between then and now and, second, making sure we deliver a decisive knock-out blow to COVID-19. To better understand the bill’s impact, let’s tackle a few questions on the mind of investors.

First, do we really need this new relief package now? All government spending—whether funded through tax increases, borrowing, or tax cuts (yes, tax cuts are a form of government spending)—should be subjected to such scrutiny. My view is that COVID-19 has proven itself a formidable enemy; it is a multidimensional contagion that spreads both fear and infection, both of which have been socially and economically crippling for over a year now. Subsequently, it’s pretty simple: if we hope to help the economy, the first rule of virus economics is to first stop the virus.1

But what about the national debt? I’m sympathetic to concerns about mounting government debt. It’s grown to levels none of us thought possible and it needs to be addressed. But now isn’t the time to suddenly embrace fiscal austerity. We didn’t do so in our drive to defeat the Axis powers during the Second World War and I’d argue we shouldn’t do so now in our drive to defeat COVID. The time for fiscal austerity is in times of plenty before a crisis or for when the crisis has passed; not while we’re in the middle of it and certainly not while the federal government can borrow at near zero interest rates. If a $1.9 trillion package is the decisive, knock-out punch we need to defeat COVID once and for all, then I’m 100% on board.

Is this really the “right” package?

I’m not a public policy expert, so I don’t know. The act’s detractors have been quick to question whether it’s little more than a handout to Democratic special interest groups. But to be fair, all government spending arguably includes a degree of pork for special interest groups and no single party has a monopoly on catering to special interests. Remember the Tax Cut and Jobs Act (TCJA) of 2017 and its special tax treatment of real estate investments? Or the CARES Act’s $25 million handout to the Kennedy Center for the Performing Arts? Both were arguably little more than handouts for special interests. This new bill undoubtedly has pork buried in it that will come to light in the days and weeks ahead. But while we can all argue over the relative merits and amounts of funding provided to specific groups and special interests, at the moment the bill’s funding for healthcare, education, state and local governments, economic stimulus, and extended unemployment benefits appears to be relatively well-targeted.

Will the bill cause inflation?

The enactment of the American Rescue Plan into law comes at a time when the U.S. economy has an estimated output gap of approximately $1 trillion. And that’s after several multi-trillion dollar rounds of stimulus already. Yet Headline CPI remains an anemic 1.7%; Core CPI is even less at 1.3%. Let’s not forget that we’ve already invested trillions in combating COVID with virtually no inflation to show for it. And with such a staggering output gap, the federal government clearly has room to go big on spending without overheating the economy. But $1.9 trillion is pretty big, perhaps too big, as Harvard economist Larry Summers recently argued.2 If it’s too big, it’s probably too big by about $900 billion—which is equivalent to about 4% of GDP (at potential output of about $20-$22 trillion by 2021 – 2023).

My view? Economists all too often suffer from over precision biases—which is comical when we consider the data they have to work with is typically messy and imprecise to begin with. But I would make three additional points.

- First, any rise in inflation would likely be transitory, meaning it likely wouldn’t be permanent. Much of the expected recovery in GDP growth later this year will come from pent up consumer demand—consumers looking to begin vacationing and dining out again, etc. That consumption isn’t expected to remain at elevated levels in perpetuity. Likewise, the new bill’s spending isn’t permanent. It’s not like we’ve signed up for $1.9 trillion in new annual spending. For example, it doesn’t provide funding for unemployment benefits, vaccinations, or aid to state and local governments in perpetuity. While the package is large, it’s nevertheless finite.

- Second, a temporary rise in inflation of somewhere between 1% and 4% doesn’t seem all that threatening given the Fed has repeatedly failed to hit its 2% inflation target for more than a decade, a fact that’s all the more shocking when we consider that it failed to do so despite nearly $5 trillion in quantitative easing. For the Fed to hit an average inflation target of 2% (over a three-year period), inflation needs to average well north of 2% for a period of time to get us there from where we are now. The takeaway is that we have room for inflation to rise.

- Finally, and perhaps most controversially and counterintuitively, a rise in inflation would be a boon for some investors, especially retirees and those concerned about market valuations. How so? Because with higher inflation we can finally have higher interest rates. The Fed has lots of great tools for combating inflation should it occur (e.g., like higher interest rates). It has no good tools for combating deflation, which is a very real risk given the economy’s output gap. Even if the Fed is politically hesitant to increase rates to cool the economy, a rise in inflation expectations should still lead to a rise in interest rates in the absence of action from the Fed. We’re already seeing this play out in the bond market. The yield on the 10-year has risen almost 70 basis points since the start of the year and now stands at about 1.6%; it’s up 1.10% from its August lows. The takeaway? Higher inflation means higher rates and higher rates means higher income for retirees (and other fixed income investors). Further, a rise in rates would bring some sanity back to equity valuations, especially highly leveraged growth stocks. While no one wants to see asset valuations decline, I would argue we also don’t want to see lofty (and unstable) asset prices fueled by little more than cheap credit. Rising rates can help bring sanity back to asset prices and investor behavior (re: GameStop, Bitcoin).

The road to recovery

I’m hopeful the package is just what the doctor ordered: a powerful shot in the arm to finally knock out COVID once for and for all. Yes, I expect there will be bruising; this is certainly a spending bill of massive proportions that, when combined with the federal government’s existing $27 trillion in debt outstanding, will burden taxpayers for generations to come. But the first step towards repairing our economy and addressing our debt is to first win the war against COVID.

Source: “What Is In The Third COVID-19 Stimulus Package”, Wall Street Journal, Mach 11, 2021.

Source: YCharts

Home » Insights » Market Commentary » The American Rescue Plan Act: Inflationary largesse or just what the doctor ordered?

The American Rescue Plan Act: Inflationary largesse or just what the doctor ordered?

Donald Calcagni, MBA, MST, CFP®, AIF®

Chief Investment Officer

Summary

The American Rescue Plan Act, signed into law last week, is poised to help millions of Americans bridge the gap to later this year when economists expect a more robust recovery to take hold.

On Thursday of last week President Biden signed the $1.9 trillion American Rescue Plan Act into law. As with all government spending, questions invariably arise around if and how the spending might impact the economy, inflation, and capital markets. But with the economy already on the road to recovery, is this new relief package really needed?

The bill comes at a time when COVID cases have fallen significantly from their mid-January highs. The 7-day rolling average for new infections hit a high in mid-January of about 250,000 per day. They’ve since fallen nearly 80% to a 7-day moving average of about 55,000 daily new cases. With daily vaccinations now averaging about 2.5 million, public health experts predict the American public could reach herd immunity by late summer. All of this is to say that this bill comes at a time when the economy was already expected to experience a vigorous recovery in GDP growth later this year (and, subsequently, a recovery in corporate earnings and jobs creation). The challenge, the bill’s proponents argue, is twofold: first, helping American families bridge the gap between then and now and, second, making sure we deliver a decisive knock-out blow to COVID-19. To better understand the bill’s impact, let’s tackle a few questions on the mind of investors.

First, do we really need this new relief package now? All government spending—whether funded through tax increases, borrowing, or tax cuts (yes, tax cuts are a form of government spending)—should be subjected to such scrutiny. My view is that COVID-19 has proven itself a formidable enemy; it is a multidimensional contagion that spreads both fear and infection, both of which have been socially and economically crippling for over a year now. Subsequently, it’s pretty simple: if we hope to help the economy, the first rule of virus economics is to first stop the virus.1

But what about the national debt? I’m sympathetic to concerns about mounting government debt. It’s grown to levels none of us thought possible and it needs to be addressed. But now isn’t the time to suddenly embrace fiscal austerity. We didn’t do so in our drive to defeat the Axis powers during the Second World War and I’d argue we shouldn’t do so now in our drive to defeat COVID. The time for fiscal austerity is in times of plenty before a crisis or for when the crisis has passed; not while we’re in the middle of it and certainly not while the federal government can borrow at near zero interest rates. If a $1.9 trillion package is the decisive, knock-out punch we need to defeat COVID once and for all, then I’m 100% on board.

Is this really the “right” package?

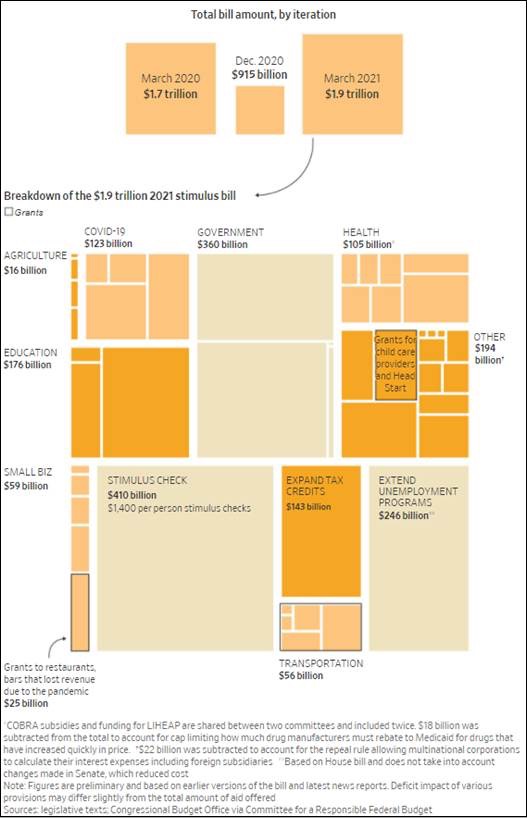

I’m not a public policy expert, so I don’t know. The act’s detractors have been quick to question whether it’s little more than a handout to Democratic special interest groups. But to be fair, all government spending arguably includes a degree of pork for special interest groups and no single party has a monopoly on catering to special interests. Remember the Tax Cut and Jobs Act (TCJA) of 2017 and its special tax treatment of real estate investments? Or the CARES Act’s $25 million handout to the Kennedy Center for the Performing Arts? Both were arguably little more than handouts for special interests. This new bill undoubtedly has pork buried in it that will come to light in the days and weeks ahead. But while we can all argue over the relative merits and amounts of funding provided to specific groups and special interests, at the moment the bill’s funding for healthcare, education, state and local governments, economic stimulus, and extended unemployment benefits appears to be relatively well-targeted.

Will the bill cause inflation?

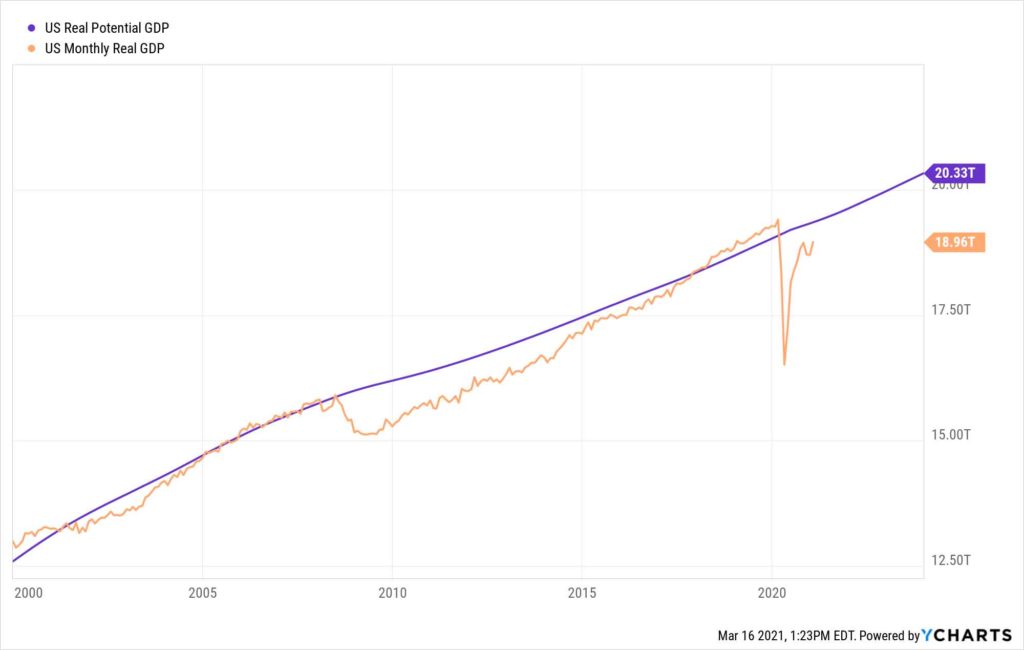

The enactment of the American Rescue Plan into law comes at a time when the U.S. economy has an estimated output gap of approximately $1 trillion. And that’s after several multi-trillion dollar rounds of stimulus already. Yet Headline CPI remains an anemic 1.7%; Core CPI is even less at 1.3%. Let’s not forget that we’ve already invested trillions in combating COVID with virtually no inflation to show for it. And with such a staggering output gap, the federal government clearly has room to go big on spending without overheating the economy. But $1.9 trillion is pretty big, perhaps too big, as Harvard economist Larry Summers recently argued.2 If it’s too big, it’s probably too big by about $900 billion—which is equivalent to about 4% of GDP (at potential output of about $20-$22 trillion by 2021 – 2023).

My view? Economists all too often suffer from over precision biases—which is comical when we consider the data they have to work with is typically messy and imprecise to begin with. But I would make three additional points.

The road to recovery

I’m hopeful the package is just what the doctor ordered: a powerful shot in the arm to finally knock out COVID once for and for all. Yes, I expect there will be bruising; this is certainly a spending bill of massive proportions that, when combined with the federal government’s existing $27 trillion in debt outstanding, will burden taxpayers for generations to come. But the first step towards repairing our economy and addressing our debt is to first win the war against COVID.

Source: “What Is In The Third COVID-19 Stimulus Package”, Wall Street Journal, Mach 11, 2021.

Source: YCharts

1University of Chicago economist Austan Goolsbee calls this the “Number 1 rule of virus economics”; see Goolsbee, Austan. “The need to spend without delay in battling the Coronavirus”, The New York Times. February 6, 2021.

2 Summers, Lawrence, H. “The Biden stimulus plan is admirably ambitious. But it brings some big risks, too.”, The Washington Post, February 4, 2021

The Hidden Hazards of Inheriting an IRA: Why Beneficiaries may Face More Harm than Good

Financial Planning for Caregivers of Aging Family Members

To Minimize Inheritance and Estate Tax, Make These Moves Now

Mercer Advisors Inc. is the parent company of Mercer Global Advisors Inc. and is not involved with investment services. Mercer Global Advisors Inc. (“Mercer Advisors”) is registered as an investment advisor with the SEC. The firm only transacts business in states where it is properly registered or is excluded or exempted from registration requirements.

All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate but is not guaranteed or warranted by Mercer Advisors. Content, research, tools and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. For financial planning advice specific to your circumstances, talk to a qualified professional at Mercer Advisors.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy or product made reference to directly or indirectly, will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark.

This document may contain forward-looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.