Originally published in Wealth Point, November 2018

Diversification offers crucial asset protection during volatile market cycles, helping with risk management in your financial planning. The market sell-off in October 2018 reminded us once again of the virtues of diversification, and due to the diversified nature of both of our Mercer Advisors portfolio management models, they each returned less than the market this year prior to the sell-off. Since the sell-off, however, they’ve outperformed due to the downside protection inherent in more diversified portfolios. The purpose of diversification in our view is to smooth out the peaks and valleys of the market, and ensure clients achieve their financial goals with the highest degree of confidence possible.

Over the past several quarters, we highlighted a series of concerns facing investors, specifically rising interest rates, resurgent inflation, and extreme valuations for growth and technology stocks. Through September 30, the market largely shrugged off these concerns. Highly valued growth stocks, undeterred by rising interest rates, fueled the S&P 500 Index ever higher. Investors continued to overweight their portfolios to the most popular stocks in the market and questioned the wisdom of diversification, especially the wisdom of owning non-US stocks and bonds. Investors had apparently gone all in on growth stocks, throwing diversification and caution to the winds.

That all changed the second week of October. On Wednesday, October 10, the Dow Jones Industrial Average lost a staggering 832 points, the second largest point loss in history. The following day, it gave up another 546 points, the 13th largest point loss in market history. The VIX, a volatility-measuring index often called the market’s “fear gauge,” spiked to its highest levels since February’s “volatility flash crash.” It appeared markets were beginning to digest—and price in—interest rates hikes, including the prospect of four additional interest hikes forecasted by the US Federal Reserve in its efforts to combat inflation and slowly shrink its balance sheet to pre-2008 levels.

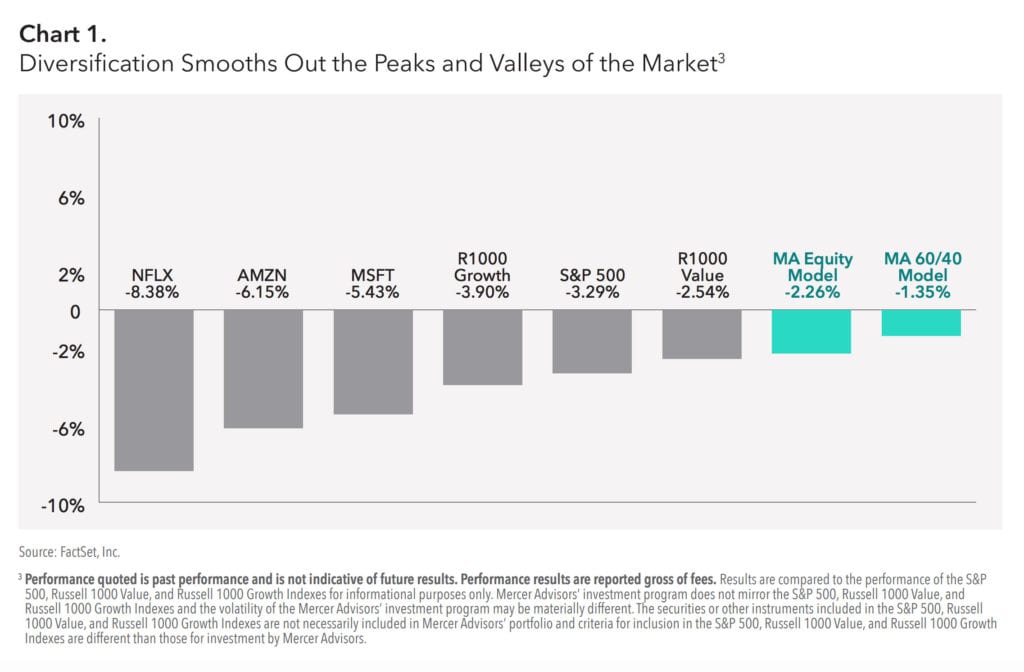

Prior to the sharp sell-off, the market’s year-to-date advance was exceptionally narrow. Only three stocks—Amazon, Netflix, and Microsoft—accounted for nearly 50% of the S&P 500’s year-to-date returns, highlighting the dangers of comparing any diversified investment strategy to an index whose returns were tied so closely to the fortunes of just three technology stocks. Imagine betting the house—your Economic Freedom, a lifetime of savings, your children’s education—on just three stocks in hopes of earning a percentage return greater than that of the index. All three stocks saw significant declines on October 10. While the relatively “more diversified” Russell 1000 Growth Index returned -3.90%, Netflix fell 8.38%, followed by Amazon (6.15%) and Microsoft (5.43%) respectively. Collectively these three stocks lost 6.65% on October 10 alone. The FAANG stocks—Facebook, Amazon, Apple, Netflix, and Google— collectively lost 5.67%.

The market sell-off on October 10 reminded us once again of the virtues of risk management through diversification. Often underappreciated and occasionally even resented, diversification is like fire insurance: no one wants to own it – until their home is ablaze. But by then it’s too late. The price of diversification spikes when the house is on fire, just when it’s needed most. It’s precisely during such times of extreme market volatility that diversification is most appreciated, and we’re reminded that investing is best viewed as an exercise in risk management, and one less fixated on winning the Indy 500.

Consider the Mercer Advisors Equity model, a globally diversified portfolio consisting of US and non-US equities, and Mercer Advisors 60/40 models. The 60/40 model, our most popular asset allocation model, is identical to the Mercer Advisors Equity model, but also includes a 40% allocation to short- term, high-quality bonds. Both portfolios own thousands of stocks across 46 different countries.  No one wanted to own non-US stocks prior to last week’s sell-off, yet the MSCI EAFE Index1, a non-US equity index, lost only 0.49% in the October 10 sell-off. Diversifying part of your portfolio into non-US stocks would’ve paid off on or before October 9; by October 10, it was too late.

No one wanted to own non-US stocks prior to last week’s sell-off, yet the MSCI EAFE Index1, a non-US equity index, lost only 0.49% in the October 10 sell-off. Diversifying part of your portfolio into non-US stocks would’ve paid off on or before October 9; by October 10, it was too late.

The same could be said for bonds. Given the Fed’s recent interest rate hikes and prospects for more, investors have questioned the wisdom of owning bonds in a rising interest rate environment. But it’s precisely during such environments that equity markets tend to experience selloffs. October 1987, early 2000, and 2008 are all prime examples of rising interest rate environments where equity prices corrected, and bond allocations provided much-needed portfolio diversification against steep sell-offs in stocks. And the powerfully diversifying effect of bonds hasn’t waned; the Barclays Global Aggregate Bond Index returned a positive 0.18% on October 10, while the Dow Jones, S&P 500, and every other major stock index saw steep declines.

It’s precisely due to the diversified nature of the Mercer Advisors Equity and 60/40 models that they weathered the sell-off relatively well. The Equity model and 60/40 model returned -2.26% and -1.35%, respectively, on October 102. This is what diversification and the advantage it brings looks like. Compare these returns to those non-diversified alternatives in Chart 1.

Netflix, Amazon, Microsoft, the Russell 1000 Growth, Russell 1000 Value, and S&P 500 all lost significantly more.

Finally, let’s be forthright about this: due to the diversified nature of both of our Mercer Advisors model portfolios, they each returned less than the market this year prior to the sell-off. Since the October 10 sell-off, however, they’ve outperformed due to the downside protection inherent in more diversified portfolios.

The purpose of diversification in our view is to smooth out the peaks and valleys of the market, and ensure clients achieve their financial goals with the highest degree of confidence possible. So, ask yourself this: What’s more important, earning higher returns via an undiversified index, such as the S&P 500, or protecting your wealth and your Economic Freedom from severe market declines? We believe in taking a diversified approach to portfolio management.

Diversifying part of your portfolio into bonds or non-US stocks on or before October 9 would’ve paid big dividends on October 10.

Mercer Advisors Inc. is the parent company of Mercer Global Advisors Inc. and is not involved with investment services. Mercer Global Advisors Inc. (“Mercer Advisors”) is registered as an investment advisor with the SEC. The firm only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements.All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change. Some of the research and ratings shown in this presentation come from third parties that are not affiliated with Mercer Advisors. The information is believed to be accurate, but is not guaranteed or warranted by Mercer Advisors. Content, research, tools, and stock or option symbols are for educational and illustrative purposes only and do not imply a recommendation or solicitation to buy or sell a particular security or to engage in any particular investment strategy. For financial planning advice specific to your circumstances, talk to a qualified professional at Mercer Advisors.

Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy or product made reference to directly or indirectly, will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals may materially alter the performance and results of your portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will either be suitable or profitable for a client’s investment portfolio. Historical performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing historical performance results. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark.

This document may contain forward-looking statements including statements regarding our intent, belief or current expectations with respect to market conditions. Readers are cautioned not to place undue reliance on these forward-looking statements. While due care has been used in the preparation of forecast information, actual results may vary in a materially positive or negative manner. Forecasts and hypothetical examples are subject to uncertainty and contingencies outside Mercer Advisors’ control.